The scene became familiar in neighborhoods across the country: as the US housing bubble burst in 2007, "For Sale" signs appeared in front yards, neighbors fled hopelessly underwater mortgages, and homeowners watched as the nation’s unemployment rate rose, worried their jobs might be next.

But while the US economy began a slow recovery, housing prices continued to drop, with mortgage rates reaching an all-time low earlier this year. If the white picket fence is a thing of the past, what does the future of housing look like, and how can Americans own a piece for themselves? It’s a question being asked at Columbia Business School’s Paul Milstein Center for Real Estate, which creates curricula and case studies, brings in industry professionals to talk with students, and promotes policy research on real estate among faculty members, including center director Lynne B. Sagalyn, the Earle W. Kazis and Benjamin Schore Professor of Real Estate, and Chris Mayer, the Paul Milstein Professor of Real Estate, research director of the Milstein Center, and co-director of the Richard Paul Richman Center for Business, Law, and Public Policy.

Hermes tapped Mayer, Sagalyn, and MBA Real Estate Program student Adam Cohen '13 to share their candid thoughts on the US housing market, where it’s going, and what homebuyers and investors need to know.

Interest rates are low, but most Americans still can’t get a mortgage. When will things improve for homebuyers?

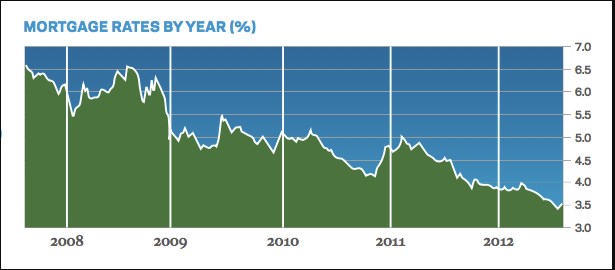

Chris Mayer: One of the biggest challenges in the housing market right now is getting access to credit. Many lenders, even if you can meet some of the standards for government loans, won’t make the loan. They’re worried that if anything bad happens, they’ll be forced to buy the loan back. To get a loan from Fannie Mae or Freddie Mac with the average headline rate (3.53 percent as of September 18), you need near pristine credit. People who lost their jobs during the recession and found another job within a couple of months may have problems qualifying for a mortgage.

Lynne Sagalyn: Historically, the problem that typical first-time homebuyers faced was that they couldn’t qualify because they didn’t have a sufficient down payment. That’s not at all in the discussion today. What Chris is talking about is a breakdown in financial institutions’ willingness to take a modicum of risk. They want to take no risk or the top 10 percent of the pyramid of risk. That’s a very different situation than we’ve ever faced before, save for after the Great Depression.

CM: Even with a strong down payment or good credit, banks are afraid that if the homeowner defaults, they’re going to have to own the loan again. Lenders know the rules of the game have changed but don’t know what the new rules are. I don’t think anyone knows the standards for being forced to buy back a loan.

Adam Cohen: It’s interesting that local banks stepped in back in ’08 and ’09 when a lot of the big banks weren’t willing to lend at all. Now, many of those local banks are subject to much stricter regulations and are no longer willing to fill that lending gap, which is creating a bigger strain on the system.

LS: It’s an institutional issue but an economic issue, too — it doesn’t matter what interest rates are if banks aren’t willing to lend.

CM: For a long time, we got used to the idea that you can borrow money to do everything. Our standards got low — if you could breathe, you could get a loan. Changing that mentality is good, but where we are today is much too strict. The problem at the moment is that it may even become harder or more expensive for people to get mortgages. As well, there is real macroeconomic risk, with the global economy weakening. China had an enormous housing bubble that’s collapsing and manufacturing is starting to slow down there. And there are the obvious problems in Europe, along with political and tax challenges in the US. The risk of another downturn is out there.

AC: With that being said, I think most of us feel like if we closed our eyes and opened them in seven years, Treasury rates would be higher than what they are today.

CM: That’s a long seven years, though.

LS: It’d be a long five years, let alone seven.

AC: But I think the consensus is that interest rates will go up, it’s just a question of when. The government has pumped a lot of money into the economy over the past several years. I think we will see an impact from that, which will create inflation and higher interest rates will follow, and hopefully banks will feel more comfortable about lending to more people.

LS: Yeah, but it’s going to take a while. We need real economic demand for credit before we can worry about inflationary pressures. We have a lot of unemployment, and we don’t seem to have capacity problems. You have to look at the interest rate question in conjunction with a lot of the other factors, not just thinking that ’oh eventually, they’ll have to go up. “Eventually” is a long time.

“Lenders know the rules of the game have changed but don’t know what the new rules are.” — Chris Mayer

CM: The fact is that we are recovering from a severe recession, with many people unemployed, underemployed, and seeing their incomes decline. It’s not that all those people are lazy and irresponsible. Many of them have problems now because we had a tough economy. And if banks are going to be unwilling to lend to them until their record is perfect for three years, it’s going to be a very, very long recovery.

Housing prices: has the market hit bottom?

LS: Is there one market?

CM: And is there a single bottom?

LS: Housing conditions of supply and demand are local; property law is state by state; both of these features of real estate are why, intellectually, you can’t talk about "the market." In Manhattan, it may be flat for a while, but we’re past the bottom. Phoenix or Las Vegas may be a different story.

CM: Reported house prices in Phoenix are higher than they were a year ago. And as Lynne said, there’s not one market. In Arizona, there isn’t a judicial process to go through for foreclosure, so it happens much more quickly. Many of the distressed properties have been sold and there’s less inventory on the market. In other places — Florida, New Jersey, California — the foreclosure process is much longer and housing may still decline further.

AC: In New Jersey, it takes two years for a bank to foreclose on a home. When it takes two years, and there is this huge portfolio of backlogged properties, it’s going to take 10 years to get through all the foreclosures. In the meantime, you’re going to have cheap inventory and be unable to get proper appraisals. Ultimately, your market doesn’t recover until that happens.

CM: On a national level, we’ve probably seen most of the decline — as long as the consensus forecast of the economy is correct and we continue to see positive growth, albeit very slow growth, but not another recession. Over the next three years, prices will likely rise as population growth continues and low rates make owning a home attractive. However, as many as 3 million people currently living in their homes who are now not making mortgage payments will eventually lose ownership through a foreclosure, short sale, or even a rental agreement with the bank or a new owner.

Is real estate still a good investment?

LS: People should buy homes to live in them. It’s a consumption good. If anything has proven why buyers should look at a home as consumption and not investment, it’s been this past cycle; other cycles have proven the same thing. When an investor buys a home or an apartment building, it’s a completely different calculus — it’s purely a risk-and-return investment.

CM: I agree — a home is a place to live. With house prices down 15 to 60 percent depending on the market, if you can get a 3.53 percent, 30-year fixed mortgage to buy a place where you’re going to live for a while, this is a wonderful time to buy. If you’re an investor, there are great opportunities to buy homes as rentals if you can finance them responsibly and manage them well.

AC: Managing a single-family home is an entirely different ball game from managing an apartment complex. Single-family homes are much more labor intensive. When you’re buying houses for investing purposes, many investors are focused on the appreciation down the line and their ability to sell them off individually — as opposed to an apartment complex, which tends to be sold based entirely off of its income potential for a prospective landlord.

"It doesn’t matter what interest rates are if banks aren’t willing to lend." — Lynne Sagalyn

LS: There’s been a lot of talk about investors buying portfolios of single-family houses and making a killing — I’ve heard it called a new asset class. To Adam’s point: managing unique, non-standardized homes, on a disparate basis across any market — or across multiple markets — is an intensive management task. Even the large-scale investment companies who have the capital to do this are shying away from it because the management issues are severe. An individual can purchase and rent out five, 10, 15 houses — but to do it in scale of hundreds and thousands, without selling off pieces to individuals, is difficult. It’s not just labor intensive; it’s expensive because there are few economies of scale. You are the landlord, and even if you have your own crew of carpenters and electricians, the problems in an individual house are specific to that house; there are no quick fixes.

How has the mortgage crisis affected the future of housing development and real estate trends?

CM: After the Great Depression, cohorts of people never invested in stocks again the rest of their lives. I do not think that is going to happen in housing. Surveys show that people still want to own homes. But I don’t think we’ll see as many McMansions because fewer people will be able to afford them.

LS: The demographics aren’t going to support them anyway.

CM: But I think as credit markets recover, we will have learned a lesson and approach housing in a more stable way, although history says we have short memories.

LS: There’s something else going on, too. The big shift in urban development is that many people who weren’t born in or never thought about cities previously want to live in cities now. There’s been a phenomenal increase in people of all ages, particularly young and old, wanting to live in cities. And that’s not just in places like New York, Boston, and LA; it’s happening in cities across the country. Whether people live there short-term or long-term, they first make a renter’s decision and may later make an apartment-buying decision. The demographics support this trend going on for quite some time.

What’s the solution to the underwater mortgage problem? Do principal reductions have a role?

CM: For a principal reduction to work, you want someone who’s committed but just can’t quite make the payments on the higher mortgage because their income has been cut. In other cases, it makes more economic sense for the owner to start over because he or she really doesn’t have the income to afford the home. For owners without a job, it’s just not economically feasible for them to stay in the house.

AC: I see what Chris is saying, but there is that significant portion of homeowners who — if you consider what their house is worth today — could afford to stay if they had a reasonable mortgage balance and interest rate. Financially, that would work out best for everybody. It seems that the process to decide who gets help and who doesn’t is quite politically charged.

CM: There’s been a push for the US government-backed institutions to offer principal reductions, which the regulator for Fannie Mae and Freddie Mac has rejected. I understand his point, that there is some risk that when the government runs a program where they forgive the debt, it is different from a private-sector firm doing a principal reduction. The risk is that many borrowers may default to get a principal reduction (the risk of moral hazard), and this risk is bigger for a program that is perceived to be government approved. A good solution would be for Fannie Mae and Freddie Mac to sell non-performing loans to private investors who can better make decisions about principal modifications based on economic, not political, calculations, something the FHA has started to do. Private servicers may also be more likely to do short sales instead of foreclosures where principal modifications don’t make sense. Short sales are often a win-win; much cheaper for the bank and more compassionate for the homeowners than other alternatives.

"It seems that the process to decide who gets help and who doesn’t is quite politically charged." — Adam Cohen '13

LS: What you want is to provide the context for people to recover. It’s all about finding a solution that will aid people and the economy. It’s very hard for government to do things that are not uniform in their application and by definition fair to all.

CM: Private servicers and investors know how to do principal reductions, and they’re better at doing this than the government is. We should have been doing loan sales a long time ago, but, as with all policies, late is better than not at all.

LS: It’s been a learning curve for everyone.

CM: At the end of the day, a home should be thought of as a place to live for the long-term and to finance responsibly, not as a piggybank to borrow against every time something comes up. Most of us have to save more. Most Americans will be unable to retire unless homes are paid off, and that means thinking about housing differently than we have in the past.