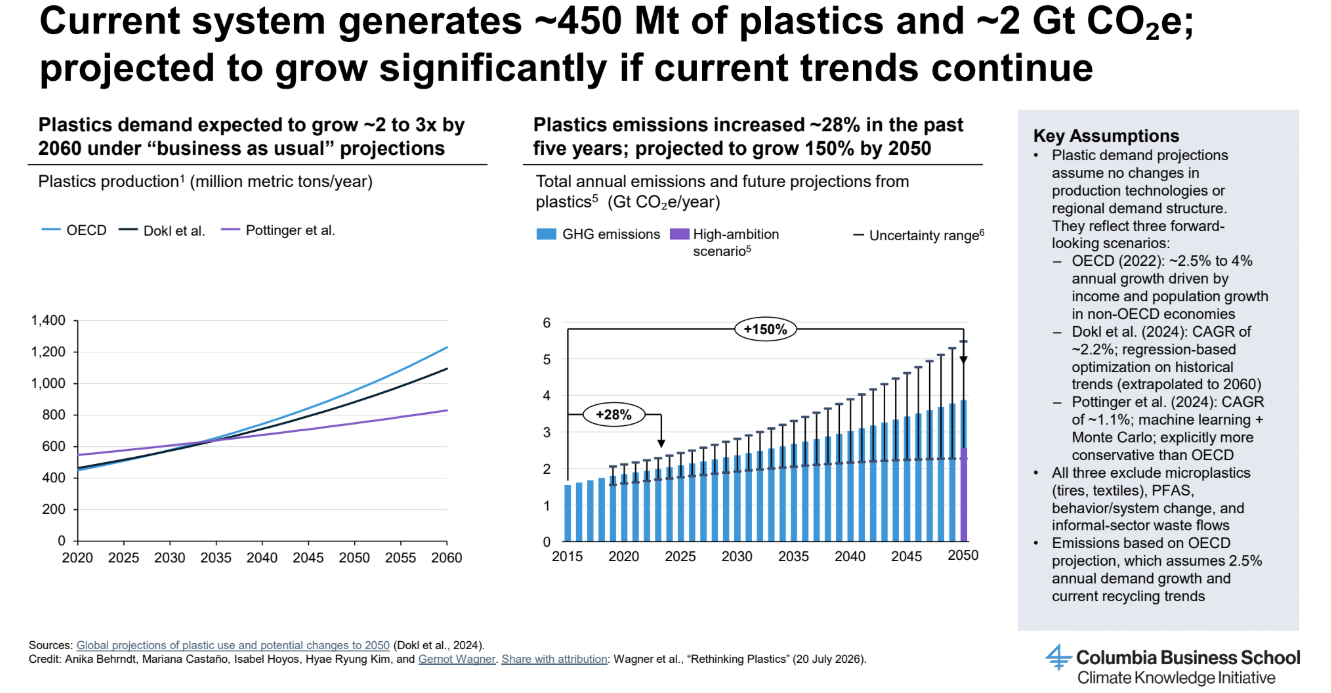

From 1950 to 2025, global plastic production multiplied from ~1.5 million to ~450 million metric tons—one of the fastest material expansions in industrial history. It’s become embedded across nearly every sector of the global economy, underpinning food systems, healthcare, mobility, and manufacturing. And the low cost of plastic has entrenched its use even in applications with limited functional necessity, like disposable cutlery, individually wrapped produce, and redundant packaging.

Structural lock-ins ensure continuous demand for virgin fossil feedstocks, while waste management costs are externalized from the petrochemicals industry onto municipalities and consumers.

Today, around 10 percent of the world’s oil production goes toward plastics manufacturing. As the transport sector electrifies, the relative importance of petrochemicals is bound to increase, though corporate strategies differ widely. If demand for petrochemicals remains unchecked, it will become the new anchor of fossil fuel consumption, sustaining long-term demand.

Beyond fossil fuel lock-in, plastic production and disposal account for around 5 percent of global greenhouse gas emissions. And this calculation excludes emerging evidence that plastic pollution, particularly microplastics, may impair natural carbon sinks—suggesting the true climate cost of plastics to be systematically underestimated.

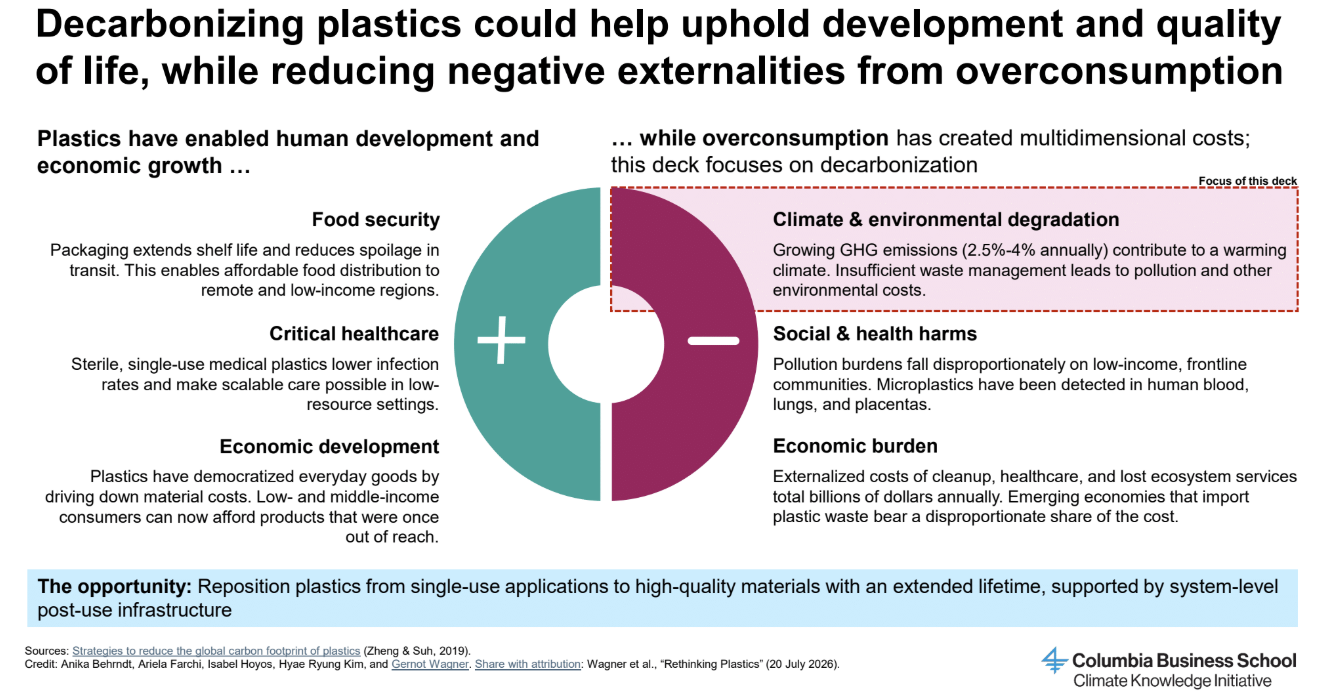

Plastics are also a well-known pollution crisis: They make up more than 85 percent of marine litter, undermining ecosystem health and biodiversity. Yet solutions to address the dual challenges of pollution and emissions reduction remain fragmented. Recent international negotiations on a global plastics treaty stalled in 2025, underscoring the difficulty of reconciling competing national interests, particularly between countries reliant on petrochemical revenues and those bearing the environmental and climate costs of plastic pollution.

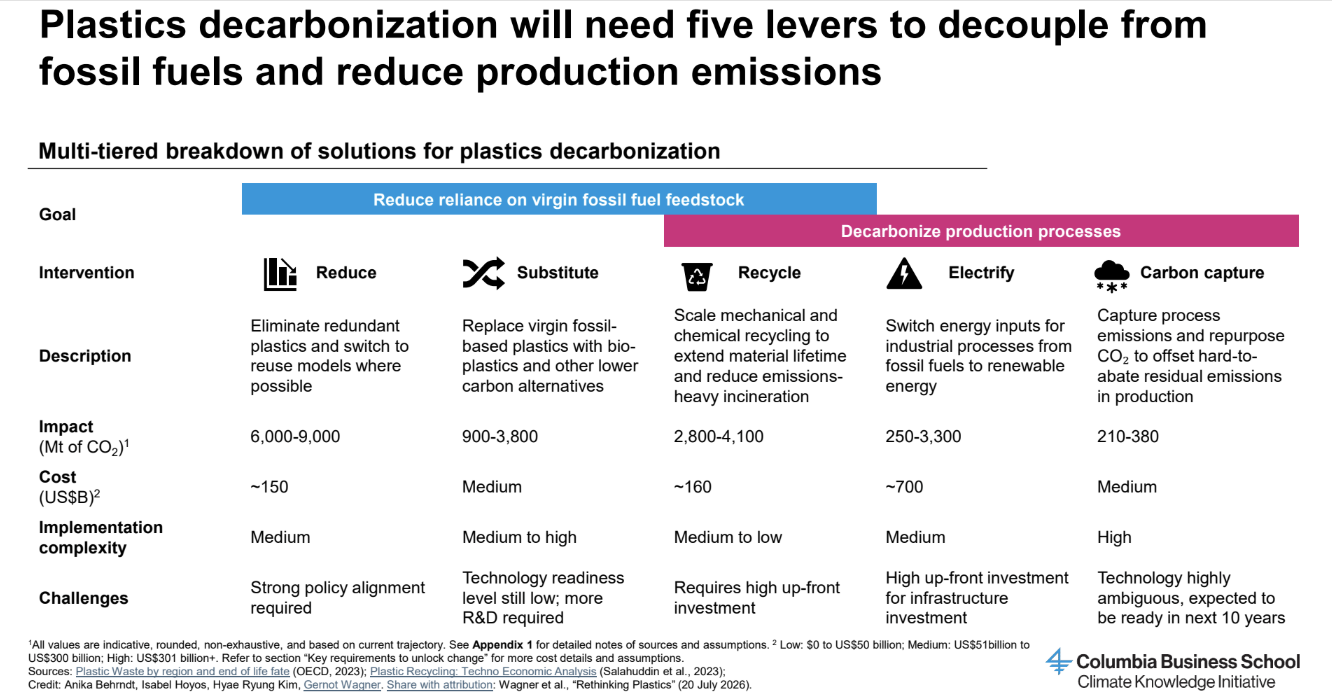

Solutions range from demand reduction to recycling, substitution, production electrification, and carbon capture, utilization, and storage (CCUS), which often compete rather than complement one another.

Key Insight 1: To abate plastic’s emissions, reduce demand first, then decarbonize residual production

The plastics industry’s emissions derive from the extraction of fossil fuels, the petrochemical production process, and emissions associated with plastic waste and end-of-life treatments. Tackling each element is important, pointing to solutions from material substitution to electrification to recycling to CCUS. But there is one underlying driver: demand.

Demand reduction

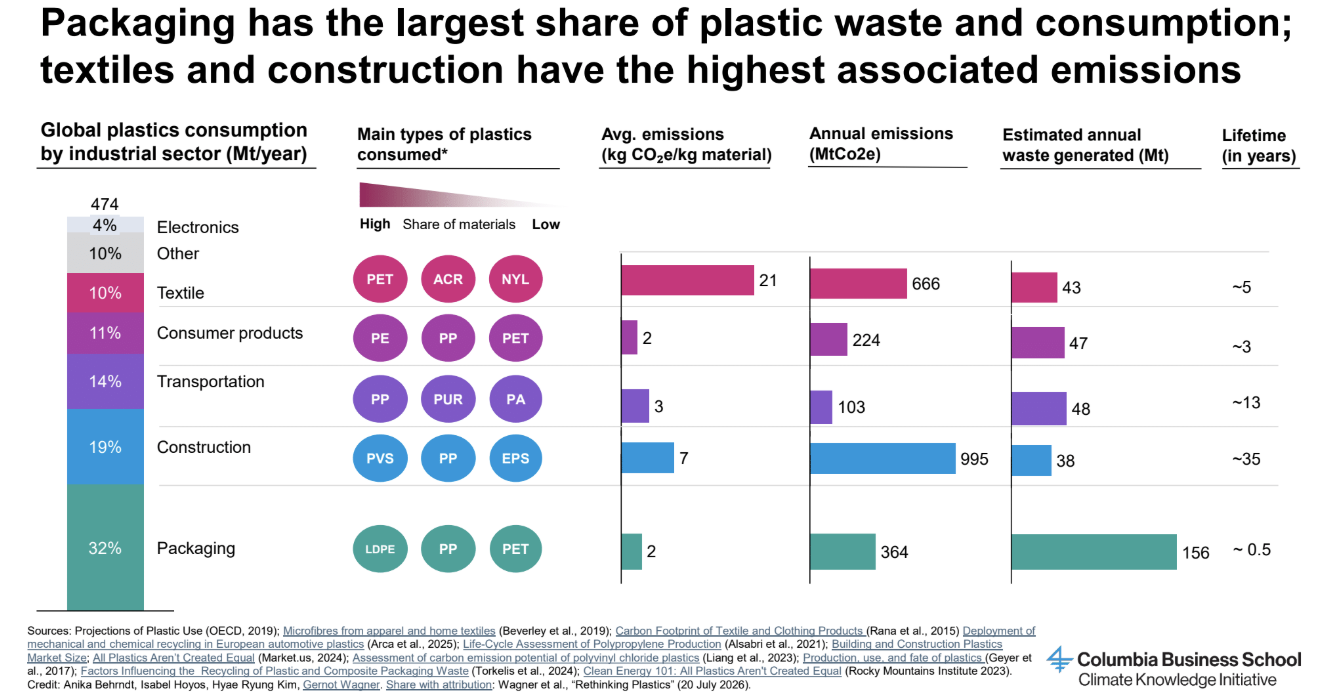

Approximately half of all plastics are used in packaging and other short-lived applications often designed to become waste within days or weeks.

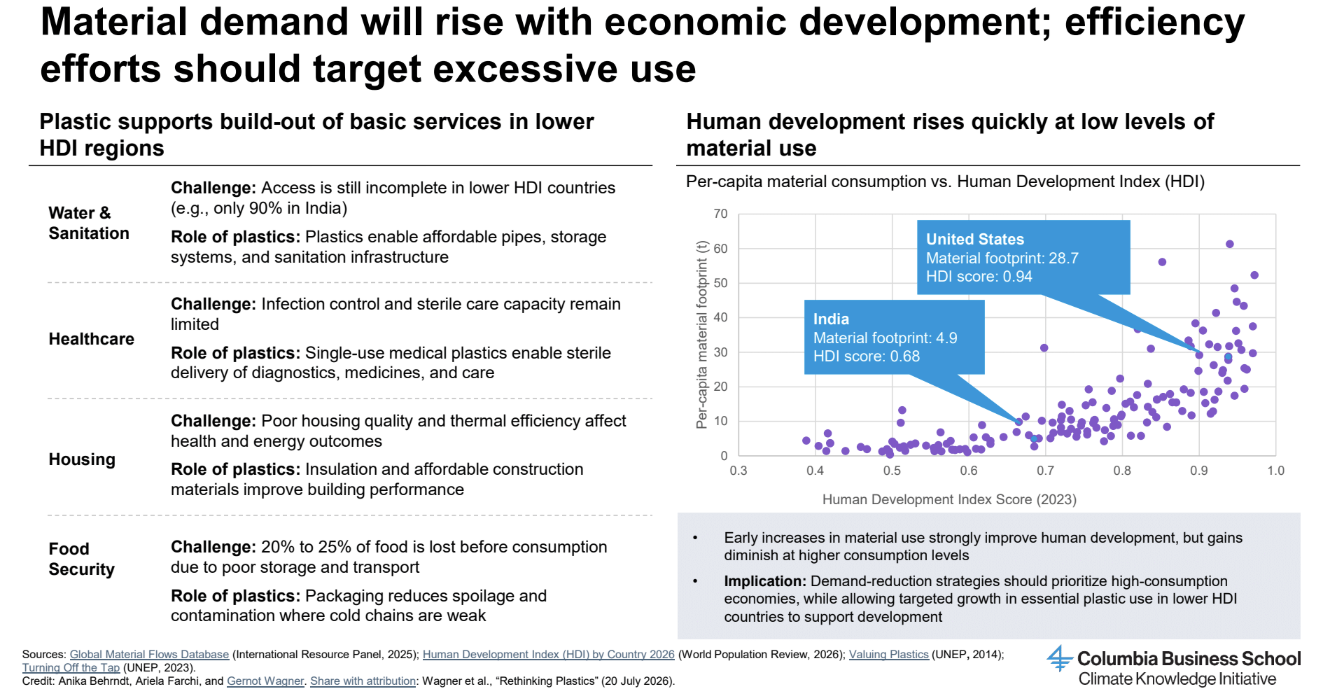

Reducing demand for short-lived plastics, through elimination, reuse, and new delivery models, represents one of the most immediate opportunities for emissions reductions. However, the case for demand reduction is geographically differentiated. In many low-income countries, plastics play an essential role in enabling access to food, healthcare, and basic services. Demand-side interventions should focus on curbing unnecessary or avoidable use, predominantly in developed countries.

Materials used in automotive, aerospace, medical devices, and renewable energy infrastructure, for instance, offer greater functional necessity and margin stability than commodity packaging. Indeed, demand reduction in low-value applications can help reorient the plastics industry toward higher-value materials and longer-lived products.

Regulatory measures like packaging standards and material reduction targets are critical to set a baseline, while reuse models depend on enabling infrastructure, including collection, cleaning, and reverse logistics systems.

But behavioral friction remains a key barrier. Returning products or participating in reuse systems introduces additional effort for consumers. Evidence suggests that financial incentives are among the most effective tools to overcome this friction. Well-designed deposit-return systems, where deposits are sufficiently high to be salient, have consistently demonstrated high return rates, indicating that behavior responds more strongly to economic signals than to awareness campaigns or other “nudges” alone.

Material substitution

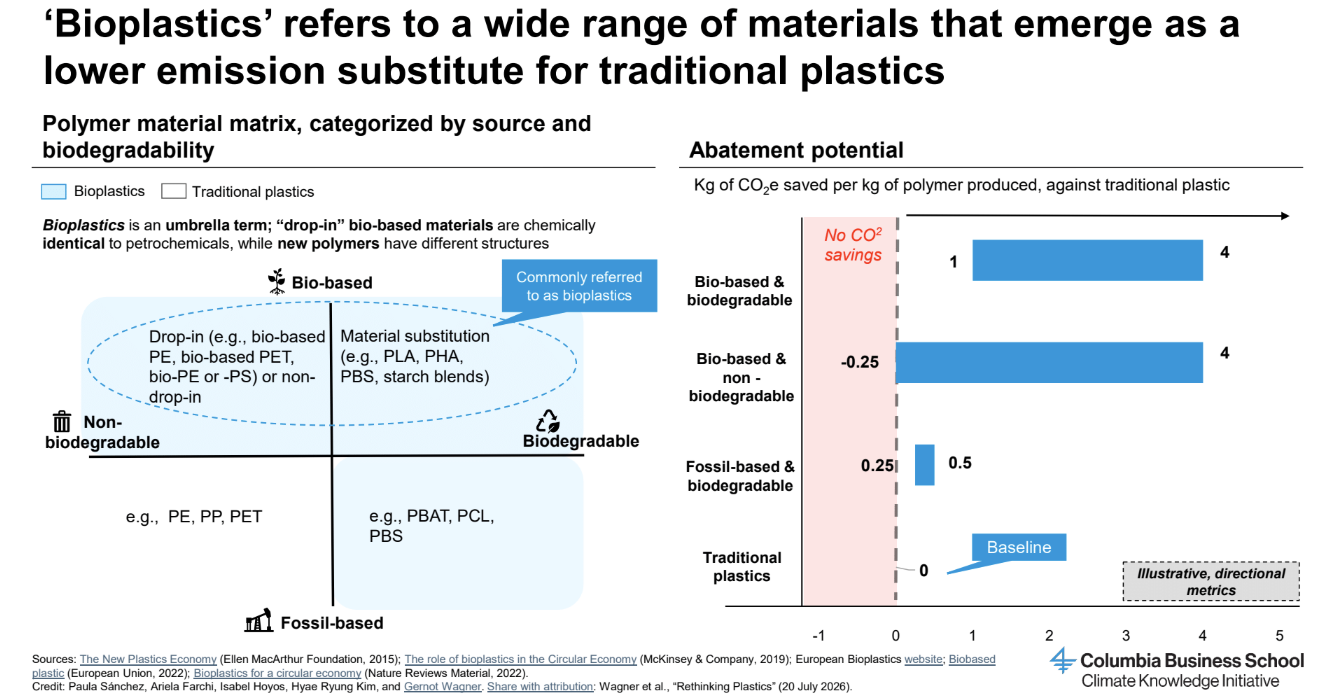

Substituting fossil-based plastics with alternative materials is often framed as a straightforward solution. Bioplastics, from algae-based products to next-generation biomaterials, promise continued consumption habits without reliance on the fossil fuels and, in some cases, better end of life through biodegradability or composting. Reality, however, is far more complex.

Bioplastics is an umbrella term for materially different polymers distinguished by feedstock origin (bio-based vs. fossil-based) and end-of-life behavior (biodegradable vs. non-biodegradable). Many bioplastics address carbon, some address waste, but relatively few deliver substantial benefits across both dimensions under current production and waste management systems.

Scaling the alternative materials market faces three key constraints: relative high cost; relative underperformance in durability, porosity, and versatility; and feedstock competition. Not to mention, environmental benefits are conditional on appropriate waste management—biodegradable materials, for example, deliver advantages only where dedicated collection and industrial composting systems exist.

Recycling

Recycling plays an important role in reducing emissions and material demand, but structural constraints limit its ability to address plastic waste and emissions on its own.

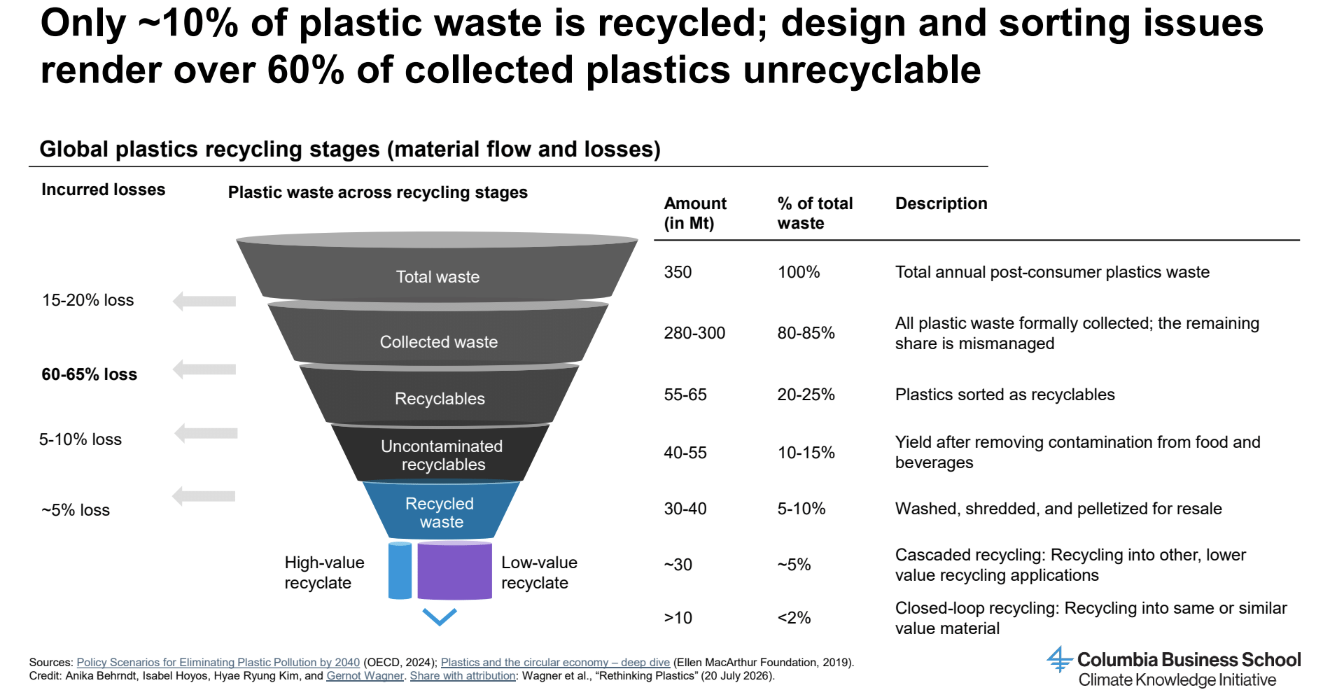

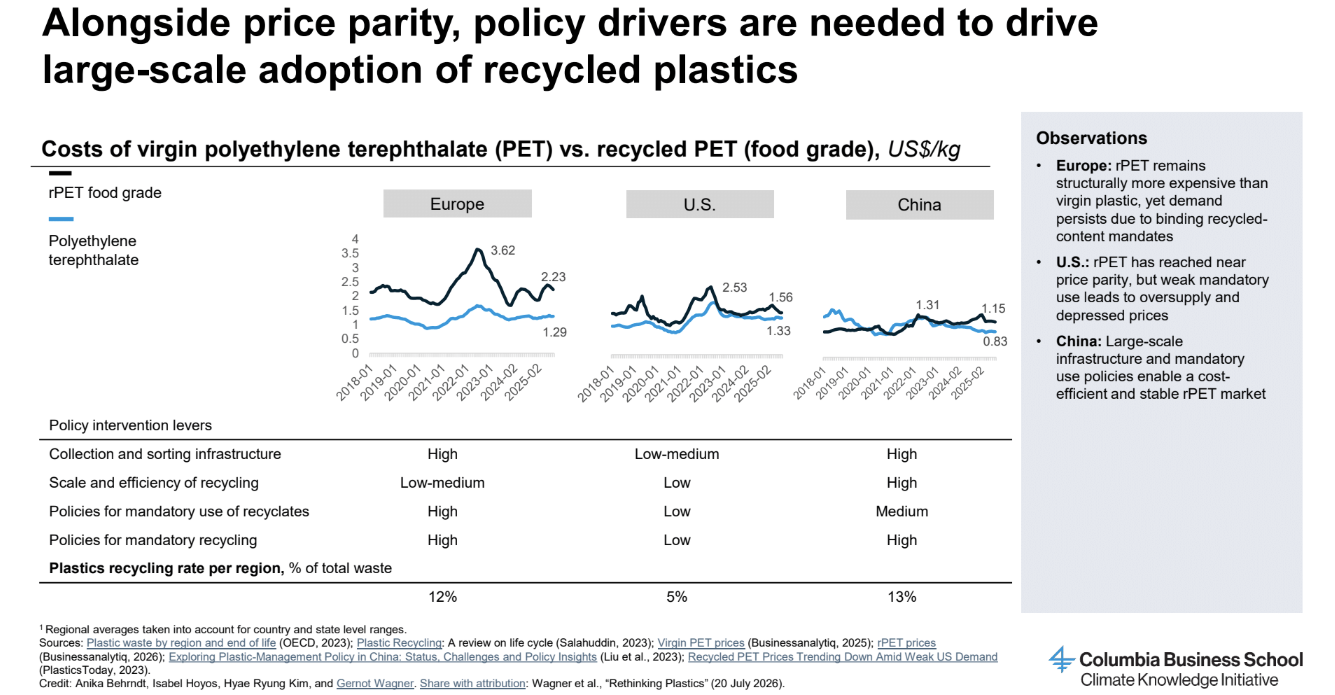

Only around 10 percent of global plastic waste is currently recycled, partly driven by misleading labeling: “recyclable” often refers to technical feasibility rather than actual recycling outcomes.

Collection and sorting infrastructure remains inadequate in many regions, particularly in lower income areas. And recyclates often struggle to compete with virgin plastics on cost, weakening demand. Material degradation also limits the number of times plastics can be recycled, which prevents an indefinitely closed loop and delivers diminishing returns.

Scaling recycling therefore depends on two system conditions: achieving sufficient scale on the supply side, and ensuring stable demand and predicable revenues for recycling operators.

Electrification and carbon capture

Even under ambitious demand reduction and circularity scenarios, residual fossil-based plastic production will still need to be addressed, and industrial electrification will be a key decarbonization pathway.

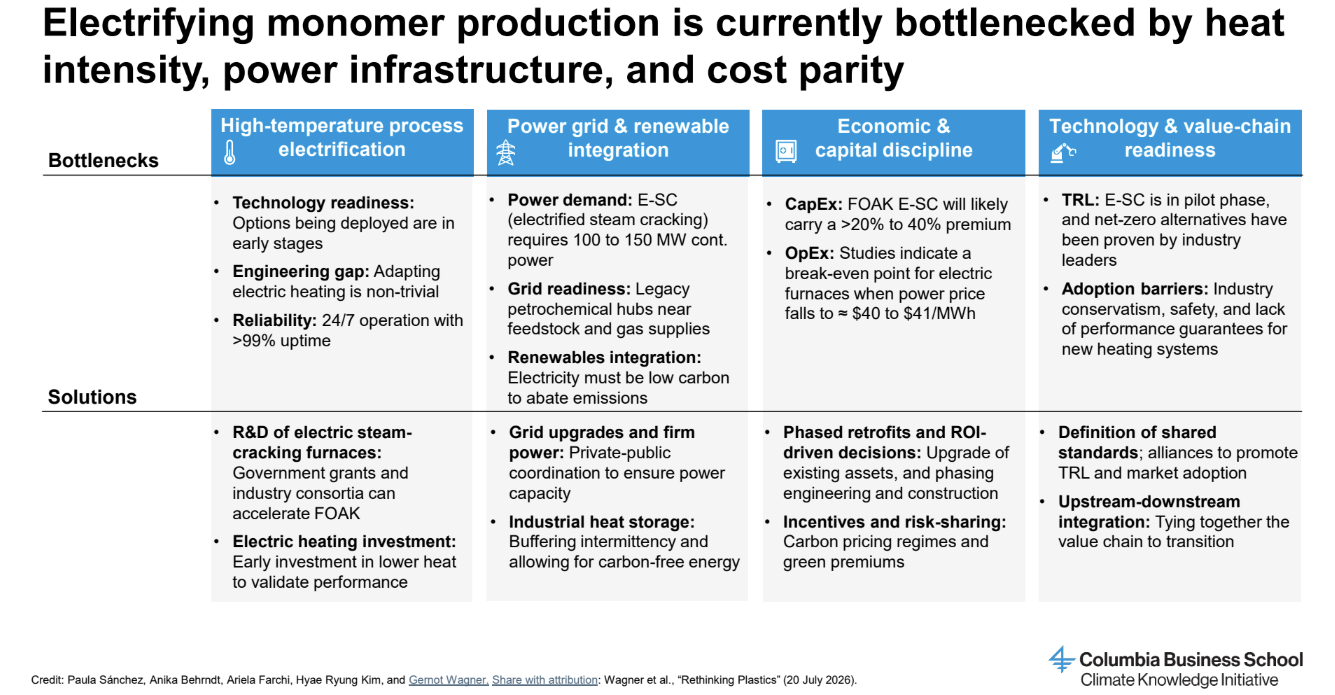

Over 50 percent of plastics-related emissions are thermal, particularly in monomer production. Steam cracking alone accounts for ~25 to 50 percent of production emissions. Electrifying these processes, however, remains challenging due to heat intensity, the need for power infrastructure, cost, and the technological readiness of electrified production plants.

Point-source CCUS can abate remaining production emissions that cannot be eliminated through electrification alone. In monomer production, CCUS applied to steam crackers can capture up to 90 percent of point-source emissions, with capture at waste-to-energy plants reaching similar rates. Deployment remains highly dependent on stable carbon pricing, regulatory clarity, and shared CO₂ transport and storage infrastructure.

Given high costs and system dependencies, CCUS is best understood as an enabling but conditional solution, which is critical for addressing residual emissions but not a substitute for upstream interventions.

Key insight 2: Markets will not correct plastic overproduction on their own because virgin fossil-based plastics are structurally underpriced, making policy intervention essential

Plastic overproduction is not simply a function of consumer demand but of distorted market incentives. Virgin fossil-based plastics often do not reflect the full environmental costs associated with their production, use, and disposal, and as a result, markets alone are unlikely to drive a meaningful shift toward lower emission alternatives.

Several structural factors reinforce this price advantage. Plastics are derived from abundant fossil feedstocks, often supported, directly or indirectly, by fossil fuel subsidies (which reached US$1.3 trillion in 2022 in explicit support, rising to roughly US$7 trillion when unpriced externalities are included). Their chemical properties make them versatile, lightweight, and easy to process at scale, also reducing both production and transportation costs. At the same time, the environmental externalities associated with plastics, most notably carbon emissions and pollution, remain largely unpriced.

This mispricing has direct implications for market behavior. Even where lower-emission alternatives exist, they struggle to compete on cost and quality perceptions. The case of recycling illustrates this clearly: Despite the availability of recyclates at competitive prices in markets such as the United States, demand remains weak. Many companies continue to favor virgin materials due to their consistency and perceived reliability, leaving recycled materials without stable offtake markets. As a result, recycling systems fail to scale, not due to lack of supply but because of lack of demand.

The underlying lesson is clear: Without policy intervention to create demand and correct price signals, markets will not naturally transition toward circular or low-carbon materials. Companies will shift away from virgin plastics only if it either reduces costs or increases revenues, conditions that are rarely met under current market structures.

A first set of interventions targets price correction, including carbon pricing, taxes on virgin resin, and the removal of fossil fuel subsidies. These measures help internalize externalities and narrow the cost gap between virgin and alternative materials.

A second set focuses on demand creation. Instruments such as recycled content mandates, extended producer responsibility (EPR) schemes, and public procurement standards create guaranteed markets for circular materials, reducing investment risk and enabling scale. Without such mechanisms, supply-side investments, such as recycling capacity, will remain underutilized.

A third set of policies acts as system enablers, supporting infrastructure and standardization. Investments in collection, sorting, and recycling systems, alongside harmonized packaging standards and labeling, improve material flows and reduce processing costs.

Finally, consumer-facing incentives can play a decisive role in overcoming behavioral barriers. Deposit-return schemes provide a clear example: In Germany, a deposit of €0.25 per bottle has driven return rates of up to ~98 percent, effectively closing the loop for beverage containers. In contrast, U.S. systems, where deposits are typically around $0.05 to $0.10 and implemented only in select states, achieve significantly lower return rates. The difference is not awareness but incentive design: When the financial signal is meaningful, behavior follows.

Regulatory momentum is emerging unevenly across regions. Europe currently leads in plastics regulation, with measures such as the EU Single-Use Plastics Directive, strengthened EPR systems, and the recently adopted Packaging and Packaging Waste Regulation (PPWR) introducing recycled-content targets, design standards, and restrictions on certain single-use products. These policies are already incentivizing investments in recyclability, recycled materials, and alternative polymers.

In the United States, plastics policy remains more fragmented, but momentum is increasing at the state level. California’s SB 54 requires all packaging to be recyclable or compostable by 2032 and mandates both plastic packaging reductions and higher recycling rates, while states such as Maine, Oregon, and Colorado have introduced EPR schemes for packaging.

When regulation alters the economics of materials, it can create incentives for innovation. Reflecting this dynamic, nearly half of global patent applications related to plastics waste management since 2015 have originated in Europe, according to the European Patent Office.

Ultimately, correcting the plastics system is not a question of technological feasibility but of incentive design. As long as virgin plastics remain artificially cheap, producers will have limited reason to redesign products, invest in circular systems, or shift feedstocks. Policy intervention is therefore not complementary but foundational to any meaningful transition.

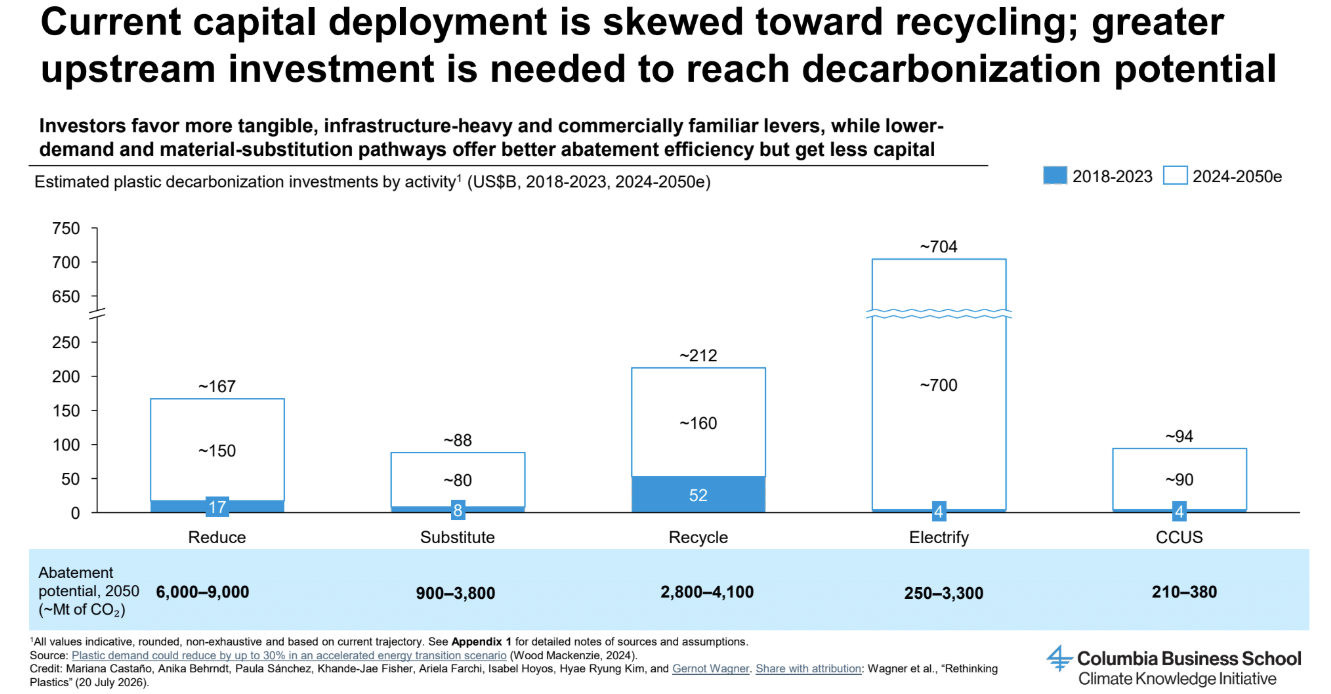

Key insight 3: Circular systems could reduce plastics’ emissions by 60 to 70 percent, but scaling them requires coordinated infrastructure and large-scale capital deployment

Circularity is best understood as a system condition: Materials remain in use at high value, and demand for virgin production is structurally reduced. This could reduce plastics-related emissions by ~60 to 70 percent but requires significant infrastructural investment.

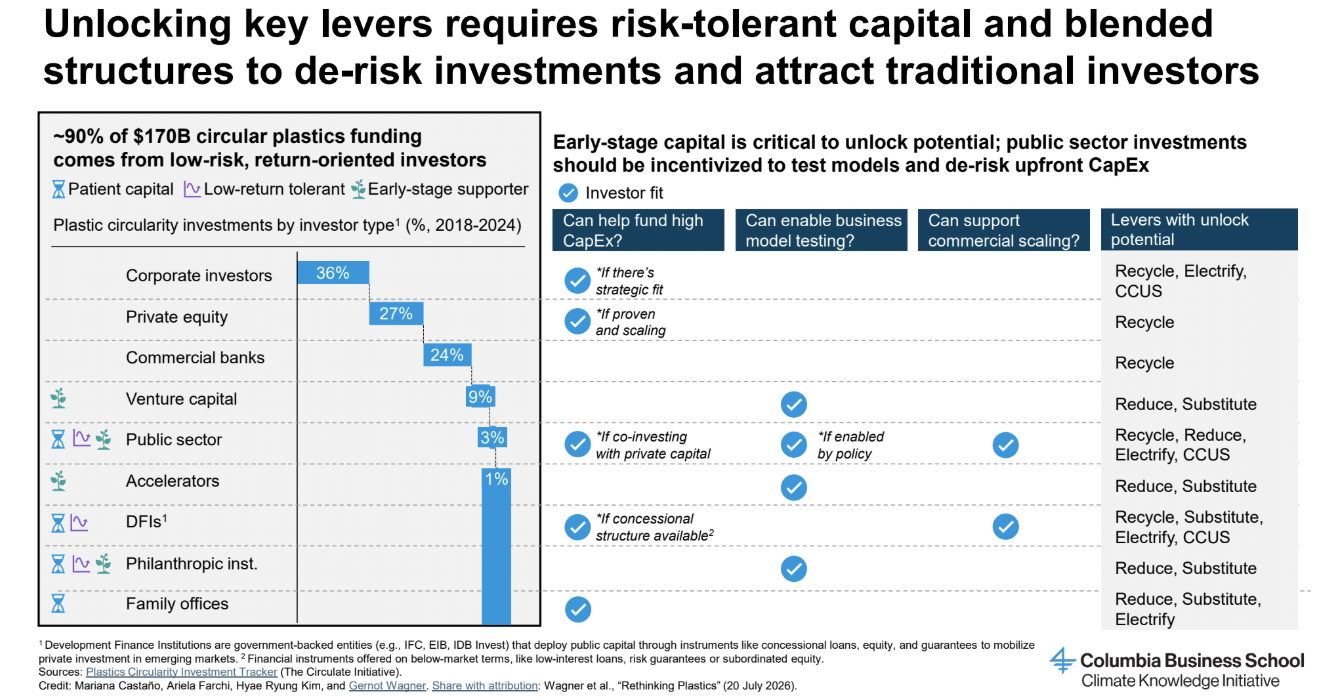

A key structural issue is that capital allocation is misaligned with where investment is most needed. An estimated ~85 to 90 percent of funding in plastics circularity comes from low-risk, return-oriented investors, including corporates (~36 percent), private equity (~27 percent), and commercial banks (~24 percent). In contrast, early-stage and risk-tolerant capital remains scarce, with venture capital contributing only ~9 percent and public or concessional actors (public sector, DFIs, philanthropy) together accounting for less than ~10 percent.

As a result, capital tends to flow toward more mature, lower risk segments (e.g., mechanical recycling in developed markets), while higher risk but system-critical areas—including collection infrastructure, advanced sorting, reuse systems, and emerging recycling technologies—remain underfunded.

Although the barriers differ across reduction and reuse models, material substitution, and recycling pathways, they share common financing challenges: high upfront capital requirements, uncertain revenues, long payback periods, and dependence on policy-driven revenue streams. This creates a structural financing gap, where projects are viable from a system perspective but unattractive under conventional risk-return frameworks.

Closing this gap requires a shift toward blended finance and layered capital structures, where different types of capital play complementary roles. Public and concessional capital de-risk early-stage investments, and catalytic capital supports business model validation and early commercialization.

Ultimately, circular systems will not scale through incremental market adjustments alone. They require a reconfiguration of capital flows, where risk-tolerant and public capital plays a foundational role in building the infrastructure and markets that private investors can later scale. Without this shift, circularity risks remaining technically feasible but financially out of reach.

From fragmentation to system transition

Plastics are not simply a materials challenge but a system-level one, embedded in how economies produce, consume, and allocate capital. The challenge is not a lack of technical pathways but a misalignment of incentives, capital, and infrastructure to enable them at scale.

If virgin plastics remain structurally underpriced and circular systems lack stable demand and revenue certainty, capital will continue to flow toward linear, fossil-based production. Correcting this requires policy frameworks that reshape price signals, create demand for circular materials, and de-risk investment across the system.

Ultimately, the transition is not about eliminating plastics altogether but about redefining their role within the economy. Plastics will remain essential in many applications, but their production, use, and end-of-life treatment must be fundamentally restructured.

Without this shift, plastics could become an increasingly important source of fossil fuel demand as other sectors, particularly transport, electrify. With it, they represent one of the most actionable levers for reducing emissions across industry, materials, and consumption systems.