Geothermal power as a clean energy source is a buried secret — in both a literal and practical sense.

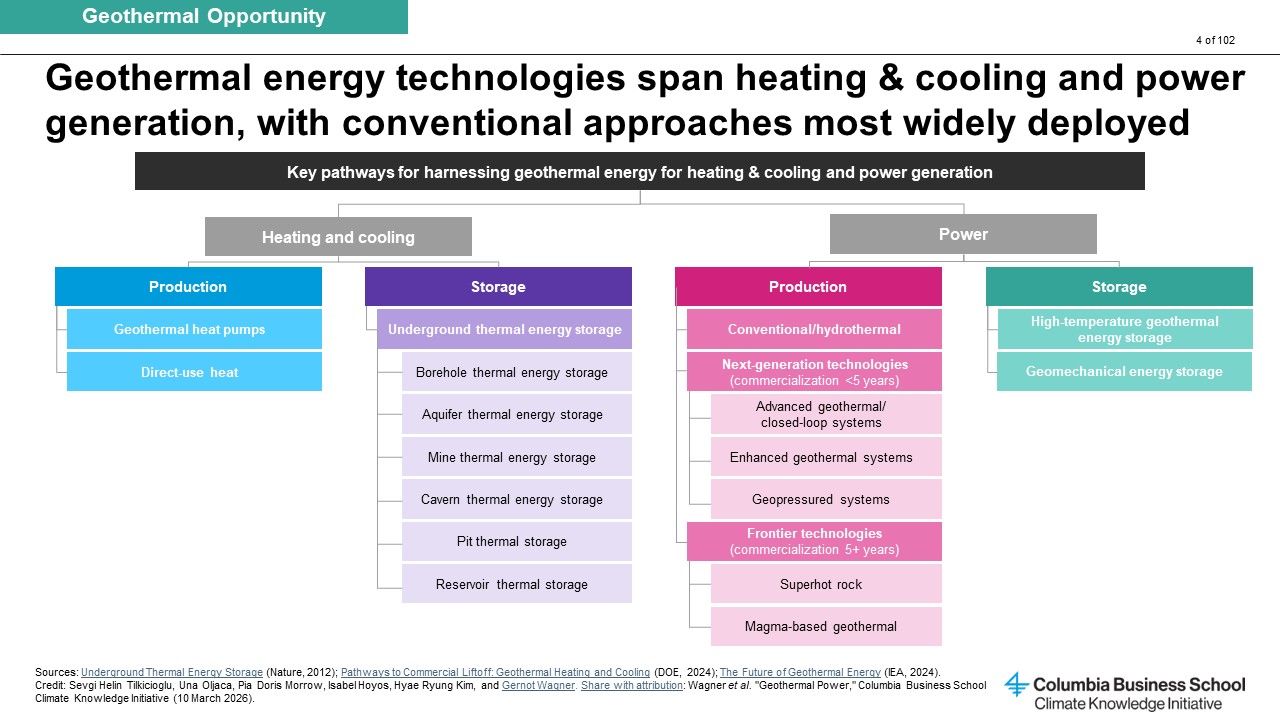

On one hand, this is literal: Geothermal energy is harvested by drilling deep into the earth to access heat that can produce steam, turn a turbine, and deliver electricity. Additionally, geothermal energy can provide heating and cooling, and even serve as a form of energy storage — like a large subterranean thermal battery. Approaches like underground thermal energy storage store heat or cold within the earth for later use, retrieving it when needed, typically to heat or cool buildings.

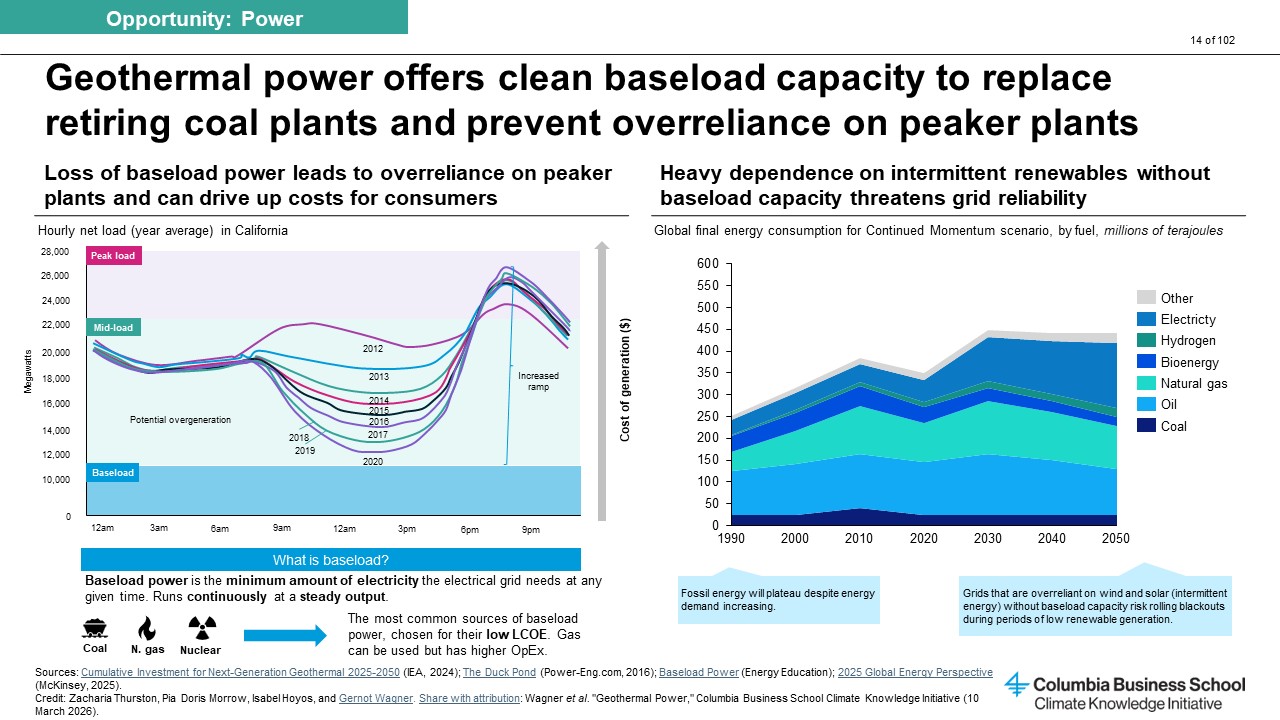

Even in its conventional form, where drills tap naturally occurring hydrothermal reservoirs beneath the earth’s surface, geothermal has long offered a distinctive advantage among renewables: 24/7 baseload power. Unlike wind or solar, geothermal does not ebb with weather or time of day. Instead, it provides a continuous, always-on source of clean electricity — precisely the kind of firm power that large industrial operations and increasingly energy-hungry data centers need.

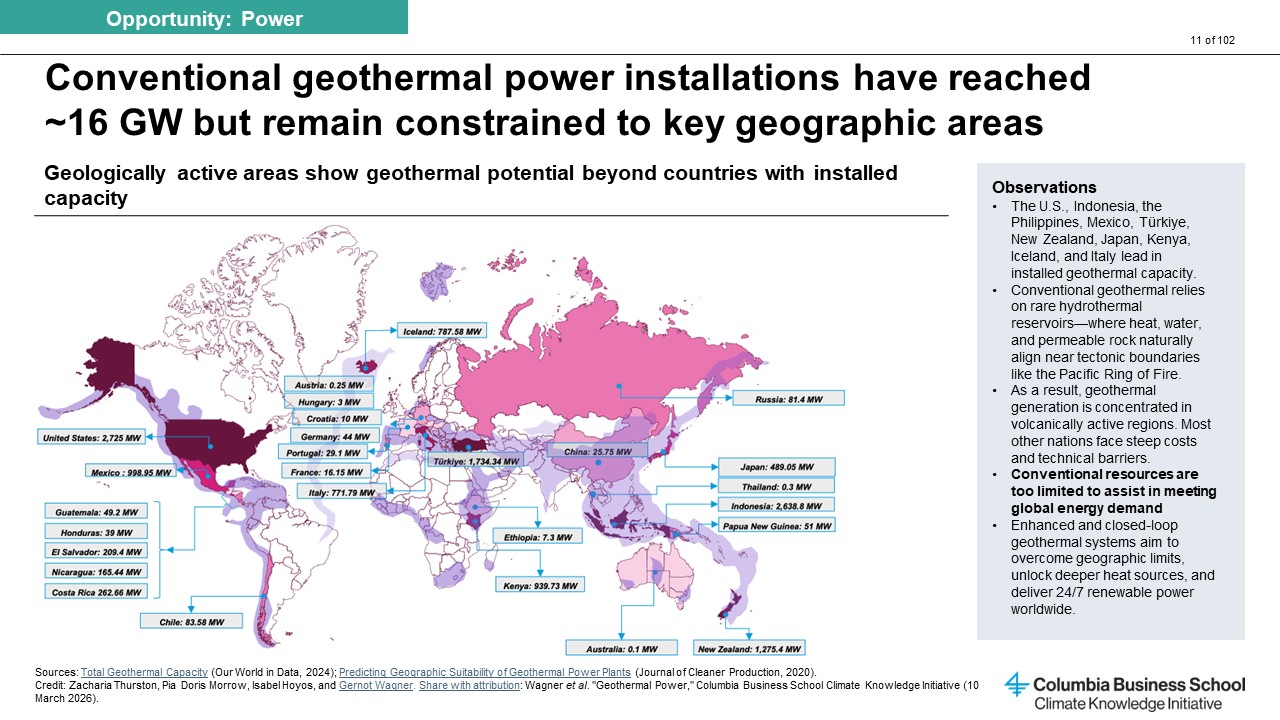

But conventional geothermal has never scaled beyond a niche; it currently satisfies less than 1 percent of global energy demand. For decades, its deployment has been constrained to select regions where geology cooperates, typically areas with natural hydrothermal systems near tectonic boundaries, like in the western U.S., Iceland, Indonesia, Türkiye, Kenya, and Italy.

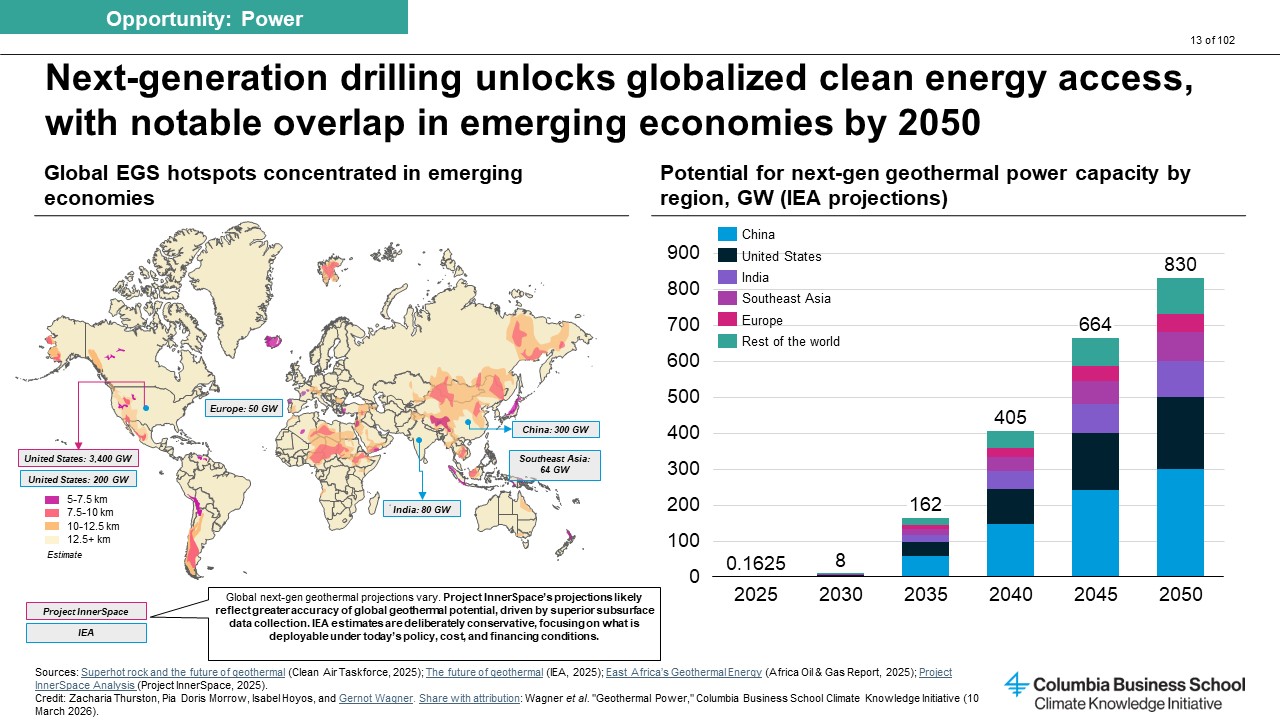

That reality is now shifting — quickly. From enhanced geothermal systems (EGS) to closed-loop systems to superhot rock geothermal, a wave of next-generation geothermal technologies aims to break geothermal free from its long-standing geographic constraints. If these technologies fulfill their promise, geothermal could deliver clean, firm, zero-carbon power nearly anywhere on the planet, massively expanding the role it can play in the global energy mix.

“The size of the prize for geothermal is bigger than for any other renewable but for solar PV — and those aren’t my words; those are IEA's words,” says Drew Nelson, vice president of programs, policy, and strategy at Project InnerSpace, referring to a report on the future of geothermal energy from the International Energy Agency.

“But people don’t know that,” Nelson adds. “Many people say, ‘We don't really have geothermal where I am, so it's not worth it for me.’ But almost everywhere on earth absolutely has geothermal industrial heat and direct-use heat potential, and in many places, there is geothermal power.”

Still, cost remains a significant barrier, and next-generation technologies are only just beginning to move down the cost curve. Several hurdles — technical, financial, and regulatory — continue to limit rapid adoption. Exploration risk remains high; drilling is expensive; deep, hot rock environments push the limits of existing tools; and heat flow variability creates uncertainty.

At the same time, possibilities across the geothermal landscape are shifting quickly: Drilling rates are accelerating, costs are falling, and new types of buyers — especially hyperscaler data centers — are creating unprecedented demand for firm, clean power.

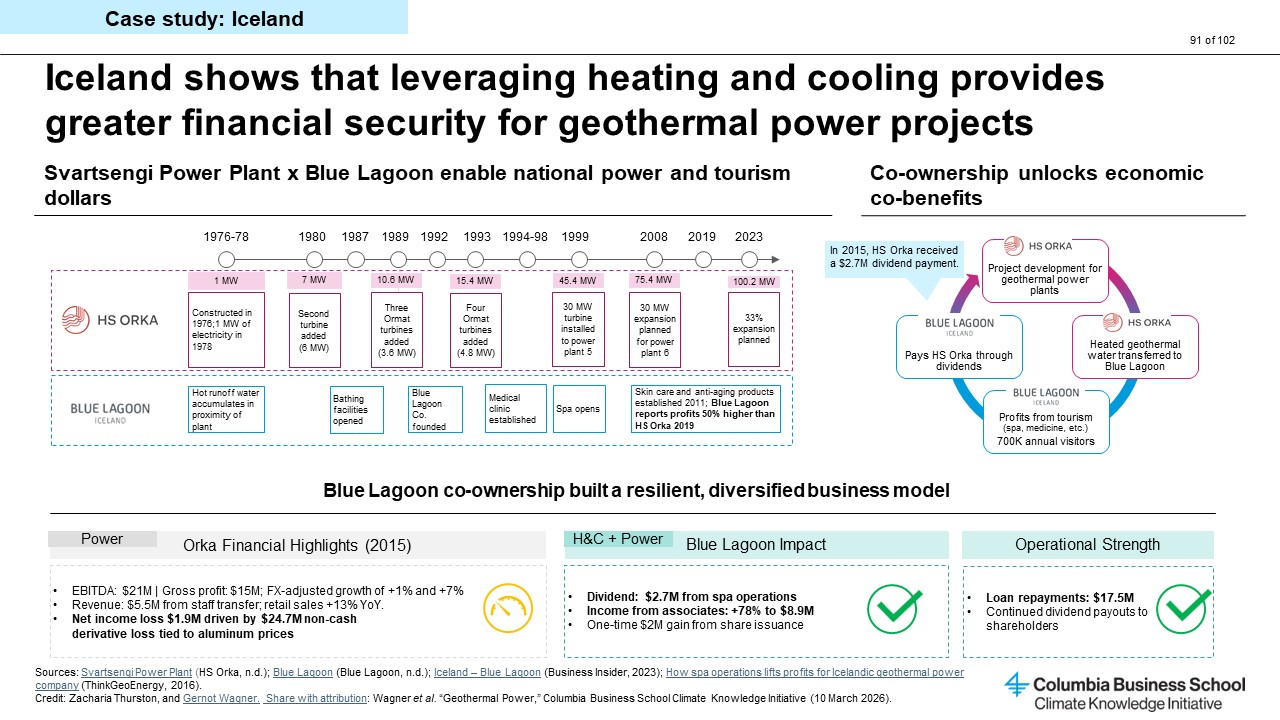

What’s more, geothermal’s benefits extend beyond electricity. As Lilja Magnusdottir, director of resource management at HS Orka, an Icelandic energy company, emphasizes, geothermal is also an extraordinarily valuable source of heat. In her country, 90 percent of houses and companies are connected to geothermal heating systems.

“Geothermal has greater multiuse potential than solar, wind, hydro,” Magnusdottir says. “Unlike those resources, geothermal energy provides heat that can be cascaded through multiple economic sectors.”

Iceland’s Blue Lagoon is one of the most famous examples of how geothermal heating benefits can exist happily alongside geothermal power projects. The series of pools that make up the Blue Lagoon outdoor spa are warmed by the “waste” (that is, heated water called brine) of one of HS Orka’s plants, and the cascaded streams have become an important source of revenue for the energy company. A similar dual-benefit can be harnessed by colocating geothermal power plants with data centers, which require both power and cooling.

The sector now stands at a pivotal moment. With vast untapped resources, rapidly improving technologies, and a global race to expand power to fuel AI data centers, geothermal is primed for a breakout decade, going from buried secret to breakout renewables star. There are still hurdles aplenty, making it necessary to find creative ways to navigate the intertwined challenges of technological innovation, financing gaps, subsurface-data availability, and policy environments.

Below are five key points that emerged from a discussion among the geothermal industry leaders who participated in a recent workshop convened by Columbia Business School’s Climate Knowledge Initiative.

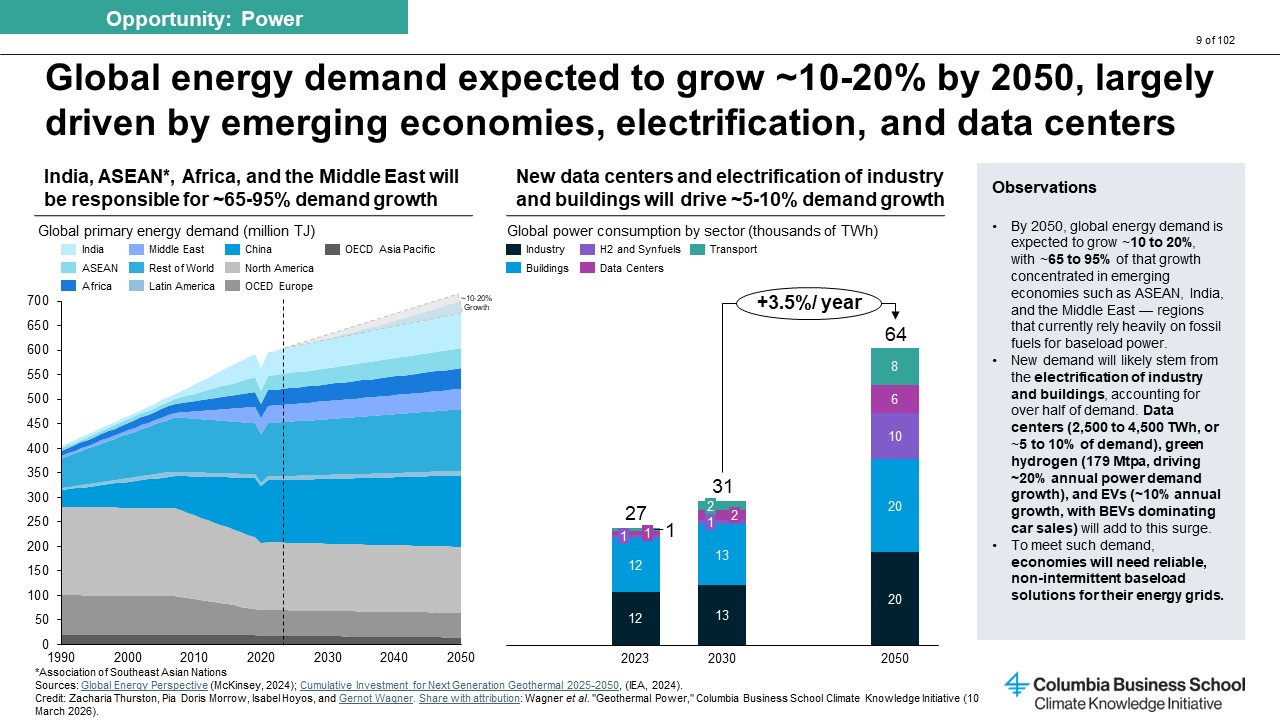

Key Point #1: Data centers are demanding a wholesale change in the energy mix — and geothermal is about to hit its big moment.

Few forces are reshaping the power landscape as drastically, or as quickly, as artificial intelligence. Total electricity demand is still relatively low, but it is growing rapidly. Since late 2022, with the public release of ChatGPT, demand for data center power has surged dramatically, driven by AI model training, inference, and deployment. Data centers consumed about 400 TWh in 2024, 1.5 percent of global electricity demand and are expected to use 1,000 TWh, or ~3 percent, by 2030.

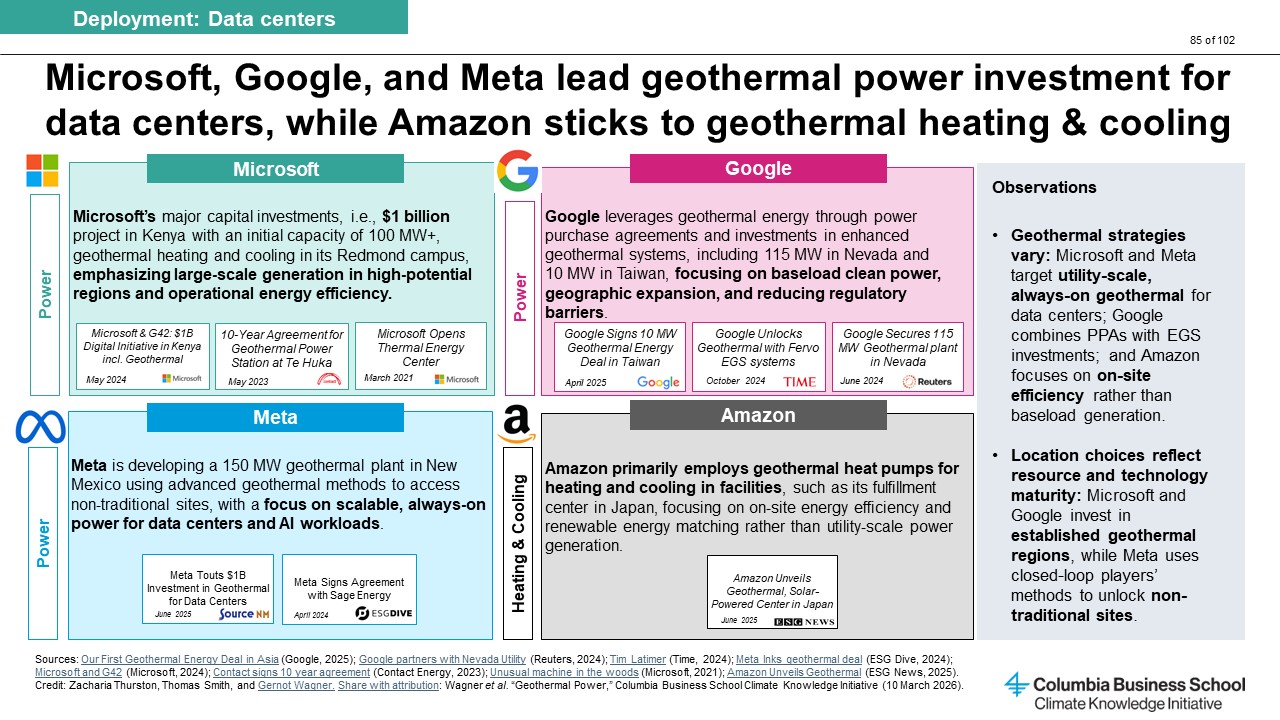

Today’s data centers are not just hungry for electricity — they are hungry for firm, clean, round-the-clock electricity. Hyperscalers like Google, Microsoft, Meta, and Amazon are under pressure from shareholders, regulators, and customers to procure zero-carbon power. But intermittent renewables, even backed by large volumes of battery storage, cannot solve the firm power gap at the scale required.

Against this backdrop, geothermal is emerging as a leading contender to meet data centers’ unique requirements, with some hyperscalers already inking deals to meet their power demands with the help of geothermal.

Geothermal is likely to continue to be a popular pick among energy-hungry hyperscalers, even as next-gen geothermal remains more expensive than solar or wind. That’s because the power source comes with “co-benefits” not necessarily reflected in the price.

“If you are looking at the full benefits of geothermal —the national security benefits, the firm benefit, the clean benefit, the fact that you have a workforce from oil and gas that's easy to transition — all those make geothermal look better,” said Nelson from InnerSpace. “All those are co-benefits. But none of that is reflected in what tech companies need to pay to get the electrons on the grid.”

Similarly, in many political debates about which renewable power sources deserve more support as AI expands, geothermal is gaining prominence. U.S. Secretary of Energy Chris Wright has expressed strong support for geothermal, noting that among its many selling points are its overlaps with oil and gas drilling technology.

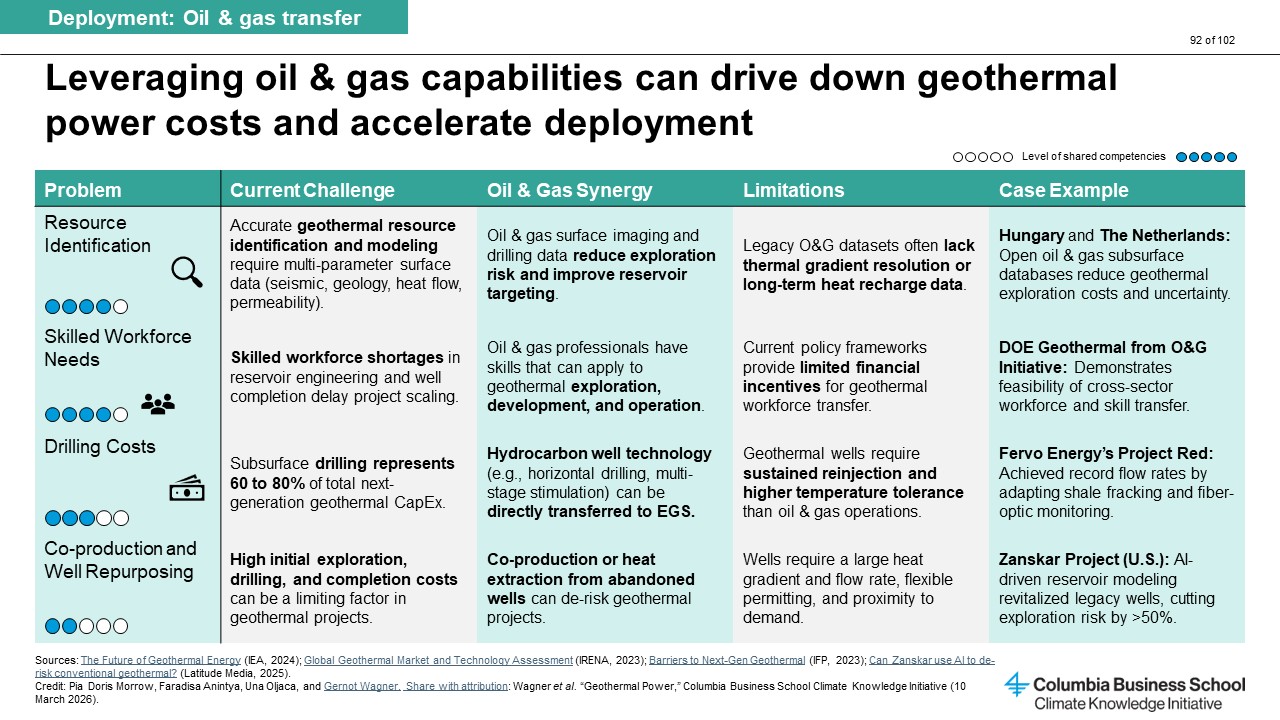

Key Point #2: Geothermal and the oil and gas industry have deep synergies.

Wright isn’t the only observer of geothermal who believes that the industry’s overlaps with the oil and gas space redound to a massive advantage for geothermal.

“There's a lot of brain power in oil and gas; there's a lot of brain power in utilities,” said Nelson. “Much of that knowledge can be easily transferred to geothermal.”

The synergies run deep. For one thing, drilling expertise is directly transferable from oil and gas to geothermal, which gives the industry — especially its most cutting-edge technologies — a leg up. Drilling accounts for 60 to 80 percent of next-gen geothermal project costs. U.S. companies, thanks to decades of shale development, are world leaders in drilling speed, accuracy, and cost efficiency.

What’s more, subsurface data and modeling from oil and gas can dramatically reduce risk. This means that emerging geothermal players do not start from a blank slate; they inherit decades of geological insight, seismic data, and reservoir modeling techniques.

“No one drills better than we do in the United States,” said Nour Ghadanfar, chief of staff at Fervo Energy, a next-gen geothermal company focused on EGS. “It’s American ingenuity.”

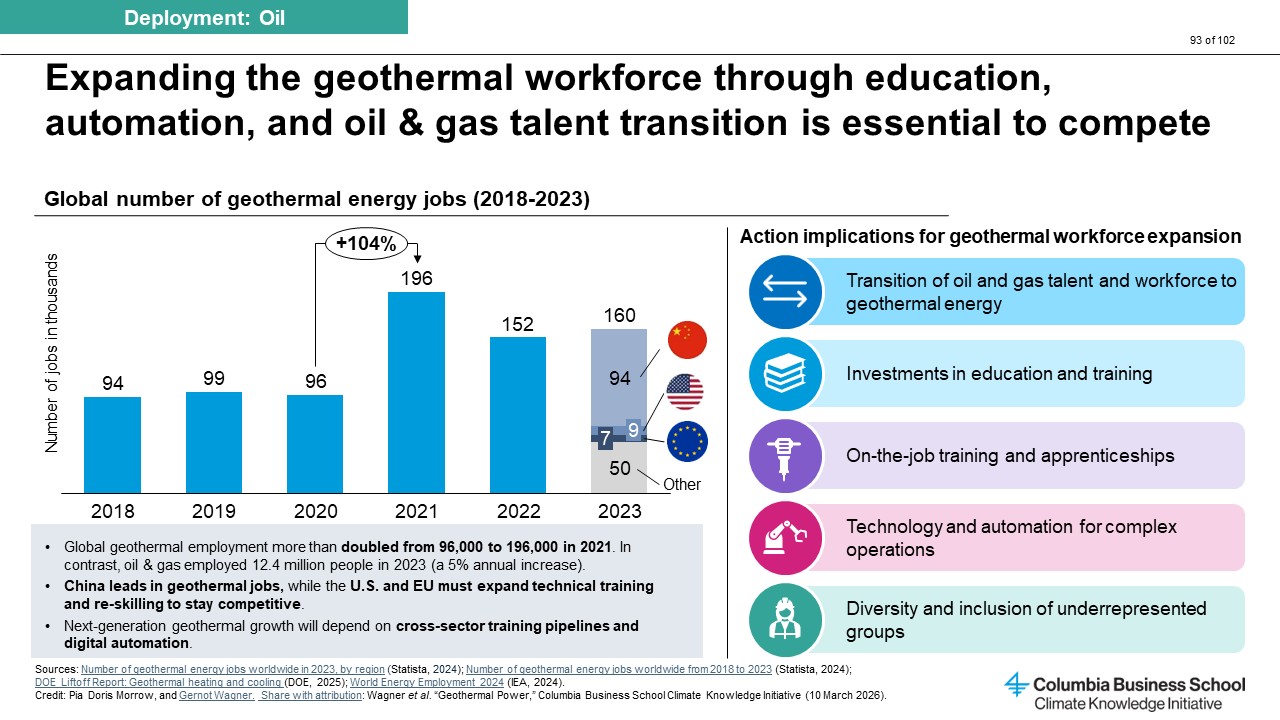

That ingenuity largely rests in the hands and minds of workers across the oil and gas industry, and geothermal is primed to make full use of it. The core expertise fueling geothermal innovation is almost identical to that of oil and gas, which makes geothermal a compelling pathway for a “just transition” for oil and gas workers as the world reduces its reliance on fossil fuels.

For all of these reasons, investing in geothermal is a bankable idea for the United States, arguably much more so than investing in nuclear or other renewables, according to Milo McBride, a fellow at the Carnegie Endowment for International Peace. “Why do we have solar research when we're never going to be a competitive solar manufacturer?” McBride said. “In brutal realist terms, it doesn't make sense. Geothermal is a place to compete, so let's double down on that.”

One idea that has captured some policymakers’ imagination — repurposing existing oil wells as sites for harnessing geothermal power — was dismissed by experts at the workshop as an impractical distraction. They agreed that while such repurposing is a good idea in theory, in practice, cost and capacity constraints are too steep.

Still, oil and gas companies are well positioned to play a close supporting role in expanding geothermal, even if not directly via transitioned oil wells. But will they? The answer is nuanced.

On one hand, legacy oil and gas companies are increasingly exploring geothermal — looking to invest, build, or buy. Jonathan Sisto, managing director of investment banking, the energy transition, and AI energy solutions at RBC Capital Markets, noted that as shale matures, oil and gas boards have been on the lookout for additional geographies or subsectors that offer growth opportunities for their companies.

“Oil and gas companies are looking for the next growth avenue, where there are technology adjacencies for their well-skilled and trained staff — and next-generation geothermal is very much in the bull’s-eye,” Sisto said.

On the other hand, most oil and gas companies are large public companies, and the current geothermal industry is too small to make a meaningful dent in their income statements in the near term, thus limiting their appetite for acquisitions.

Still, that’s not a good reason for oil and gas majors to ignore such a plum opportunity, argued Roland Horne, the Thomas Davies Barrow Professor of Earth Sciences at Stanford University. “Oil companies know the subsurface all across West Texas and the Gulf Coast and many other places as well,” Horne said. “They've got the people, they've got the technology, they've got the capital, they've got the data, they've got the land positions. What's holding them back?”

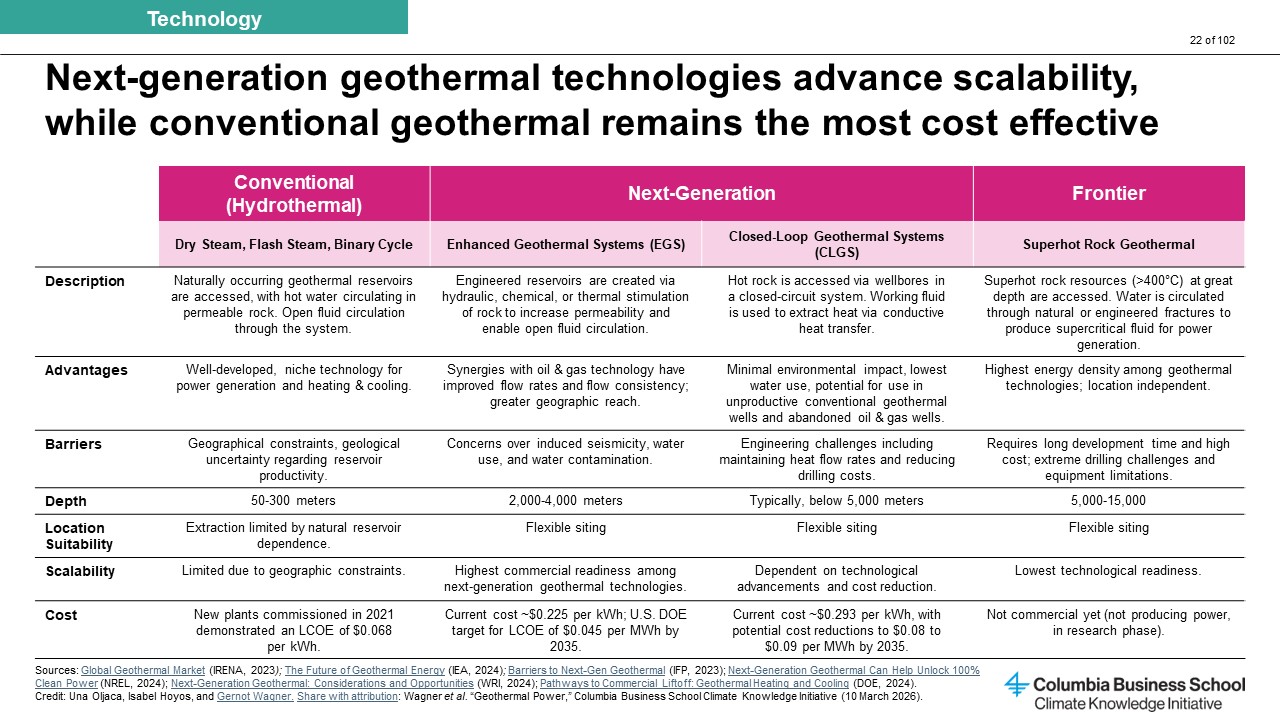

Key Point #3: The world’s energy demands call for a diverse mix of many geothermal technologies and approaches — not a winner-take-all race.

A misconception about next-gen geothermal is that a single dominant technology — most often EGS — will unlock the sector’s full potential.

Experts at the workshop emphasized the opposite.

“The technology needs to follow the problem archetype,” said Nestor Sepulveda, Advanced Energy Investments and Partnerships at Google. In other words, the best geothermal technology for a specific case depends entirely on the geology, energy use case, and minimum scale, along with a host of other factors.

For many years, the only geothermal approach available was conventional: reliance on rare hydrothermal reservoirs where heat, water, and permeable rock naturally align near tectonic boundaries, like the Pacific Ring of Fire. While these resources are plentiful in some parts of the world, conventional geothermal alone cannot meet global demand. The best hydrothermal resources are already tapped; the remaining potential is limited in scale and geography.

Next-gen technologies, by contrast, break this constraint. They can:

- Unlock geothermal power in regions with no natural reservoirs;

- Go deeper and hotter to deliver more power;

- Enable behind-the-meter systems for data centers (meaning they serve data centers directly, rather than a utility); and

- Reduce reliance on exploration luck.

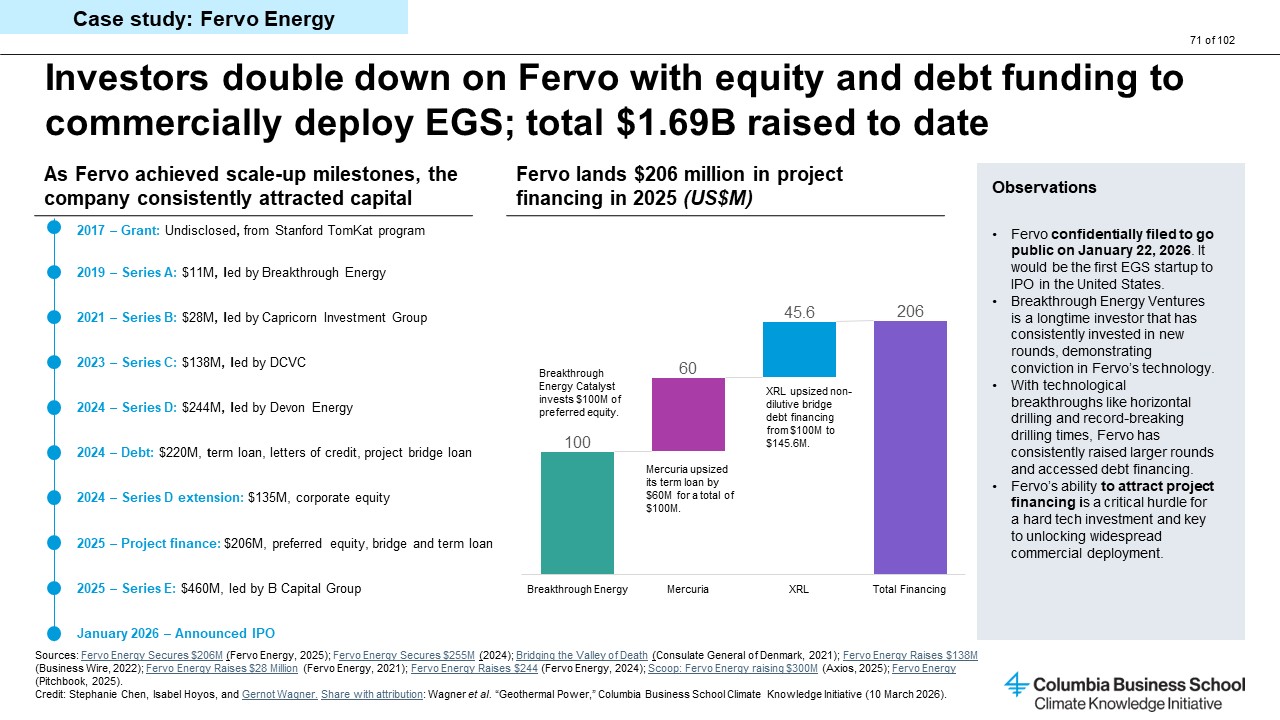

Fervo Energy’s approach is a leading example of next-gen geothermal and the potential it implies. Fervo harnesses heat through EGS and leverages horizontal drilling and advanced data analytics to speed demand and increase efficiency.

Ghadanfar shared numbers to illustrate just how rapidly the company is shrinking drill speeds: Its first two wells — both 8,000 feet deep and 3,500 feet long — were drilled in 70 and 59 days while its most recent well — 11,200 feet deep — was drilled in just 11 days and reached 555°F.

Historically, that kind of learning curve is characteristic of shale, not geothermal, and it indicates something essential: Next-gen geothermal is still early in its learning journey, meaning dramatic cost declines are plausible.

Moreover, modularization — particularly of surface power plants — may further accelerate deployment speed and reduce costs. “For us, having a modular power plant means we can sign long-term service agreements with parts suppliers, which means we can get parts faster,” Ghadanfar said.

“In the end,” she added, “we won’t be a project company but rather a product company, where our product is geothermal power plants.”

Fervo’s EGS approach isn’t the only next-gen geothermal technology receiving funding and gaining momentum. Closed-loop systems, geopressured geothermal, and even superhot technologies all expand the boundaries of heat resource potential and address different limitations of conventional systems.

Several experts voiced concern that the geothermal sector is wasting time debating which of these technologies will win.

“It's broadly recognized that multiple technology approaches are going to be needed to unlock the full potential of hot rock resources, particularly when overlaid with water and geology considerations,” said Lucy Darago, chief commercial officer at XGS Energy, a next-gen geothermal company using heat-harvesting technology and a closed-loop well architecture.

Key Point #4: Geothermal’s growth depends on data sharing and open knowledge — something the private sector cannot solve alone.

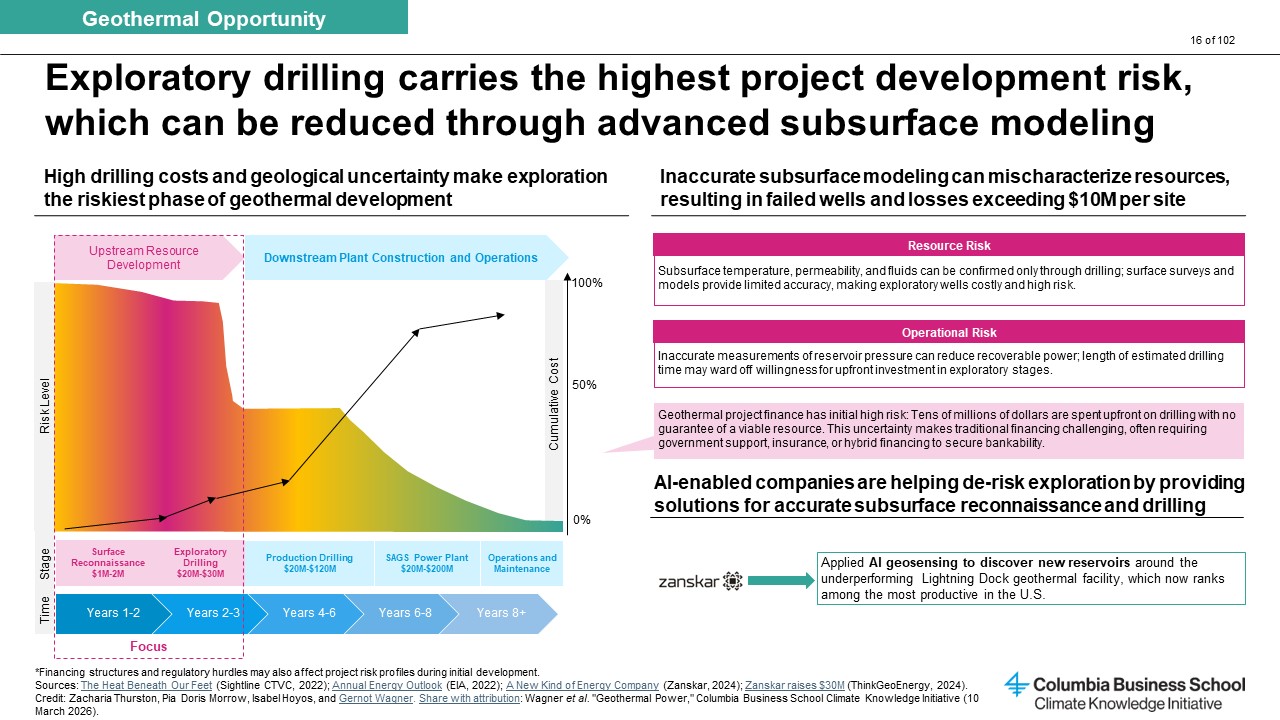

Exploration risk remains one of the biggest barriers to investment. Developers face high upfront costs to confirm whether a site has the right temperature, rock type, and permeability. And unlike shale, geothermal has no established, standardized public geological database.

Some experts at the workshop argued that geothermal will need its own public database of subsurface information and acknowledged that this will be an effort best organized by governments, not private actors.

There are lessons to be gleaned from the European Union’s willingness to do just this: As Martina Lyons, Energy Analyst at IEA, explained, Europe’s interest in geothermal grew after Russia’s invasion of Ukraine disrupted gas supplies. Geothermal heat, particularly for buildings, gained greater attention as a way to strengthen national security.

That shift catalyzed new efforts to standardize data and make it public.

“Countries started thinking about how to pull together data and make them available publicly, standardize them so they are comparable,” Lyons said. “We’re not there, but there is an effort — and it is being supported by public funding.”

Stanford’s Horne emphasized that such government-led data sharing can be catalytic. Utah FORGE, a federal research site, provided extensive open data on geology, heat flow, and rock quality. Fervo sited its Project Cape nearby in part because FORGE’s data dramatically reduced uncertainty.

“A lot was revealed by Utah FORGE,” said Horne. “The data was all available. That opened the door for Fervo; they could have done it themselves, but it would’ve cost another $50 million.”

For its part, Fervo is publishing its own drilling and reservoir data to accelerate industry learning. “From Fervo's perspective, we try to publish a lot of our drilling data,” said Ghadanfar. “I think as we're trying to build this next-generation industry, there are a lot of learnings from conventional and vice versa. And it's important for a lot of developers to share in that open transparency.”

Project InnerSpace is developing GeoMap, a geospatial platform aggregating global geothermal data. But such efforts need public support. As Lisa Epifani, head of policy at ClearPath, said, even basic questions, like where transmission lines align with geothermal potential, lack available data.

One form knowledge sharing could take is cross-border experimentation, suggested Marta Karlsdóttir of Baseload Power Iceland — for instance, taking advantage of Iceland’s accessible resources and geothermal experience as a fertile place for experimentation.

“I think Iceland is probably one of the best places to innovate in technology, with our mature geothermal market, experienced workforce, proven infrastructure, favorable geological conditions, and strong support from authorities and local communities,” she said. “Companies like Fervo and XGS could find exceptional value in partnerships with Icelandic developers to pilot emerging technologies that would benefit the entire industry.”

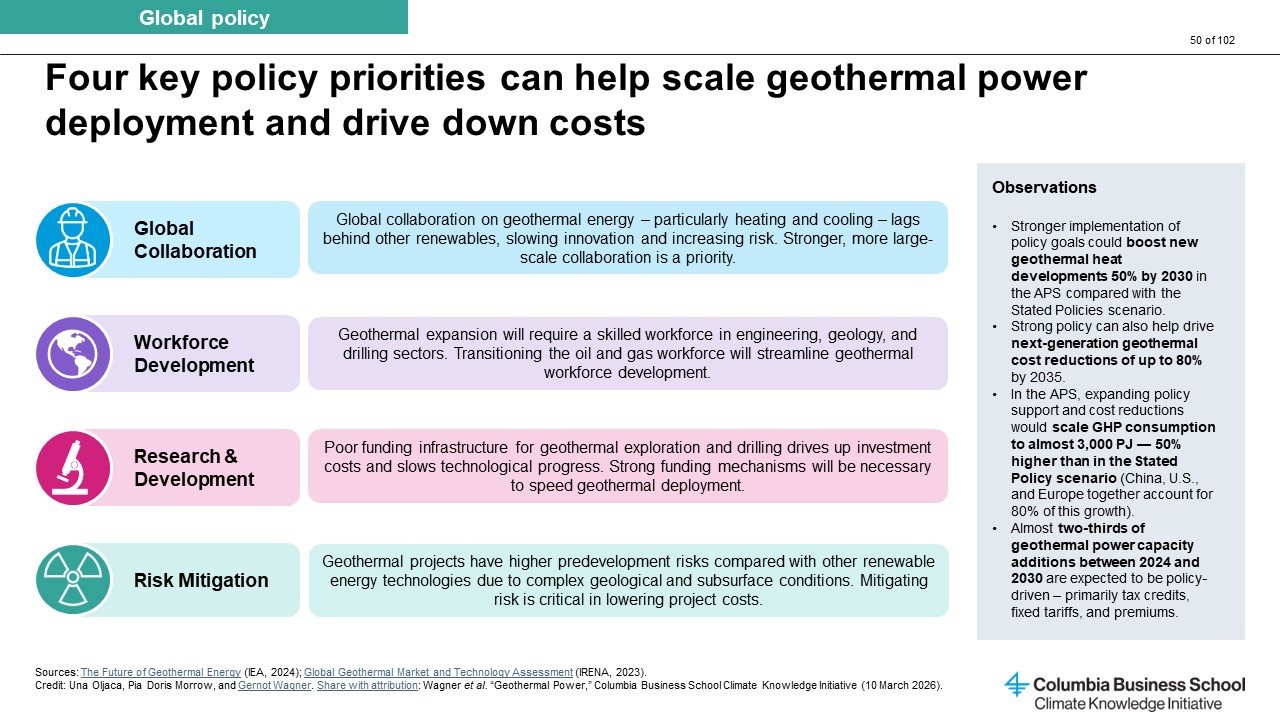

Key Point #5: Geothermal’s biggest financing challenge is early-stage de-risking.

The issue is not the total availability of capital — energy markets are flush with it. The issue is risk appetite.

Next-gen geothermal projects sit in a difficult stage: too capital-intensive and risky for venture capital and too early and uncertain for major banks or infrastructure investors.

While many national governments can finance early geothermal exploration (and have historically done so), today’s policy frameworks often don’t cover the drilling risk that most deters private capital.

World Bank’s ESMAP program and similar tools show that government-led exploration, cost-shared drilling, and fiscal incentives can unlock private investment. According to sector analyses, these tools — combined with oil and gas expertise — could reduce next-gen geothermal costs by up to 80 percent, making them competitive with nuclear and solar PV (plus storage).

Charles Gertler, CEO and co-founder of New Mantle Technologies, pointed out that the role public funding has played in past expansions of the geothermal industry cannot be underestimated — and underscores the need for continued government support of the sector.

“Instrumental to everything we're talking about today was a couple hundred million dollars of federal funding,” Gertler said, pointing to Utah FORGE as a prime example. “The U.S. built a ton of geothermal in the middle of the century, largely on the back of public financing and funding, as in other countries."

Fervo’s Ghadanfar noted that hyperscalers have played an unexpected role in derisking geothermal — for example, Google’s early involvement in Project Red. She said the partnership both proved Fervo’s technology works at commercial scale and demonstrated that there is a buyer for the electrons.

“If Google had not worked with us on Project Red,” Ghadanfar said, “Fervo would not be where we are today.”

Joint ventures with other big players could be another solution for allowing next-gen geothermal companies to achieve takeoff. Many experts agreed that a partnership model, perhaps pairing geothermal innovators with oil and gas majors, could spread risk and accelerate development.

Darago of XGS said a solution may be collaborations with power and infrastructure companies, which are accustomed to power project returns structures and more predictable risk profiles. Leading U.S. power producer Constellation Energy is an investor in XGS.

“We often talk as if geothermal only scales if oil and gas, namely integrated energy companies, move in and use balance sheet capital to develop these assets, similar to how oil and gas resources are developed,” she said. “But in the foreseeable future, it's not obvious that a financing approach will make sense for geothermal power.”

“Who it does make sense for is power and infrastructure companies,” Darago added, pointing out that they are used to low-risk, predictable projects, with lower but longer lived returns. In follow-up comments, she added, "The key challenge infrastructure capital has is production risk. If geothermal players can prove they can deliver multidecade predictable performance, or, in other words, address the industry's historical challenge of volatile production, there's an opportunity to access an enormous infrastructure capital pool that is hungry for these assets."

Funding support can come from other unexpected sources as well, InnerSpace’s Nelson said, touting a new $100 million fund created for the sole purpose of derisking next-gen geothermal.

Government support, too, remains essential in this mix.

From ARPA-E to the Department of Energy’s shifting priorities to new federal de-risking funds, policymakers will play a decisive role in geothermal’s trajectory.

Today’s global geothermal industry exists in large part because national governments, alongside oil companies, funded most of its earliest projects, Horne noted: “Capital in large amounts — capital that understands risk, which governments and oil companies both understand — is how we got the current industry.”

The question now is whether the world’s governments, financiers, and energy developers can (or will) move fast enough to match the opportunity presented by the rapidly changing geothermal landscape.

If they do, geothermal may finally emerge from underground and into the center of the clean energy transition.

We thank Pia Doris Morrow, Zacharia Thurston, Heather Hartel, Sevgi Helin Tilkicioglu, Stephanie Chen, Una Oljaca, Shubhangi Prasad, Thomas Smith, Faradisa Anintya, Leo Gordon, Hassan Riaz, Hyae Ryung Kim, Ariela Farchi Behar, and Isabel Hoyos for research and analysis supporting this article.