While the office market often dominates discussions of distress, the true epicenter of pain in New York is the nearly one million rent-stabilized apartments across the city. This segment of the market grapples with distinct and severe risks, both from the specter of increased regulation and the perils of past deregulation, demanding a nuanced understanding from any investor attempting to navigate this treacherous terrain. It's a true catch-22, where owners face significant challenges whether or not their units were deregulated.

The History of Regulation, 2019 HSTPA, and the Rent Freeze

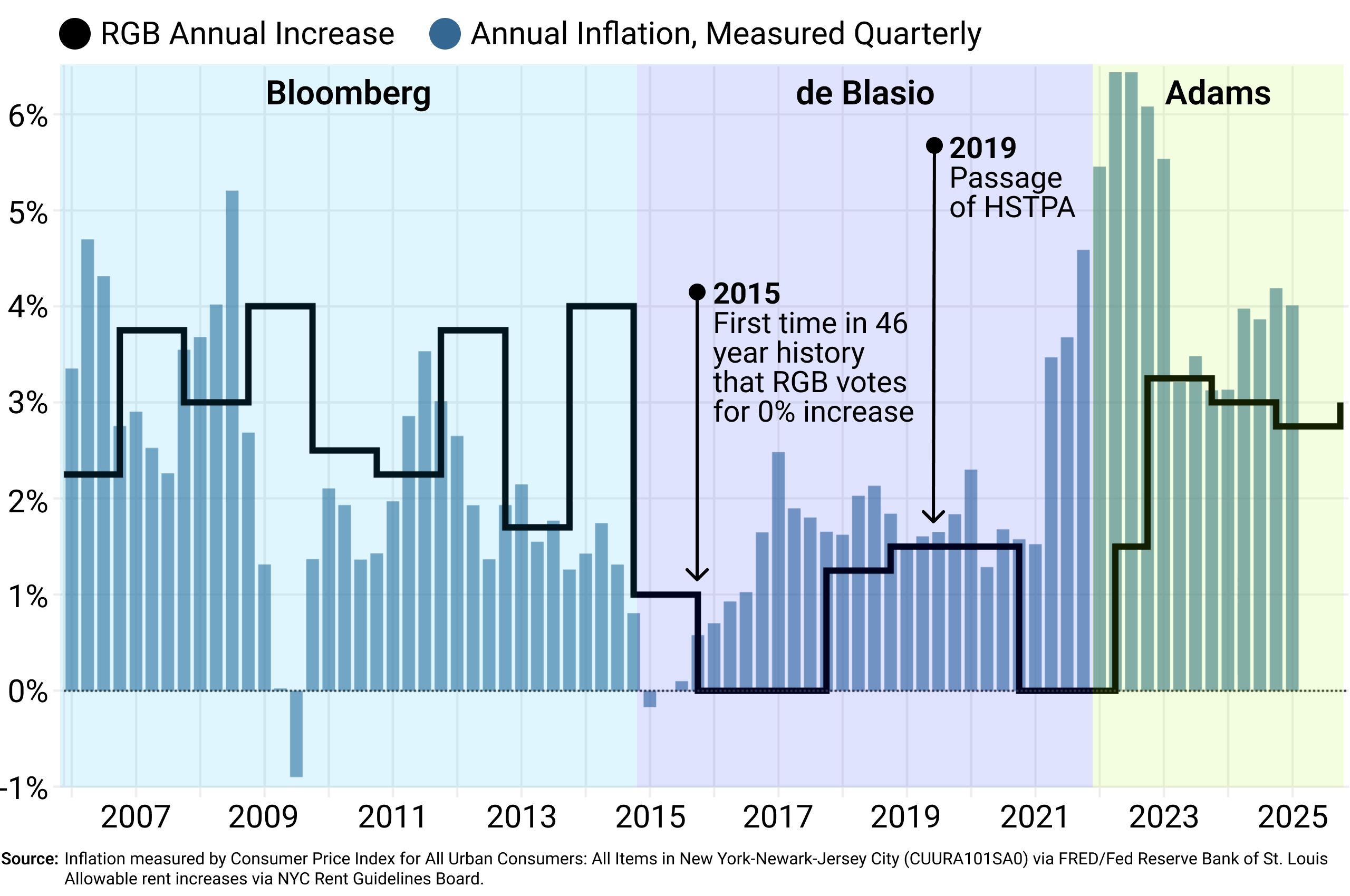

The modern framework of rent stabilization was largely shaped in the latter half of the 20th century, with the establishment of the NYC Rent Guidelines Board (RGB) in 1969. For decades, a viable business model existed for investors: acquire rent-regulated buildings and pursue a path to deregulation, unlocking the significant value differential between regulated and market-rate rents. Regulated rents are adjusted annually by the RGB, and now this has come into focus as Democratic nominee Mamdani has vowed to freeze regulated rents. The recent history of rent increases compared to inflation provides meaningful context:

Rent Increases vs. Inflation

In 2019, the state legislature passed — and then Governor Cuomo signed — the Housing Stability and Tenant Protection Act (HSTPA). The HSTPA effectively eliminated the pathways to income growth that had been the cornerstones of rent-stabilized investment theses for a generation of real estate professionals. The law severely curtailed the ability to raise rents through vacancy bonuses, individual apartment improvements (IAIs) and major capital improvements (MCIs). The result has been a dramatic increase in deferred maintenance, a spike in insurance premiums, and a growing trend of "warehousing" units off the market as owners wait out potential new legislative changes or decline to renovate units without the means to efficiently recoup those investments.

The Weight of Debt in a Stagnant Market

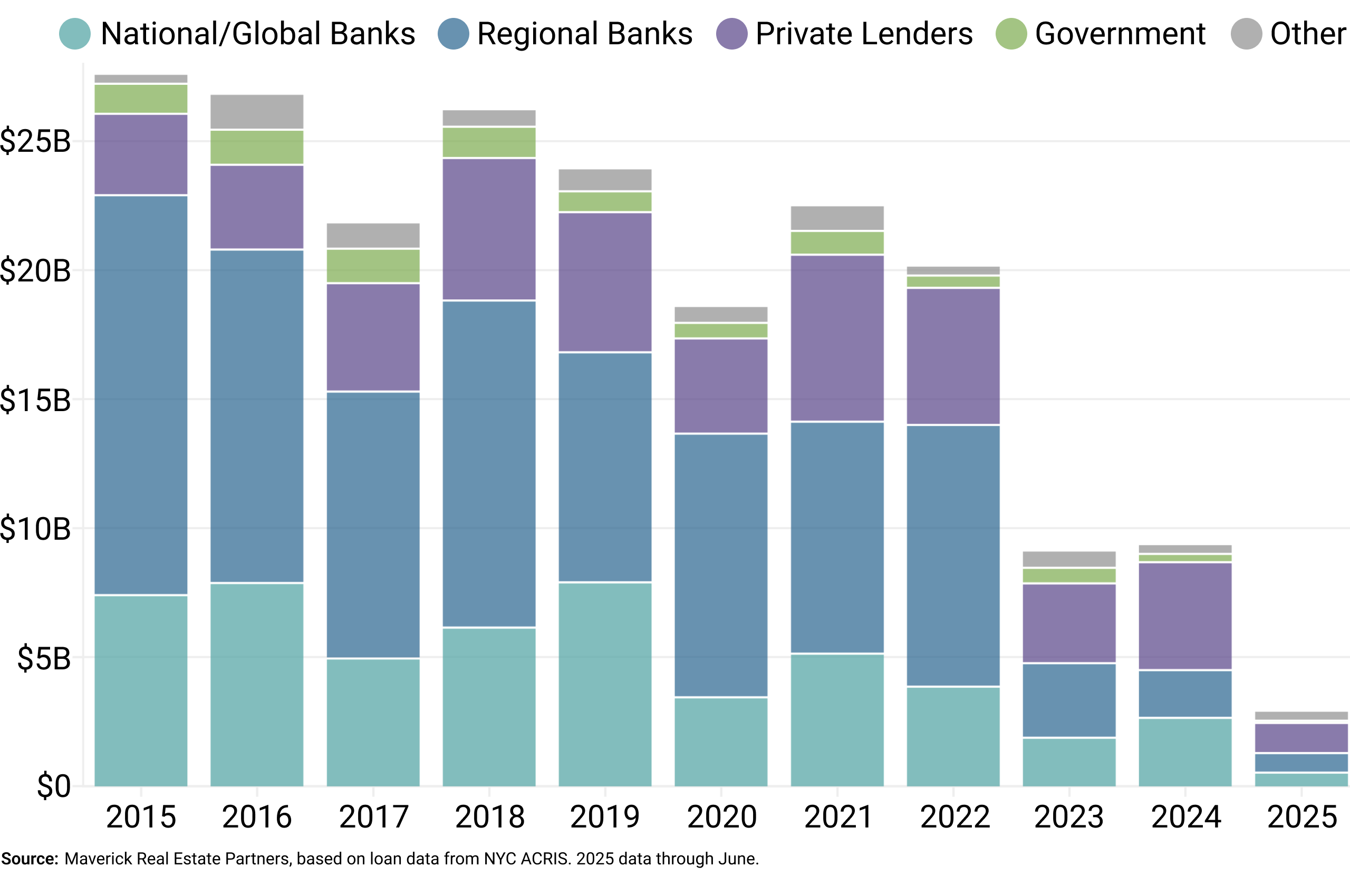

The HSTPA’s impact has been magnified by the enormous amount of debt encumbering these assets. There is $105 billion of debt outstanding, spread across 21,000 loans secured by 26,000 rent-stabilized buildings (excluding 421a properties). The primary lenders in this space have historically been regional banks, and with most of them now exiting the market, the availability of debt financing has plummeted:

Rent-Stabilized Loan Originations in New York City

This reduced liquidity means fewer owners are able to refinance. Banks are holding loans for longer, with the average age of a loan on a typical bank's balance sheet nearly doubling from under three years in 2015 to over five years today. This balance sheet buildup creates risk and prevents banks from originating new, higher-quality loans.

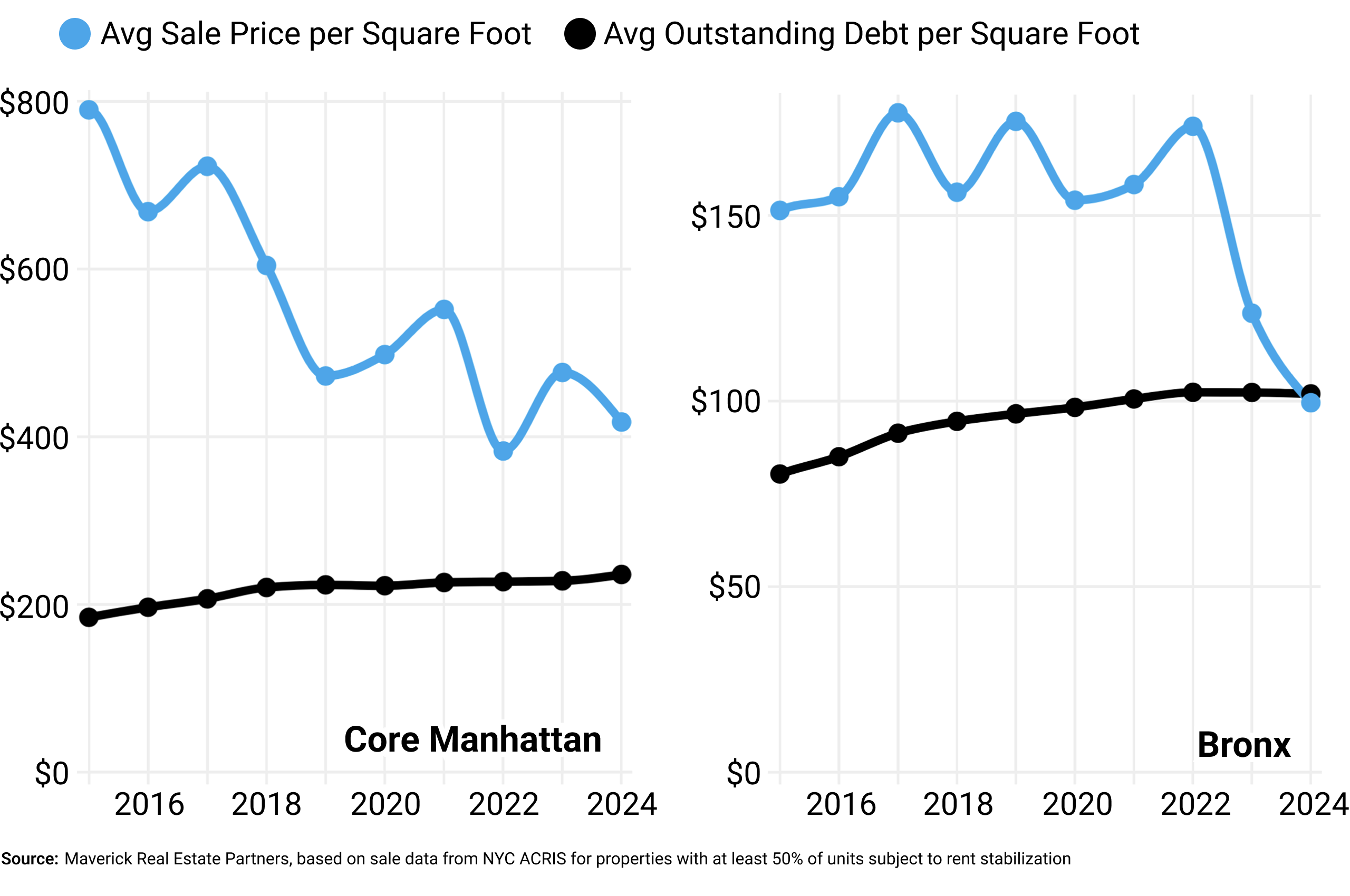

The erosion of equity is most starkly illustrated when comparing the average sales price per square foot to the outstanding debt per square foot. In the Bronx, for instance, the average sales price has fallen to a level that is roughly on par with the average debt, meaning that a significant portion of the buildings in the borough likely have zero or negative equity:

The Perils of Regulation: The 100% Rent-Stabilized Fortress

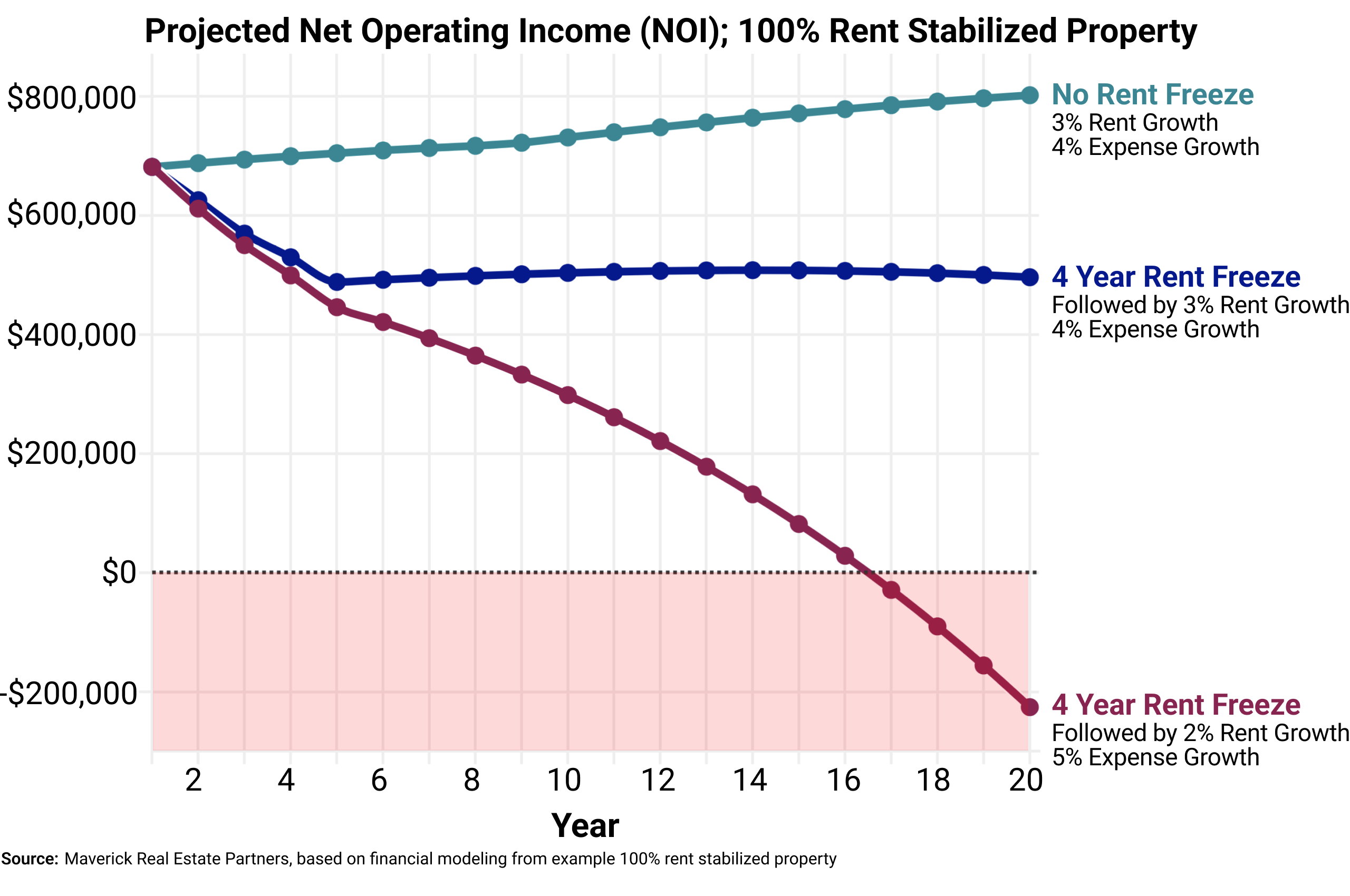

For buildings that are entirely or almost entirely rent-stabilized, the primary risk is a slow and steady bleed of net operating income (NOI). With revenue growth tightly capped by the RGB, even modest increases in operating expenses can have a devastating impact on the bottom line. This is particularly true in boroughs like the Bronx, where expense margins are already thin.

The political climate adds another layer of risk. A mayoral administration committed to a "rent freeze" could, by appointing a sympathetic RGB, effectively halt all rent increases for a four-year term. The impact of such a policy would be catastrophic for many owners. A realistic scenario for a 100% rent-stabilized building in the Bronx shows that a four-year rent freeze, followed by a return to modest 3% annual rent growth, would still cause a significant and permanent reduction in NOI. A more draconian, but entirely plausible, scenario of a four-year freeze followed by 2% rent growth and 5% expense growth would see the property's NOI turn negative within 16-17 years, rendering the property worthless. The graph below highlights this dynamic on a recent transaction that was underwritten, but not acquired, by Maverick:

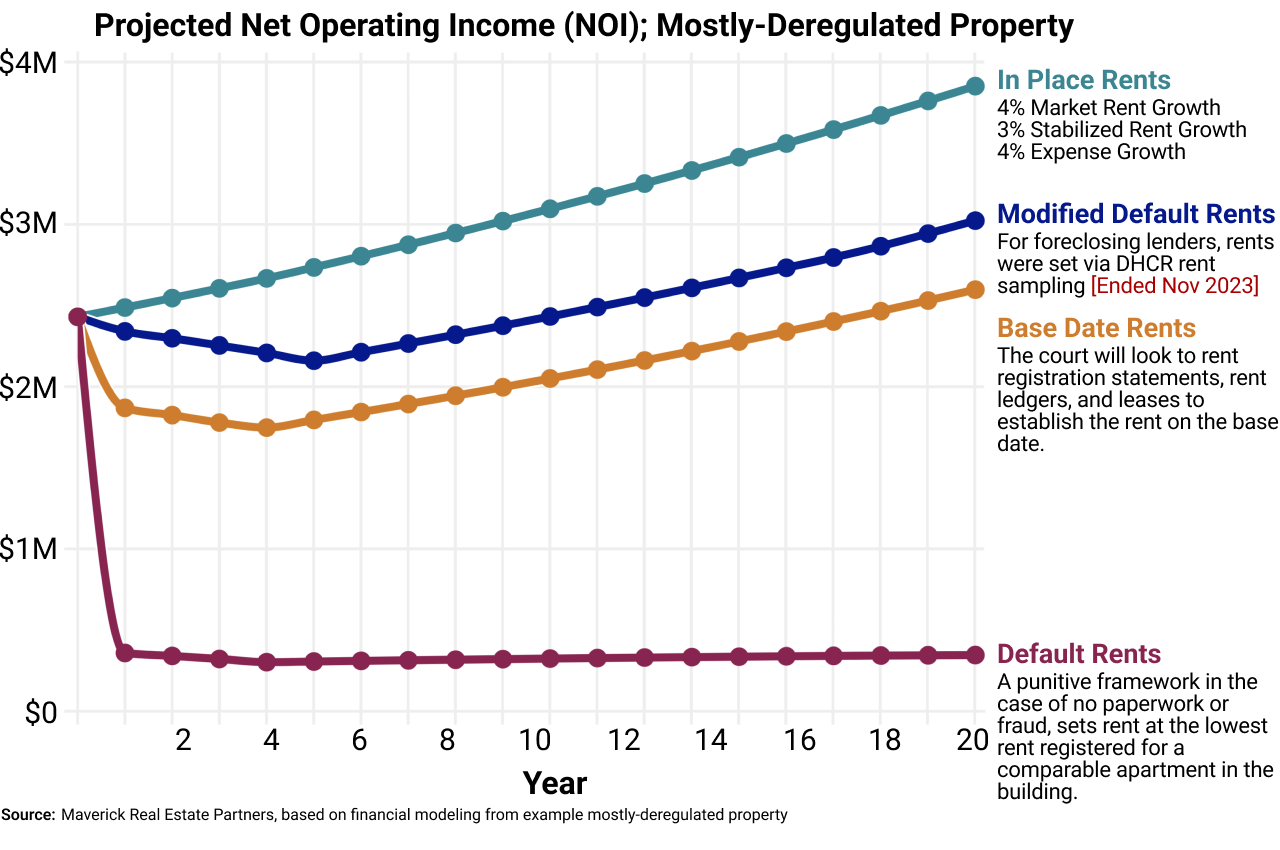

The Risks of Deregulation: The "Default Rent Formula" Minefield

For buildings with a mix of rent-stabilized and free market units, often the result of successful deregulation efforts prior to 2019, a different, more insidious risk has emerged. The HSTPA and subsequent court rulings have created a "default rent formula," a punitive framework that can be triggered if a landlord is unable to produce meticulous records justifying the deregulation of a unit. If a tenant successfully challenges the legal status of their apartment, and the landlord cannot provide the necessary documentation, the rent can be forcibly reset to the lowest rent of a comparable unit in the building. A coordinated challenge by tenants in a building could, in a realistic worst-case scenario, revert all deregulated units back to regulated status at drastically reduced rents, wiping out a building's NOI overnight. While most owners maintain sufficient rent records, lenders are often not in direct possession of this documentation, complicating potential foreclosure considerations.

This creates binary risk for both lenders and investors. Until November 2023, lenders had a unique layer of protection: the "modified default rent” formula. This less punitive standard, available to lenders who foreclosed on a property or subsequent buyers of those properties at foreclosure or bankruptcy sales, allowed for the rent to be reset to the average of the regulated rents in the neighborhood, rather than the lowest comparable rent in the building. This protection was subsequently deemed to be a loophole and closed by amendment to the Rent Stabilization Code. Lenders must now underwrite the Base Date Rent scenario - which requires possession of rental history documentation - otherwise face the risks of the aforementioned default rent formula. The chart below is based on an investment acquired by Maverick in 2022:

Finding Opportunity Amidst the Chaos

Navigating this complex landscape, fraught with both the risks of increased regulation and the challenges stemming from past deregulation, requires a level of diligence and expertise that goes far beyond traditional real estate analysis. For investors looking to acquire distressed debt in this space, a multi-pronged approach is essential:

- Pre-Acquisition Diligence: A Freedom of Information Act (FOIL) request to the Department of Housing and Community Renewal (DHCR) is a critical first step, providing a historical record of every regulated unit in a building. This data, combined with a thorough review of Department of Buildings (DOB) records, can help to justify historical rent increases and assess the risk of a deregulation challenge.

- Litigation and Receivership: The loss of a lender’s ability to utilize the modified default rent formula is a significant setback for a foreclosing lender, and therefore lenders must obtain records from their borrowers supporting the prior deregulation of units. Receivership orders can be modified to explicitly demand historical leases, books and records, rent rolls, and related documents, providing lenders with legal leverage to obtain necessary documentation.

- Strategic Asset Management: For those who end up taking title to a property, the key is to create a clear and defensible narrative for the next buyer. This involves organizing all historical documentation, obtaining opinion letters from counsel, and presenting a comprehensive package to the market that addresses all potential risks head-on.

The rent-stabilized multifamily market in New York City is not for the faint of heart. The challenges are immense, and the risks are complex. However, for those with the expertise to understand the nuances of the legal and political landscape, and the patience to navigate a distressed market, opportunities are likely to emerge. The coming years will likely see a wave of loan sales secured by rent-stabilized properties. The investors who are best prepared to analyze and underwrite these complex risks will be the ones who not only survive but thrive in the aftermath of this challenging market.