I've spent the last decade at MetaProp watching real estate dollars chase the obvious AI infrastructure plays, hyperscale campuses in Northern Virginia, gigawatt sites in West Texas, gas turbines being airlifted to suburban office parks. The capital flows have been staggering and the returns, for now, are real. But the constraints are getting louder than the returns. Power. Water. Land. Local opposition. Permit timelines that outrun lease economics.

So the smartest founders have started asking a different question: what if the data center doesn't sit on land at all?

Two answers are emerging, one beneath the ocean, one above the atmosphere. Most of the press goes to the orbital story. Starcloud just hit a $1.1 billion valuation, the fastest unicorn in Y Combinator history, on the premise of solar-powered compute in low Earth orbit. SpaceX has filed paperwork with the FCC for what could become a vast distributed compute constellation, and Google is running a moonshot called Project Suncatcher.

The underwater story is quieter. It shouldn't be.

Why this matters now

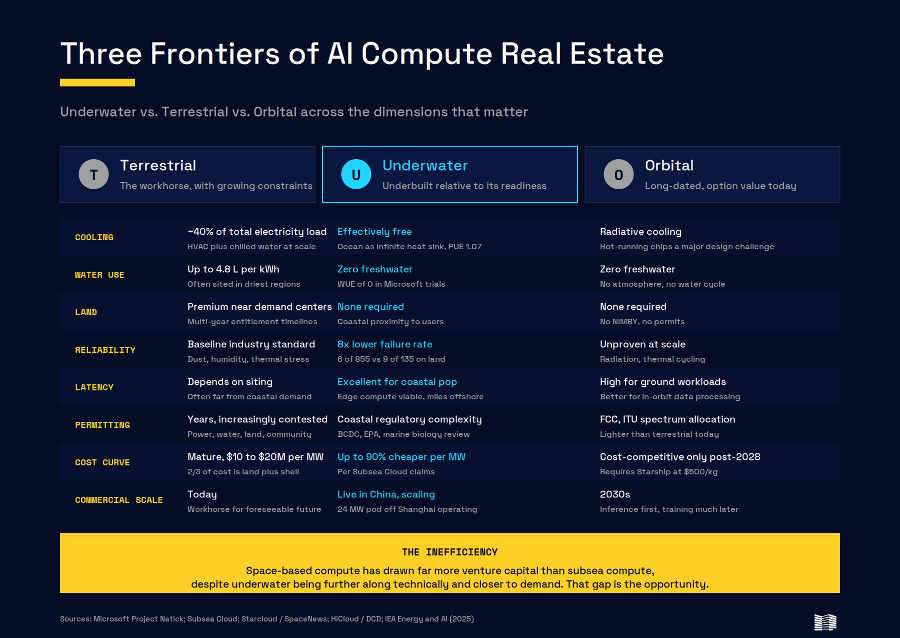

Cooling and water are a large share of a traditional data center's electricity load, and a typical hyperscale facility cycles through hundreds of thousands of gallons of fresh water a day. The industry's response so far has been to push the worst environmental costs into the driest places on earth, Arizona, Spain, the Gulf, which is precisely backwards. Underwater data centers flip that equation. The ocean is a near-infinite, free, naturally cold heat sink. Microsoft's Project Natick, deployed off the Orkney Islands, ran with a power usage effectiveness of 1.07 and zero water consumption. Server failure rates were one-eighth of the matched land-based control group, because the inert sealed environment eliminated the dust, humidity, and human jostling that quietly degrade hardware on land.

Then there's the land question, which is the one that should make every CRE investor pay attention. Coastal metros, where the users actually are, have the worst land economics on the planet. An underwater pod sited a few miles offshore from Manhattan, Boston, San Francisco, Miami, or Singapore is geographically closer to demand than a campus in Loudoun County, with none of the entitlement fights. That's a latency story and a NIMBY story rolled into one.

Figure 1. Underwater, terrestrial, and orbital compute compared across the dimensions that drive real estate underwriting.

Who's actually building

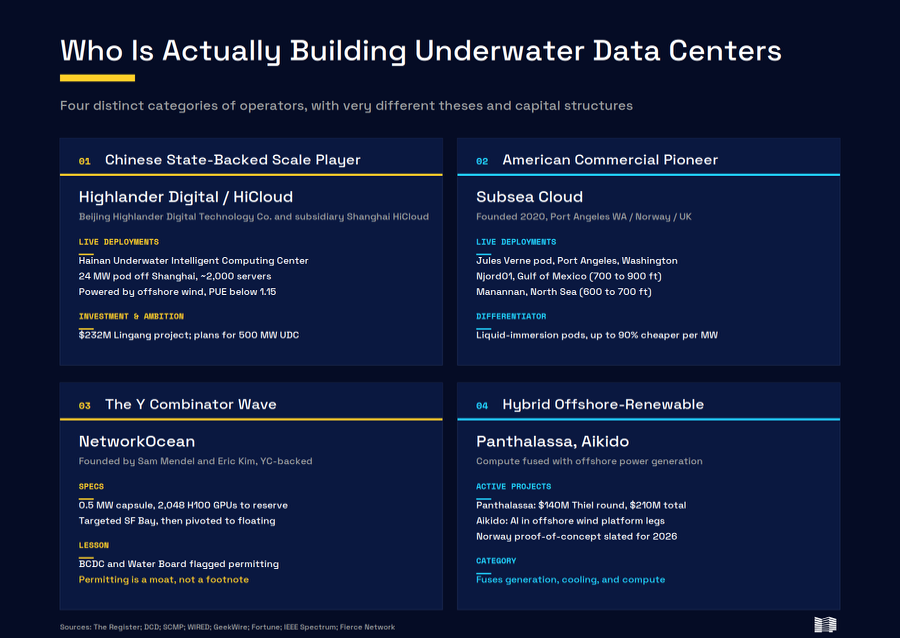

This is no longer theoretical. The active players fall into four buckets.

The Chinese state-backed scale player. Beijing Highlander Digital Technology and its subsidiary HiCloud have moved further than anyone else. Their Hainan facility was the world's first commercial underwater data center, and in 2025 they lit up a 24 MW pod off Shanghai powered directly by an offshore wind farm, housing roughly 2,000 servers at a reported PUE below 1.15. The Lingang project carries a total investment of about $232 million. The company has announced ambitions to build a 500 MW underwater facility, and China Telecom is now exploring “land + subsea” hybrid cloud as a productized offering. Whatever your view on Chinese tech policy, this is a working, paying, AI-workload-bearing system.

The American commercial pioneer. Subsea Cloud, founded in 2020, has taken the opposite design path from Microsoft, pressure-equalized, liquid-immersion pods rather than nitrogen-filled pressure vessels, and claims it can deploy 1 MW of capacity for as much as 90% less than a land-based equivalent. They have publicly described deployments at Port Angeles, Washington (Jules Verne), the Gulf of Mexico (Njord01), and the North Sea (Manannan). Their target customers span healthcare, finance, defense, and AI workloads.

The Y Combinator wave. NetworkOcean, founded by Sam Mendel and Eric Kim, came out of YC and announced 2,048 H100 GPUs available to reserve in a 0.5 MW capsule designed for the San Francisco Bay. They have since had to navigate regulatory backlash, with the Bay Conservation and Development Commission and the SF Regional Water Quality Control Board both flagging permitting concerns, and have leaned toward private and floating approaches. They are the cautionary tale and the leading indicator at the same time.

The hybrid offshore-renewable category. This is where I think the most interesting capital will flow. Panthalassa, funded in May 2026 with a $140 million round led by Peter Thiel at near-unicorn valuation, is building wave-powered floating AI data centers off Oregon. Aikido Technologies is putting AI servers inside the ballast legs of semi-submersible offshore wind platforms, with a Norway proof-of-concept slated for 2026. These are not subsea data centers in the Natick sense, they're a new category that fuses generation, cooling, and compute into a single offshore asset.

Figure 2. The four operator categories building underwater and offshore data centers, with very different theses, geographies, and capital structures.

Underwater vs. orbit vs. terrestrial

Every conversation about exotic data center locations eventually collapses into a comparison, so let me be direct about how I rank these.

Terrestrial is and will remain the workhorse. The vast majority of compute will live on land for the foreseeable future. But the marginal new gigawatt is getting harder, slower, and more expensive to permit every quarter. The Columbia Business School team studying data center real estate is right that we're in “the year of the data center,” and also right that the residual value risk in a 20-year hyperscale lease is nontrivial if the constraint shifts from “build more” to “build smarter.”

Orbital is the most exciting story and the longest-dated bet. Starcloud's pitch, unlimited solar, radiative cooling, no permits, no NIMBY, is genuinely compelling for inference workloads. But the unit economics depend almost entirely on Starship reaching commercial cadence at roughly $500 per kilogram of payload, which Starcloud's own CEO acknowledges is a 2028 to 2029 story at the earliest. The 2030s will likely produce real orbital compute. Today's investments are option value.

And yet the orbital story is sucking up almost all the oxygen. SpaceX went public in June 2026 in the largest IPO in history, raising roughly $75 billion and vaulting past a $2 trillion valuation, with orbital AI compute pitched directly in the prospectus as a challenge “only we can solve at scale.” That is an extraordinary amount of capital and attention riding on a thesis that SpaceX's own S-1 admits relies on “unproven technologies” that “may not achieve commercial viability,” and that Sam Altman has flatly called “ridiculous.” The physics is unforgiving: in vacuum there is no convection, so shedding a single megawatt of heat needs roughly 1,200 square meters of radiator, and a gigawatt of solar needs about a square mile of array in orbit.

Here is the part that should bother any disciplined allocator. The underwater approach solves the same terrestrial constraints, power, water, land, NIMBY, but it does so today, on the seabed, with hardware that has already run for years, at a fraction of the cost and with none of the launch-cadence dependency. Orbital compute is getting valued as if it were the obvious successor to the data center while underwater compute, which is demonstrably more feasible right now, is treated as a curiosity.

The attention is inversely correlated with the readiness. When the most feasible option is also the least hyped, that is exactly where a contrarian investor should be looking.

Underwater is the one that should already be a real asset class and isn't. The technical questions Microsoft answered with Natick, reliability, PUE, deployability, were answered favorably. The Chinese have demonstrated commercial scale. Subsea Cloud has shown the cost curve. Compared to orbit, underwater requires no new launch infrastructure. Compared to terrestrial, it sidesteps the two binding constraints of land and water. Yet venture capital has put far more dollars into space-based compute than into subsea compute. That's a market inefficiency.

Where the capital is actually going

The investor map tells you which thesis Wall Street and Sand Hill are willing to underwrite today.

Space: Starcloud has raised $200 million in total, with its $170 million Series A led by Benchmark and EQT and joined by Macquarie Capital, NFX, Nebular, Y Combinator, Adjacent, 776 Ventures, Fuse Ventures, Manhattan West, and Monolith Power Systems, plus angels including Dennis Muilenburg and Kevin Johnson. Aetherflux, Aethero, and Google's Project Suncatcher round out the orbital field.

Wave-powered offshore: Panthalassa's $210 million total to date includes Peter Thiel's Founders Fund, John Doerr, Marc Benioff's TIME Ventures, Max Levchin's SciFi Ventures, Lowercarbon Capital, and Gigascale Capital. This is the most credible LP roster in the entire offshore-compute thesis.

Underwater pure-play: Light. Subsea Cloud's backers are deep-sea industry investors and strategic operators. Nautilus Data Technologies has Keppel Data Centres in Singapore. Highlander/HiCloud is funded through Chinese state and provincial vehicles plus China Telecom. NetworkOcean came through Y Combinator. The signal here is that the underwater category is still being built by operators and strategic capital, not yet by traditional venture infrastructure funds. That's typically when prices are most attractive.

Figure 3. Disclosed funding flows reveal the inefficiency. Space and wave-powered offshore have attracted name-brand venture capital. Underwater pure-play remains the province of operators, strategics, and sovereign dollars.

What could break it

I don't want to make this sound easier than it is. Three challenges are real and underappreciated.

The first is environmental and regulatory friction. Even small temperature increases in coastal waters can trigger algal blooms and stress marine ecosystems, and the Bay Area regulators who pushed back on NetworkOcean were not being unreasonable. The precedent runs deep: Microsoft's own Project Natick was flagged by the California Coastal Commission in 2016 for an unpermitted 2015 deployment in San Luis Obispo Bay. Any startup in this space that treats permitting as a footnote will eventually become a cautionary tale. Any startup that treats permitting as a moat will quietly win.

The second is maintenance and supply chain. When a server fails 100 feet down, you can't walk over and swap it. Subsea Cloud cites a 4-to-16-hour service window per pod, which is plausible at small scale and harder at gigawatt scale. The deeper you go, the more you need ROVs, specialized vessels, and offshore engineering talent, a labor pool that overlaps almost entirely with the offshore oil and gas industry, which is itself capacity-constrained.

The third is geopolitical and security exposure. Subsea data centers depend on submarine cables for connectivity, and those cables are already being surveilled and, in some cases, sabotaged, with vessels interfering with offshore wind and communications infrastructure in northern Europe since Russia's invasion of Ukraine. Add high-value compute to the equation and the threat surface gets larger, not smaller. This is exactly why defense interest is real, and why Western sovereign capacity is going to matter.

What I'm watching

The window for venture-stage entry into this category is open right now, and it won't be open forever. A few specific things I'm watching for over the next 18 months:

The first commercial Subsea Cloud pod going live in the US under full regulatory daylight, which will set a permitting precedent for everyone behind them. Panthalassa's Ocean-3 pilot deployment, the first real test of whether wave power can carry an AI workload at meaningful capacity factor. Any US hyperscaler announcing a coastal subsea or offshore-floating partnership; Microsoft has the most institutional knowledge here and has been notably quiet since shuttering Natick in 2024. And real activity from sovereign wealth and infrastructure funds, who are the natural buyers of an asset class with 25-year design lives, contracted offtake, and renewable power coupling.

For real estate investors, the mental model shift is the important part. Data center real estate is still being underwritten as if the constraint is land entitlement and grid interconnect. The next leg of this build-out is going to be underwritten as if the constraint is environmental optionality, water, power, latency, and political license to operate. The teams who figure out how to assemble those four things in coastal and offshore environments are going to have a structural cost advantage that on-land developers cannot match.

Bibliography

- Axios. “Are SpaceX’s space data centers realistic?” Axios, June 12, 2026.

- Brightlio. “5 Largest Underwater Data Centers in the World.” Brightlio, March 2026. brightlio.com/underwater-data-centers.

- Capacity Media. “PayPal founder Peter Thiel backs $140m floating data centres powered by waves.” Capacity, May 2026.

- CNBC. “SpaceX IPO explained: The price is set, but retail allocation still up in the air.” CNBC, June 9, 2026.

- CNBC. “SpaceX’s historic IPO plans: Billions in losses and Musk’s massive ownership.” CNBC, May 20, 2026.

- Computer Weekly. “Microsoft hails heightened reliability of servers run in sub-sea datacentres.” September 15, 2020.

- Data Center Dynamics. “HiCloud’s offshore wind-powered underwater data center up and running off coast of Shanghai, China.” DCD, October 2025.

- Data Center Dynamics. “Project Natick: Microsoft’s underwater voyage of discovery.” DCD, 2020.

- Data Center Dynamics. “Space data center company Starcloud secures $170 million Series A.” DCD, April 2026.

- Data Center Dynamics. “Subsea Cloud announces three underwater data center projects.” DCD, September 1, 2022.

- Fortune. “Peter Thiel is leading investment in an ocean data center powered by waves—and the startup is reportedly worth $1 billion.” Fortune, May 14, 2026.

- GeekWire. “Data centers at sea: Oregon’s Panthalassa nets $140M led by Peter Thiel for wave-powered AI.” GeekWire, May 4, 2026.

- GeekWire. “Orbital AI: Seattle-area startup Starcloud hits $1.1B valuation to build space-based data centers.” GeekWire, March 30, 2026.

- IEEE Spectrum. “This Offshore Wind Turbine Will House a Data Center Underwater.” IEEE Spectrum, March 2026.

- International Energy Agency. Energy and AI. Paris: IEA, 2025.

- Latitude Media. “Are Thiel-funded floating data centers enough to make wave energy pencil?” Latitude Media, May 2026.

- Microsoft. “Project Natick Phase 2.” natick.research.microsoft.com (accessed June 2026).

- Microsoft Source. “Microsoft finds underwater datacenters are reliable, practical and use energy sustainably.” September 14, 2020.

- Renewable Energy Magazine. “Aikido launches offshore datacenter technology to deploy GW-scale, sovereign AI compute.” March 2026.

- SpaceNews. “Starcloud achieves unicorn status with $170 million raise for orbital data centers.” SpaceNews, April 23, 2026.

- Scientific American. “SpaceX IPO valuation depends on Starship and orbital AI data centers.” June 2026.

- South China Morning Post. “China turns to offshore wind farms, subsea data centres to ease AI computing bottleneck.” SCMP, April 2026.

- The Next Web. “SpaceX S-1 warns orbital AI data centres may not be viable.” TNW, May 2026.

- The Register. “Commercial underwater datacenter goes online this year.” The Register, September 1, 2022.

- Tom’s Hardware. “China says ‘world’s first’ offshore wind-powered underwater data center has entered full operation.” Tom’s Hardware, May 2026.

- TechCrunch. “Starcloud raises $170 million Series A to build data centers in space.” TechCrunch, March 30, 2026.

- WIRED. “An underwater data center in San Francisco Bay? Regulators say not so fast.” WIRED, September 11, 2024.