Artificial intelligence is reshaping the global economy and the energy system that powers it. Hardly a week goes by without a hyperscaler announcing a new energy deal to revive an old nuclear power plant or build new geothermal capacity, or signing a power purchase agreement (PPA) to support the demand expected by yet another data center.

The very term hyperscaler suggests that something new is afoot for electricity suppliers: Companies like Amazon, Google, Meta, and Microsoft and the many dedicated data center operators prize flexibility as much as cheap, firm power supplies. The big question is how much they also prize clean power—and which price they are willing to pay.

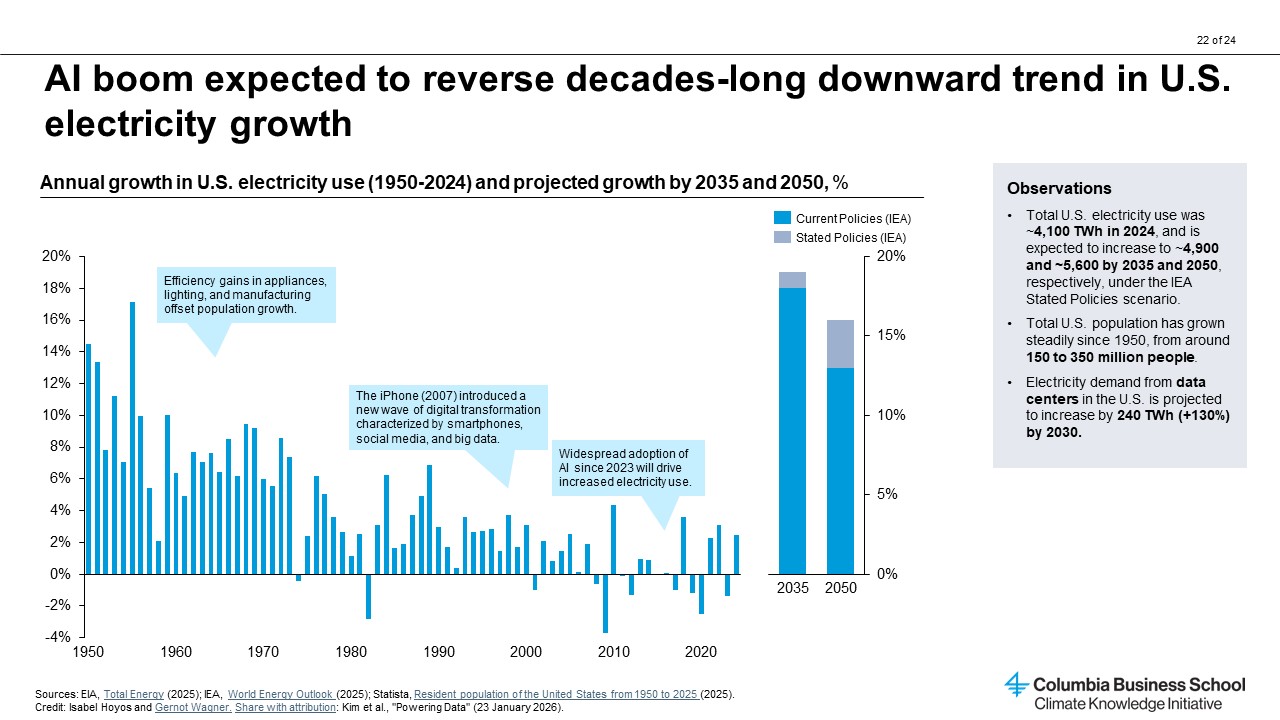

Since the late 20th century, electricity demand in advanced economies has remained relatively stagnant, especially in the United States and Europe. Efficiency gains in appliances, lighting, and manufacturing have offset population growth, leaving overall demand almost unchanged for decades. The digital boom of the early aughts and subsequent decade brought modest upticks from server farms and data centers but nothing that fundamentally altered the trajectory.

Learn more about Columbia Business School’s Climate Knowledge Initiative: AI Data Centers

With massive computational intensity and a steep adoption curve, AI is a different story. In its 2025 World Energy Outlook report, the International Energy Agency’s (IEA) forecast for global electricity generation by 2035 under the “stated policies” scenario increased ~9 percent from its 2023 forecast, up from 40,494 terawatt-hours to 44,274 TWh, largely driven by AI data center requirements.

Projections and estimations vary given data uncertainty, inconsistent reporting, and differences in assumptions. But according to IEA, data centers accounted for roughly 400 TWh, or about 1.5 percent, of global electricity use by 2024 and will reach 1,000 TWh (~3 percent) by 2030. This 15 percent annual growth rate is more than four times greater than in any other sector.

In fact, energy constraints are a limiting factor in the expansion of AI, at least in the United States, with tech companies building data centers faster than they can be connected to the grid or new power sources. This puts the race to build new power generation at the intersection of global economic dominance, energy security, and climate change.

Today, U.S. and Chinese data centers—which together consume about 70% of global data center energy—run primarily on natural gas and coal, reflecting the local power grids. But as renewables continue to exceed growth expectations and data center operators accelerate investment in both renewable deployment and next-generation clean technology development, data center electricity is projected to become less carbon-intensive, with emissions plateauing around 2030, according to IEA.

In the best-case scenario, the AI boom will act as a catalyst for the clean energy transition, with market-dominating tech giants using their massive capital muscle to accelerate clean energy buildout. Tailwinds are cause for optimism: Solar is now the cheapest electricity source globally and nuclear and geothermal energy are experiencing a resurgence after decades of stagnation. Meanwhile, coal plants continue their phase-out and natural gas turbines face long development timelines, making them increasingly unattractive for meeting urgent power needs.

But significant headwinds loom as well, particularly in the United States, where the AI race meets an administration set on hampering renewables and eager to seize the opportunity to throw fossil fuels a lifeline. The risk is that instead of accelerating decarbonization, AI's energy appetite will trigger a resurgence of America's declining fossil fuel industry.

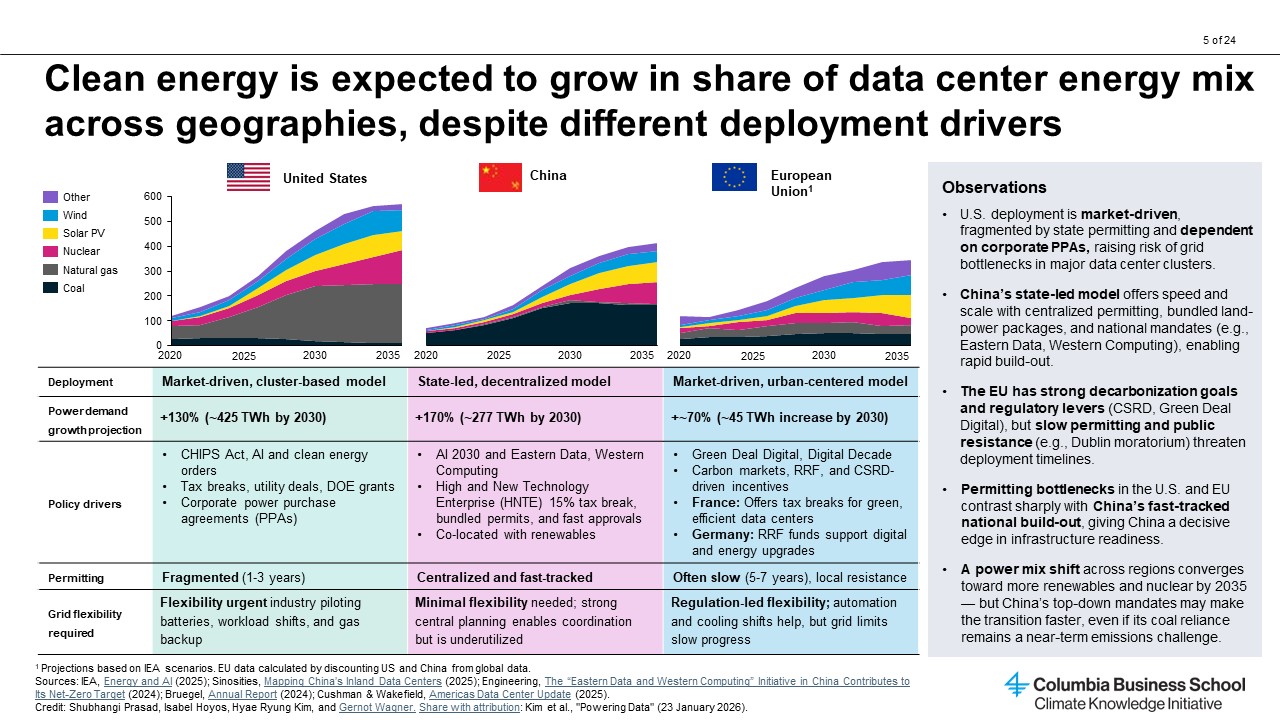

The United States, China, and—to a lesser extent—Europe lead global data center buildout

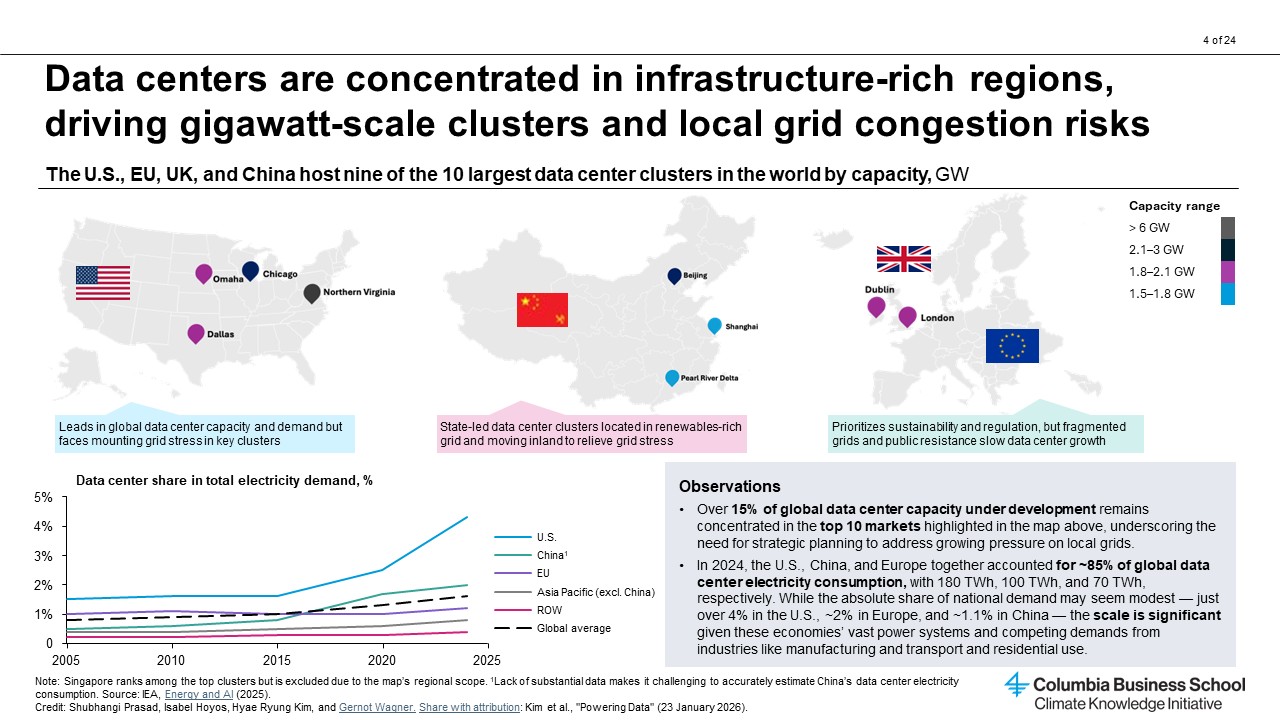

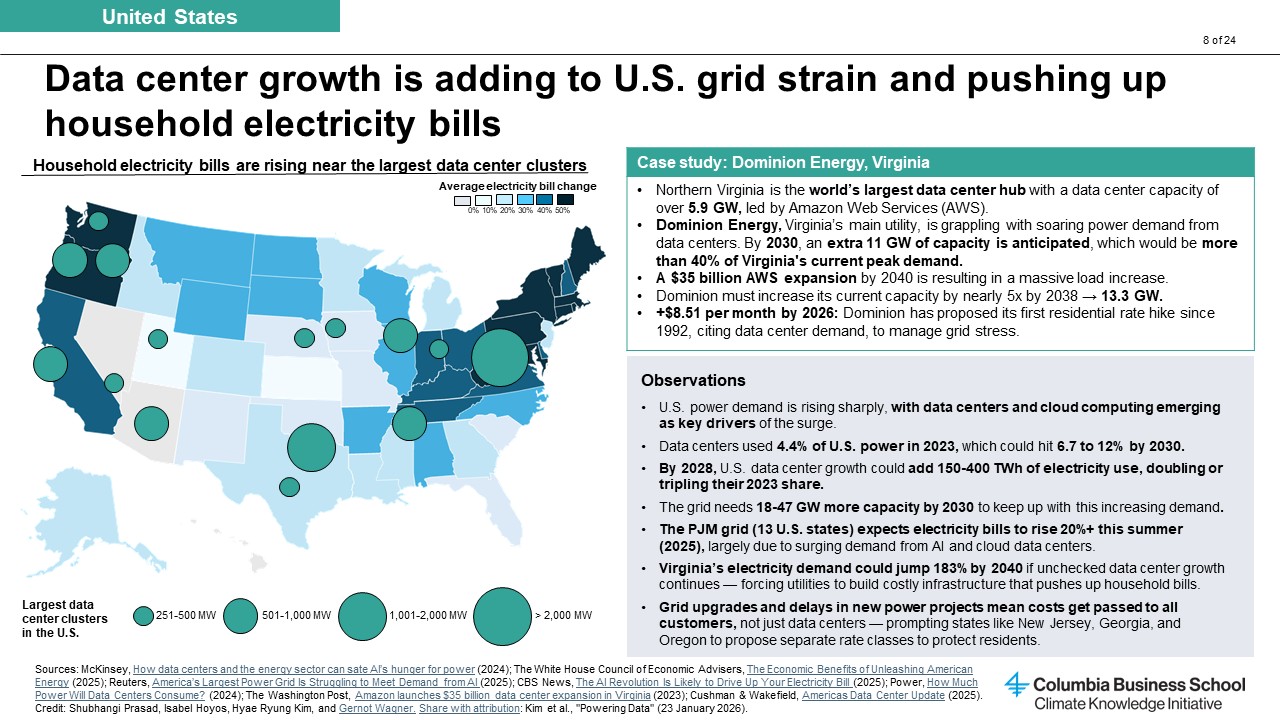

The United States is home to the world’s largest hyperscale data center market, with the biggest cluster located in Northern Virginia’s so-called Data Center Alley. But rapid growth is straining energy infrastructure, with electricity demand from power-hungry centers outpacing supply and households in these regions facing both rising energy bills and the risk of grid failures. One way developers are responding is by adopting “power-first” siting strategies, selecting sites based on power availability.

China instead is tackling the challenge with a centrally coordinated approach. The government’s East Data, West Compute initiative relocates clusters away from crowded coastal cities and to renewable-rich inland regions, where land and energy are more abundant. Bundled infrastructure packages, fast permitting, and coordinated transmission planning enable rapid buildout, but the near-term reliance on coal to power some of these facilities remains a challenge to China’s decarbonization goals.

Europe’s data center growth is relatively slower and more sustainability centered, with permitting delays that can stretch from five to seven years. The region has seen significant public pushback over AI energy and land intensity, to which the European Union has responded with policy frameworks like Green Deal Digital and the Digital Decade, designed to balance digital expansion with climate goals.

Some countries are offering their own incentives for efficiency and clean power use. France, for example, provides tax breaks for data centers that meet stringent energy and water efficiency standards.

Intelligent grids and operators can drive energy efficiency

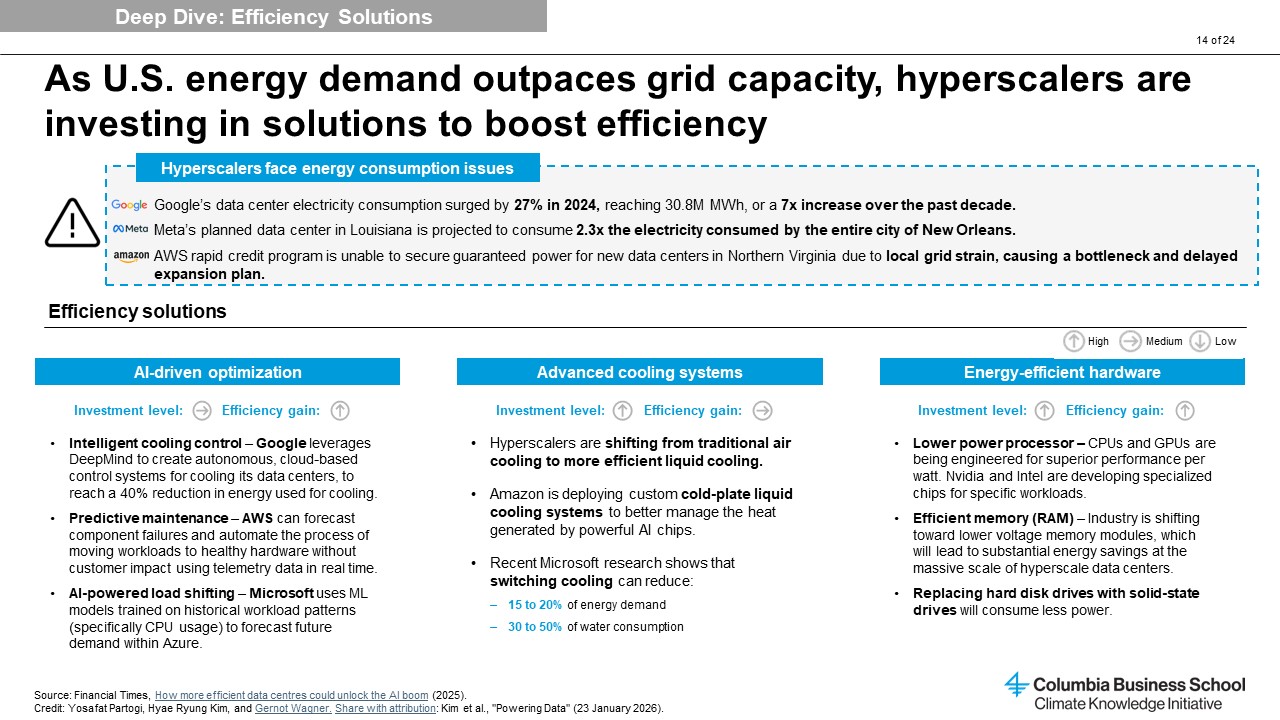

Efficiency, though not a true decarbonization solution, is a lever data centers can use to partially decouple growth in computing power from energy demand and, thus, emissions. Hyperscalers are constantly improving hardware, software, and cooling systems to extract more performance per watt, with the industry benchmark, Power Usage Effectiveness (PUE), improving steadily. Cooling innovations, able to reduce energy use by up to 40 percent, are proving particularly effective.

Google, as an example, is partnering with utilities to integrate demand flexibility into its data center fleet, reducing strain on local grids during peak hours. The collaboration allows machine learning and non-urgent compute tasks to be shifted to times when electricity is more readily available. Together with its investment in clean energy procurement, these efforts resulted in a decrease in emissions of ~12 percent in 2024, despite a ~28 percent increase in energy demand.

AI itself is also being used to optimize the energy value chain by forecasting solar and wind energy based on hyperlocal weather data, analyzing energy markets to predict the most efficient charge and discharge rates for batteries, and predicting price and load downstream. Inside data centers, AI could optimize everything from demand response to temperature control.

Data centers as clean energy market makers

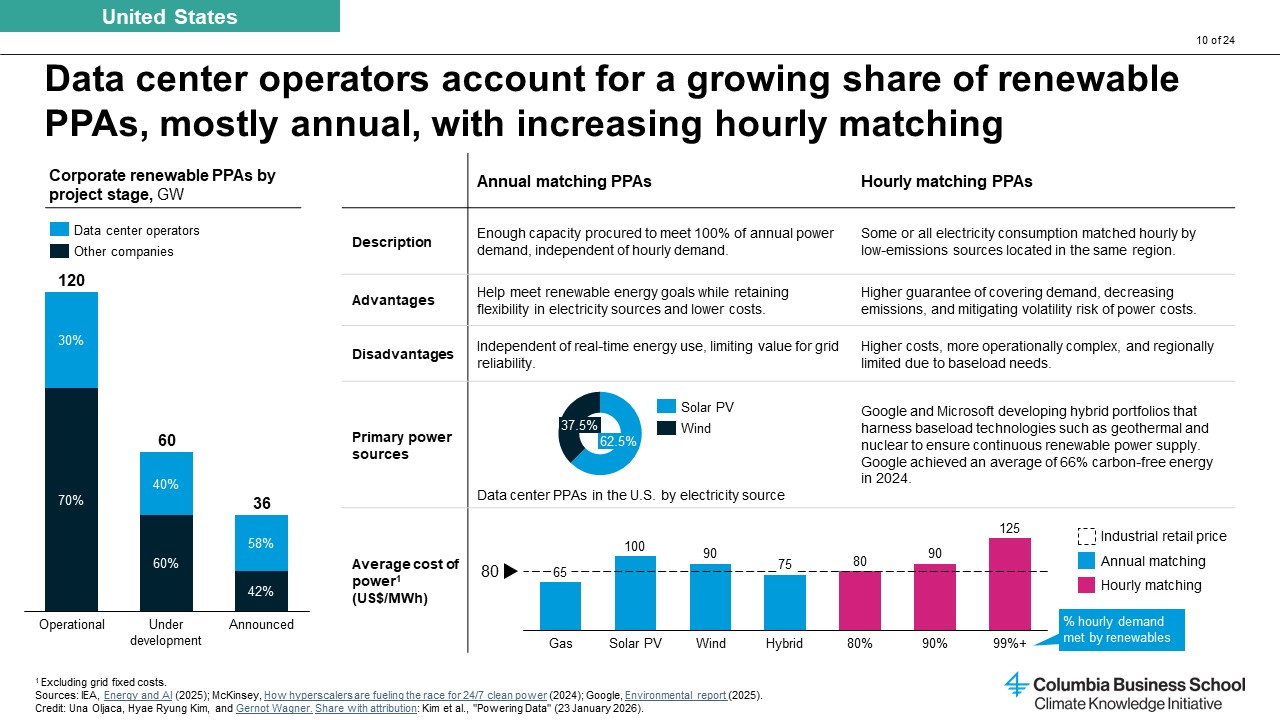

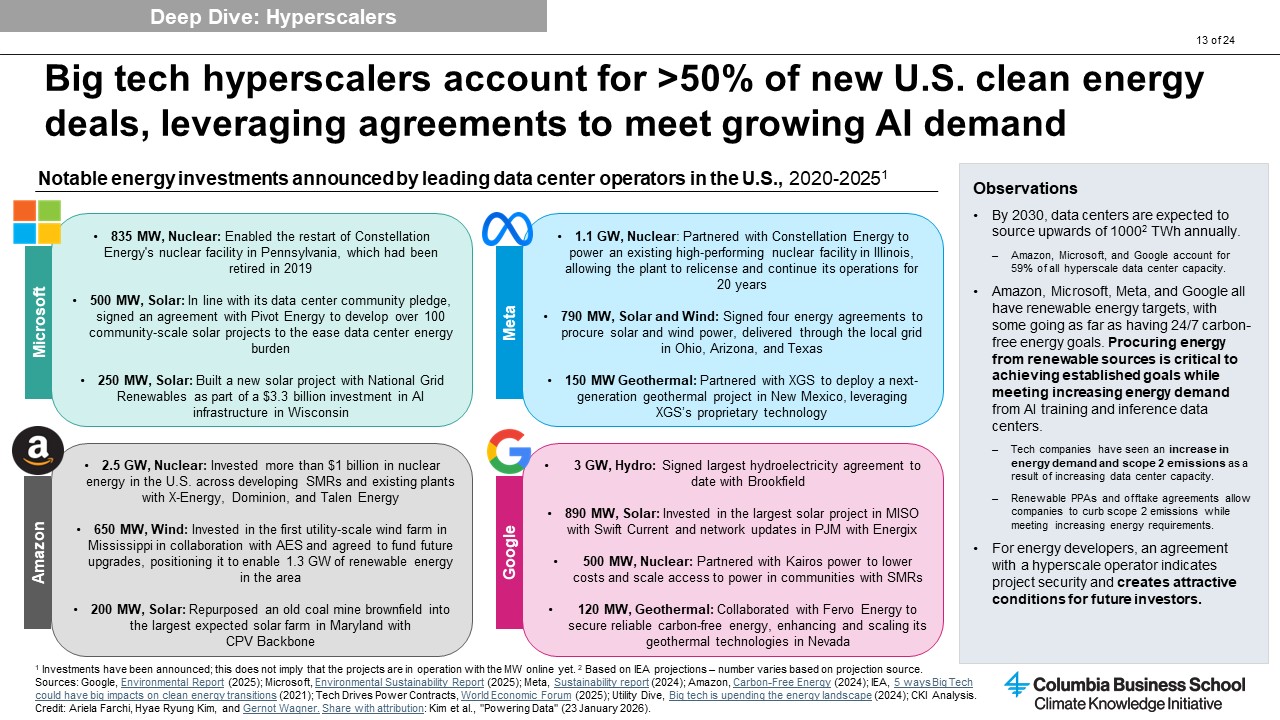

In the United States, Amazon, Microsoft, Google, and Meta account for more than half of all new renewable energy deals. They are using their power as the largest corporate buyers of energy to help finance solar, wind, and, increasingly, geothermal and nuclear projects through long-term PPAs. This creates a powerful, creditworthy demand signal for new clean energy projects.

In the same way data center operators must consider power availability before they begin construction, clean energy developers often need to be backed by firm offtake contracts to get projects financed. The cost of capital might also be lower for robustly backed projects.

There’s innovative financing to some of these contracts themselves, with hourly matched PPAs that ensure that every hour of data center operation is powered by carbon-free electricity, rather than relying on annual averages that can obscure fossil fuel use during certain times of day.

At the same time, utilities like AEP in Ohio and Dominion Energy in Virginia are building in protections to hedge against the uncertainty of a potential AI bubble. These protections include large penalties for contract termination and “take or pay” provisions with 85 percent minimum capacity payments, where data center operators pay for contracted power even if they don't use it.

Beyond financing traditional renewables, hyperscalers are accelerating next-generation energy technologies, including enhanced geothermal systems (EGSs), small modular nuclear reactors (SMRs), and fusion power. Unlike intermittent solar and wind, these technologies could provide firm, 24/7 generation. They’ve also surfaced winners of the Trump administration’s energy-related tax reforms, retaining Biden-era tax incentives under the One Big Beautiful Bill Act.

These emerging technologies are poised to mature faster than they would without the data center energy race, benefiting from investment, debt financing, and offtake agreements from tech companies. However, none are yet delivering commercial power at scale, and it's unclear whether they can deliver power in time to meet the current wave of data center construction, though industry leaders like Fervo (EGSs) and TerraPower (SMRs) claim their first commercial plants will be operational by 2026 and 2030, respectively.

The dirty side of an ‘all of the above’ power rush

The urgency of AI's power demand is driving tech companies to pursue an "all of the above" energy strategy that's breathing new life into the fossil fuel industry and raising costs for consumers.

In regions hosting data center clusters, residential electricity bills are climbing as utilities upgrade infrastructure to meet surging demand. States like New Jersey, Georgia, and Oregon have proposed separate rate classes to protect residents, as wholesale electricity costs near data centers have risen as much as 267 percent compared to five years ago.

Despite renewable energy pledges, tech companies are also turning to natural gas to meet immediate capacity needs, signing contracts that could lock in fossil fuel infrastructure that may outlive the AI workloads it’s meant to serve.

Notably, in October 2025, Google signed the first corporate deal to buy electricity from a natural gas power plant that uses carbon capture and storage (CCS) technology to stop CO2 from being released into the atmosphere as it is produced. Though this strategy technically delivers net zero-carbon electrons, it comes with the moral hazard of extending the operating life—and social license—of gas under the guise of climate action. While CCS has legitimate applications in hard-to-electrify sectors, using it when cheap and deployable clean energy alternatives exist is a misallocation of both technology and capital.

The future of AI energy demand remains highly uncertain, with projections dependent on several contested assumptions. Will inference workloads continue to scale, or will efficiency gains flatten the curve? Will AI adoption sustain its exponential trajectory, or are we in a bubble? If demand falters, will households be left subsidizing overbuilt fossil fuel infrastructure that is locked into decades-long contracts?

It's clear that the AI boom has made Big Tech a key player in the energy system. The question is whether it will accelerate decarbonization or entrench our dependence on fossil fuels for another generation.

We thank Hyae Ryung (Helen) Kim, Una Oljaca, Shubhangi Prasad, Yosafat Partogi Simbolon, and Clara Zibell for research and analysis supporting this article.