Nuclear energy, for all its promise as a safe and reliable source of abundant, clean power, remains dogged by a perception paradox: A 2024 survey found that while a record 78% of the U.S. public now supports the expansion of nuclear energy, even those supporters tend to mistakenly believe their pro stance on nuclear power is a relatively unpopular one.

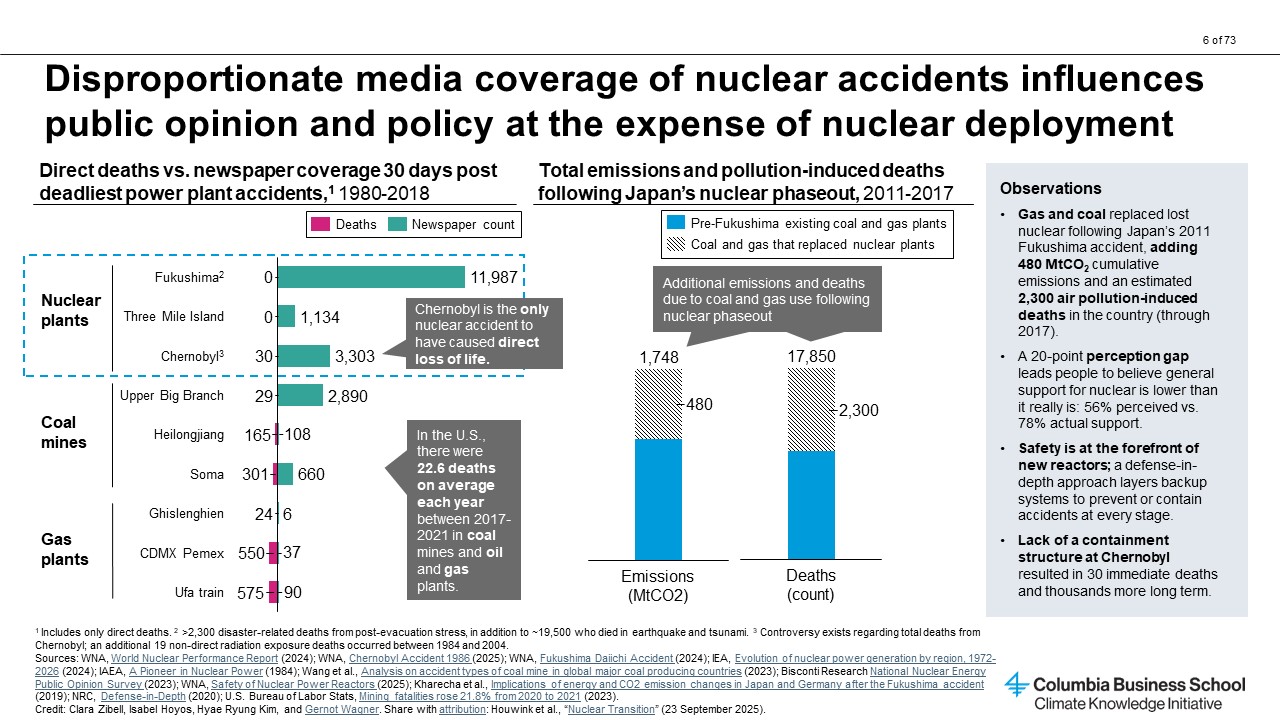

From one perspective, the factors behind nuclear power’s complicated reputation are no mystery: Nuclear plants have been at the center of some high-profile accidents. The largest, in Chernobyl in 1986, resulted in about 30 immediate deaths and thousands more lives lost long term, due to the radioactive contamination that resulted from the lack of a containment structure. In 2011, a tsunami triggered reactor meltdowns and radioactive releases at the Fukushima Daiichi Nuclear Power Plant in Japan, which forced evacuations and led to environmental contamination but no immediate deaths. A partial nuclear meltdown in 1979 at the Three Mile Island Nuclear Generating Station in Pennsylvania kicked up public anxiety though resulted in no deaths.

These incidents have received well-deserved media scrutiny — yet, the amount of media coverage around the events has proved dramatically disproportionate to coverage of far deadlier disasters in coal mines and gas plants during the same time period. This has likely contributed to a widespread perception of nuclear energy’s outsize riskiness and unpopularity.

Learn more about Columbia Business School’s Climate Knowledge Initiative: Nuclear

What’s more, such nuclear disaster coverage fails to take into account, as a point of comparison, the deaths related to air pollution from burning fossil fuels. One analysis, for example, estimated that the gas and coal generation that replaced nuclear after the 2011 Fukushima accident led to roughly 2,300 pollution-induced deaths through 2017. And it also doesn’t take into account the additional CO2 emissions that contribute to global climate change and increase the risk of, among many other things, weather-related disasters, extreme temperatures, and forced displacement.

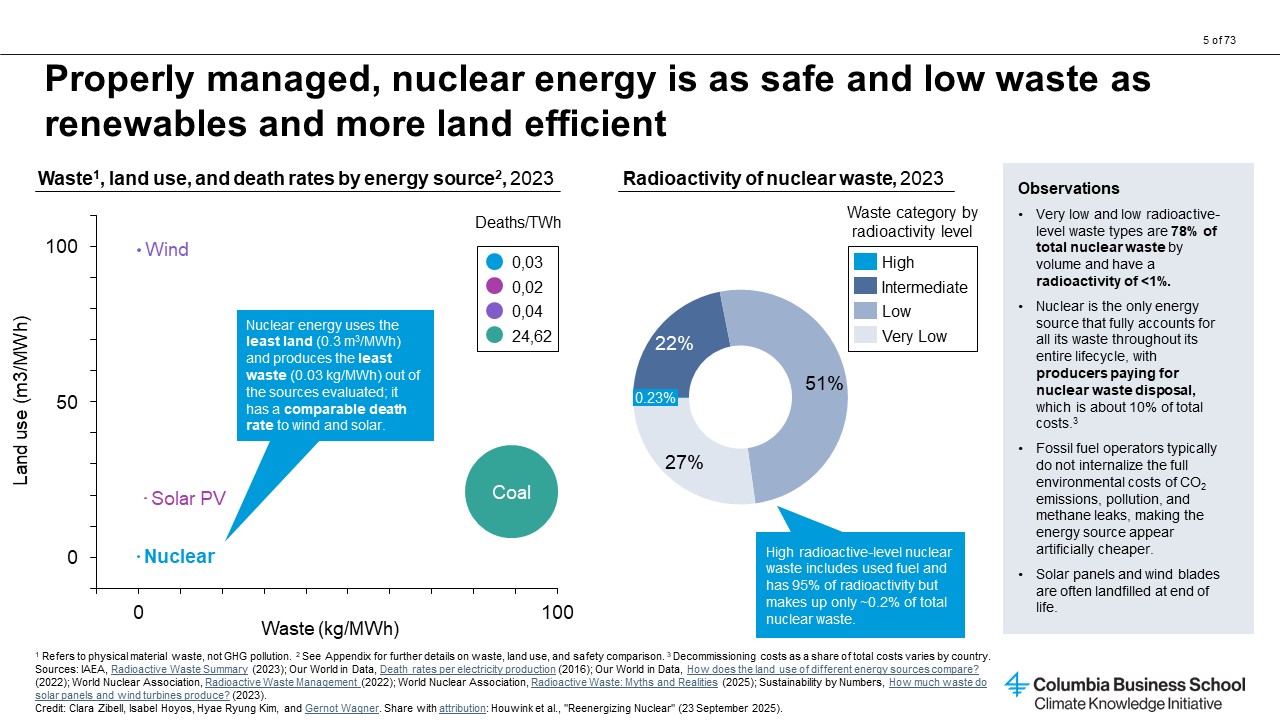

This is why, from another perspective, nuclear power is long overdue for a reputation correction. In fact, nuclear power, when properly managed, produces as little material waste as renewables, and less than 1% of it is highly radioactive. And nuclear producers, unlike fossil fuel producers, pay for their own waste disposal. Nuclear energy also requires far less land than renewables and has comparable low death rates.

Why, then, does deployment of this power source remain hampered by outdated and skewed perceptions of its viability?

After all, nuclear energy has seven decades of established familiarity, and it started strong: Soon after the first nuclear plant began to produce power at scale, in 1954, the energy source contributed a sizable 10% to 20% share of global power generation. But that share has largely stagnated, especially in the West, and today, nuclear energy accounts for only 9% of the global power supply.

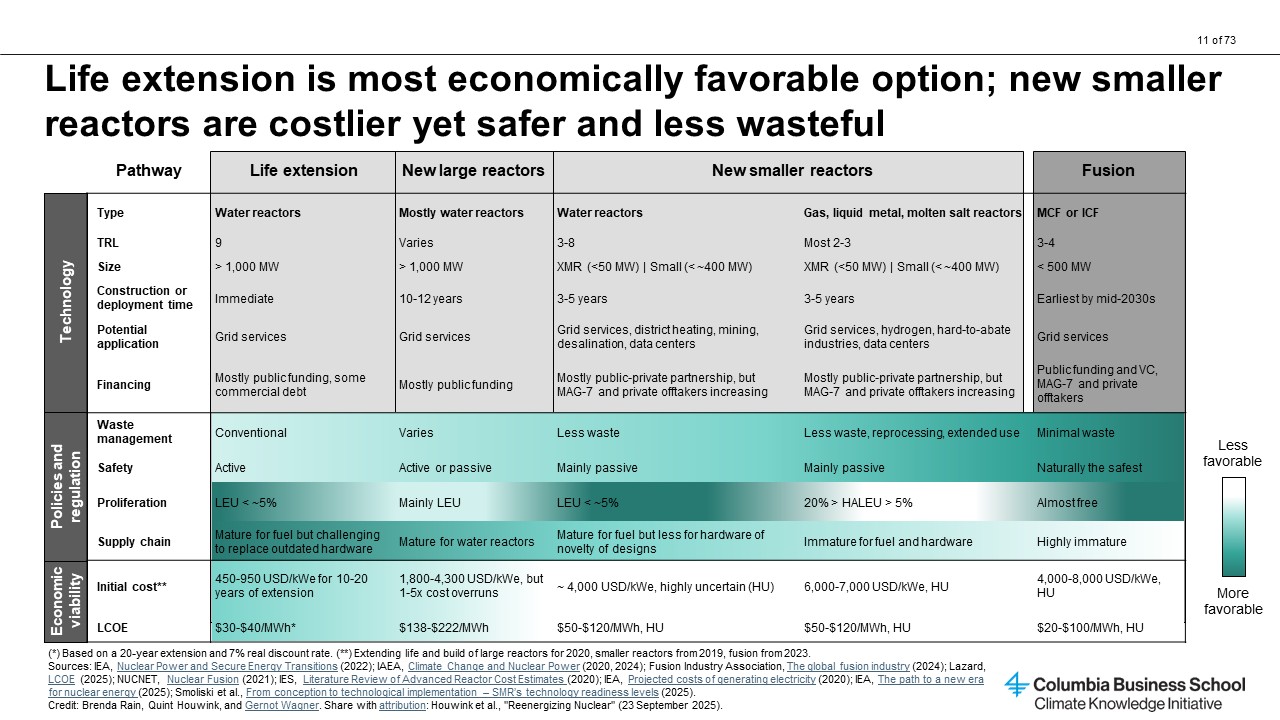

The explanations for why nuclear power deployment has stalled extend far beyond its perception problems. To understand nuclear’s current barriers — as well as the steps necessary to reenergize the energy source — it’s critical to first define what exactly constitutes nuclear development today, which is largely occurring across four distinct pathways.

- Building large nuclear reactors.

With electrical capacity of 1,000 MW or more, large reactors largely rely on mature, water-based technology to provide baseload power to national grids. Today’s global nuclear capacity is almost 400 GW, all of it provided by large, ~1 GW-size reactors. That figure is set to double if all plants currently under construction or announced are realized. However, such construction projects have developed a reputation for major cost and time overruns, which has compounded the difficulty of financing them.

- Extending lifetimes of existing reactors.

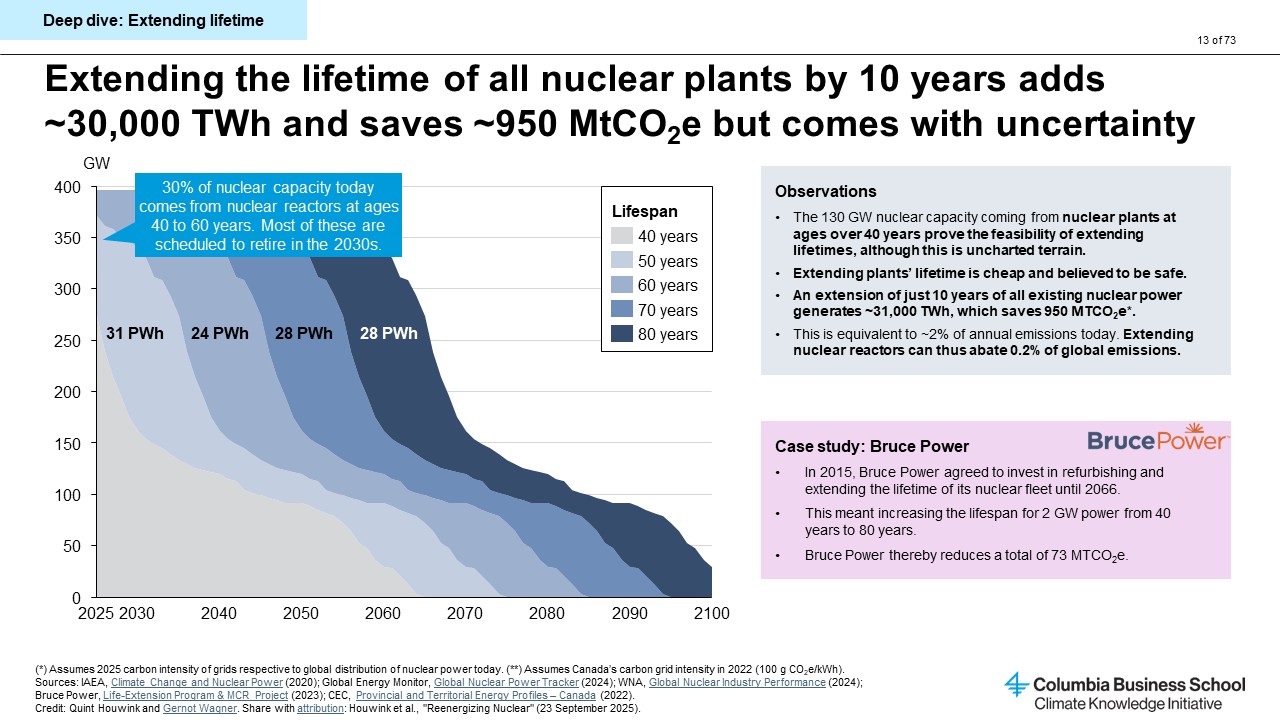

The U.S. Nuclear Regulatory Commission provides initial licenses of 40 years to nuclear power plants. This timeline was never meant to indicate the complete lifespan for the plants but to allow them to recoup their initial investment. Still, many plants are scheduled to retire at around 40 to 60 years of age, despite the potential to continue producing energy after some cheap refurbishments.

With nearly one-third of the world’s current nuclear capacity generated by nuclear reactors 40 to 60 years old and set to retire in the coming years, extending the lifetimes of existing reactors is likely to be the cheapest and fastest way to increase the world’s share of nuclear power.

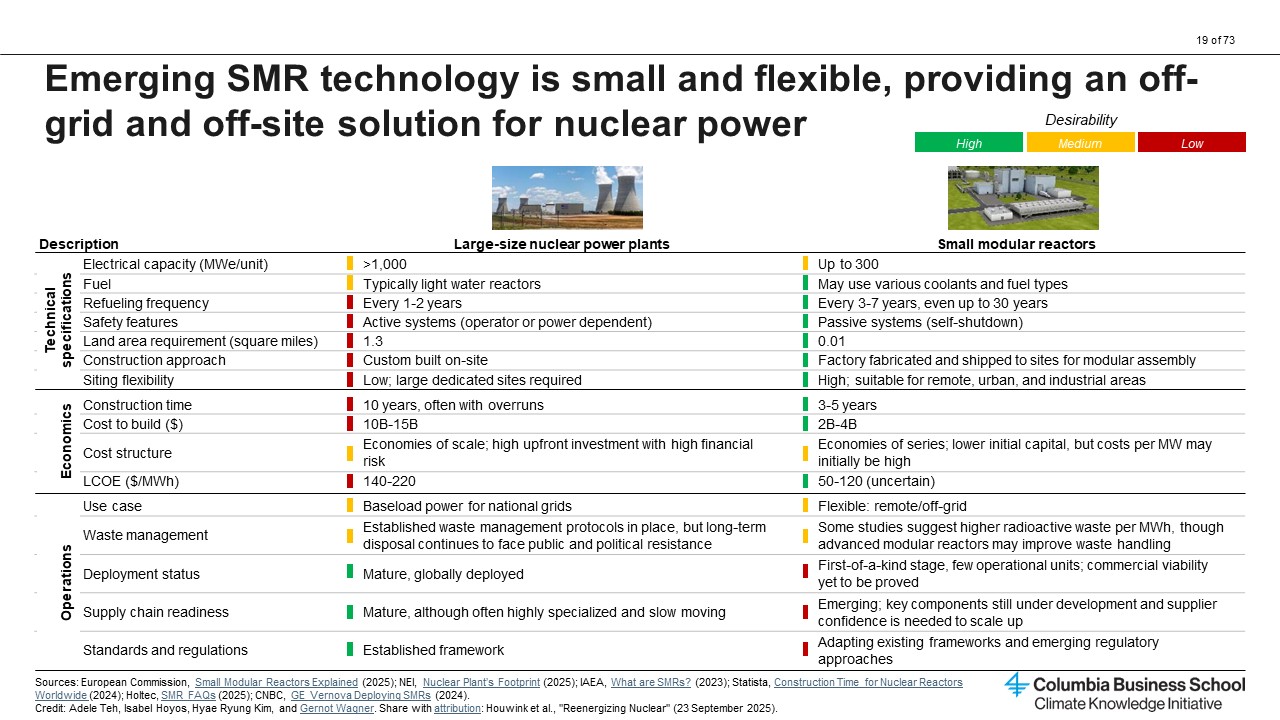

- Developing and commercializing small modular reactors (SMRs) and microreactors.

SMRs, with up to 300 MW capacity, and microreactors, with up to 50 MW capacity, are currently in early stages of development, with none yet commercially deployed in the United States as of July 2025. Therefore, any estimates of their likely costs are based on literature, not real-world data.

Even so, the potential advantages of installing SMRs and microreactors instead of larger reactors have generated significant excitement — especially among massive data center operators whose energy needs are multiplying exponentially thanks to artificial intelligence. Unlike large reactors, SMRs and microreactors will be much more flexible in their siting options, opening up the potential for positioning close to data centers.

- Pursuing fusion energy.

The fusion process produces energy using an operation fundamentally distinct from that of nuclear fission: Fusion fuses two nuclei, while fission splits an atom apart. In theory, fusion can generate up to eight times more energy than fission from 1 kilogram of fuel. The fuels for this process are relatively light and non- to low-radioactive deuterium and tritium, the former naturally abundant in seawater and the latter produced as a byproduct of either fission or fusion reactions.

Fusion proponents emphasize its relative safety, since unlike fission, fusion reactions don't involve a chain reaction. This means that if something were to go wrong in the process, it couldn’t prompt a cascade of uncontrolled energy release.

For these reasons, fusion holds great promise as an abundant source of clean energy, but it is still just a promise. Despite billions of dollars in investment and some scientific breakthroughs, no company has yet to prove fusion energy is viable. That means realizing its promise is still conditional on establishing the science, not to mention achieving commercialization. Commercially available fusion energy is still at least a decade away, by optimistic estimates.

Each of these pathways to nuclear energy development comes with its own promises and perils — and each will require a specialized set of solutions. Read on for four key points about the state of nuclear today, along with its attendant hype and hang-ups.

Key Insight 1: Large-scale nuclear reactor technology may be established and plug and play, but project risk is massive, and appetite to overcome that risk, in many parts of the world, is small.

Large-scale nuclear plants are beset by a reputation risk separate from the accident-related anxieties spurred by Chernobyl and Fukushima. They are also hampered by their financial risks.

Many cite Plant Vogtle in Waynesboro, Georgia — the largest nuclear plant in the United States — as a prime case study. Vogtle’s first two units were constructed in the 1980s, and the initial capital investment estimate of $660 million mushroomed by more than a factor of 10 to $8.87 billion.

In 2009, construction began on two additional units at Vogtle, using Westinghouse AP1000 reactors. Unit 3 was completed in 2023 and Unit 4 in 2024. The costs for these units were initially projected to be $14 billion; by 2023, costs had more than doubled to $34 billion. These cost overruns and construction delays were cited as a major contributor to the bankruptcy of Westinghouse in 2017.

“Building a nuclear plant is like a snake eating a horse,” says David Victor, a professor of innovation and public policy at the University of California San Diego and co-director of UCSD’s Deep Decarbonization Initiative. “It’s a bet-the-balance-sheet proposition. If the CEO of a utility wants to retain his or her job, they’re just not going to announce a new nuclear reactor.”

Compounding the hesitation to finance large nuclear plants is the fact that, in many parts of the world, particularly in the United States, the steady growth of electricity demand throughout the past decades was not significant enough to justify massive investments in new nuclear plants. That no longer holds true, as demand from data centers is projected to grow rapidly in the next decade (though hyperscalers appear to have more of an appetite for small and microreactors than large, 1 GW-size reactors).

What’s more, other clean sources of energy like solar have gotten much cheaper, fast, while standing up new nuclear plants has not. Even factoring in the costs of battery storage on top of intermittent renewables like wind and solar doesn’t quite bring their costs as high as nuclear’s — and the cost of battery storage, too, continues to fall.

All this points to the fairly simple question looming over most discussions about the development of large nuclear reactors: Who’s going to pay?

Stephen Comello, executive director of the Nuclear Scaling Initiative at the EFI Foundation, argues that blended finance arrangements will be critical in breaking down financing barriers and building the next generation of nuclear plants.

Comello points with some optimism to the June 2025 announcement that New York Governor Kathy Hochul has directed the New York Power Authority (NYPA) to develop a nuclear power plant in the state with at least 1 GW capacity.

“I believe that with this kind of risk, there should be public-private risk sharing,” Comello says. “I’m really excited about what NYPA is doing, because that’s a situation where you could have a public entity take on some of that non-commercially acceptable risk.”

Key Insight 2: Extending the lifetimes of existing nuclear plants is a cheaper and faster means of building capacity than developing new plants. However, securing stronger public and political acceptance of nuclear energy is pivotal here, too.

Extending the lifetimes of all existing nuclear plants by just 10 years would generate an estimated 31,000 additional TWh of energy, thereby saving about 950 metric tons of CO2 emissions — equivalent to 2% of today’s annual emissions.

This would require relatively cheap and safe refurbishments to standing power plants — at least, that’s the broadly shared belief, as this approach is still uncharted terrain.

“There’s a lot of boring but really important stuff happening with regard to innovating around extending the lifetimes of existing fleets,” says Victor. He cites as an example the development of robots that can inspect and make repairs in older nuclear plants.

In the past few years, a small number of shuttered nuclear plants in the United States have been mentioned as candidates for reopening, including the Three Mile Island power plant near Middletown, Pennsylvania, which was shut down in 2019 because of economic pressures like record-low natural gas prices and competition from other renewable energy sources.

What’s needed to push more decommissioned and soon-to-retire nuclear plants to follow suit? The answer actually has little to do with economics or engineering and almost everything to do with politics, says Mark Nelson, founder and managing director of Radiant Energy Group.

After all, he says, “once a nuclear reactor is built, it is essentially immortal” — as long as it isn’t closed down by regulators.

He points to Germany as an example, where the government imposed a “nuclear phaseout” soon after the Fukushima disaster, responding to broad public concern about nuclear plants’ safety. This represented a dramatic political U-turn in the ultra-green country; until 2011, Germany had procured a quarter of its electricity from nuclear energy.

In 2022, the German government altered its plan, announcing that the country’s remaining three operational nuclear reactors would operate through early 2023 to reduce dependence on Russia’s gas supply.

More recently, debates have heated up again about whether the country’s shuttered reactors should be reopened, amid continued concerns about energy security, rising electricity prices, and an acknowledgment that Germany’s use of imported fossil fuels has increased since the nuclear phaseout.

In 2025, the country’s conservative Christian Democratic Union (CDU) party called for the reopening of up to six of the shuttered plants. As Nelson emphasizes tends to be the case elsewhere, the main obstacles in Germany’s situation are political and regulatory, not technical.

Regardless of where in the world a decommissioned nuclear plant may be, many experts agree that the key to mustering the political will to reopen it is the stance of communities nearby.

“Politics is a dynamic problem — and an opportunity,” says UCSD’s Victor. “The most important part is getting support from local communities: organized labor, the firefighters’ union, schools. Even though the opposition is super-well organized, nuclear power often has built-in political support.”

John Shingledecker, principal technical executive at the Electric Power Research Institute, echoed this sentiment about the importance of community buy-in. He says redeveloping a site that was formerly a coal plant or restarting a shut-down reactor comes with a built-in advantage: It means keeping a plant rooted in a community that is accustomed to it and has been reliant, at least at one time, on its jobs.

Heike Freund, chief operating officer at Marvel Fusion, says such logic has guided her team’s decision-making, too, in terms of determining where to establish prototype plants for the generation of fusion energy.

“One area we are looking at to use as a location for fusion prototypes are shut-down nuclear fission power plants, because there, you already have a population of people who have lost jobs because the power plants have been shut down and they would be interested in having jobs being created there again,” Freund says. “[In comparison], if we build the prototype on a greenfield near a population that has not been exposed to nuclear in the past, we’d expect to see a lot more resistance.”

Key Insight 3: New and promising technologies come with significant potential tech risk but also offer high-risk, high-reward economics comparable to other types of venture capital investments.

Emerging technologies like SMRs present a set of challenges that invert those posed by large nuclear reactors: While building a large nuclear plant is a known quantity and technologically safe, it’s a highly risky financial proposition because of unpredictability and cost overruns. In contrast, SMRs still pose plenty of tech risks, but their upfront financing costs are comparatively low — and therefore more attractive to VC investors and other private capital.

In addition, energy finance experts explain that while large nuclear plants demand economies of scale (that is, high upfront investment), emerging tech like SMRs calls for economies of series — referring to the fact that while the first-of-a-kind versions of SMRs may be costly, they are also likely to benefit from swifter learning rates and cost reductions via the repetitive production of many standardized units.

Such financing perks have stoked excitement around SMRs in particular — despite the fact that none have yet been commercially deployed. SMRs also come with functional benefits that are attracting eager attention from investors and other major players, including hyperscalers with mushrooming energy demands, like Microsoft. In particular, many of these tech companies appreciate the smaller reactors’ siting flexibility as well as their scalability.

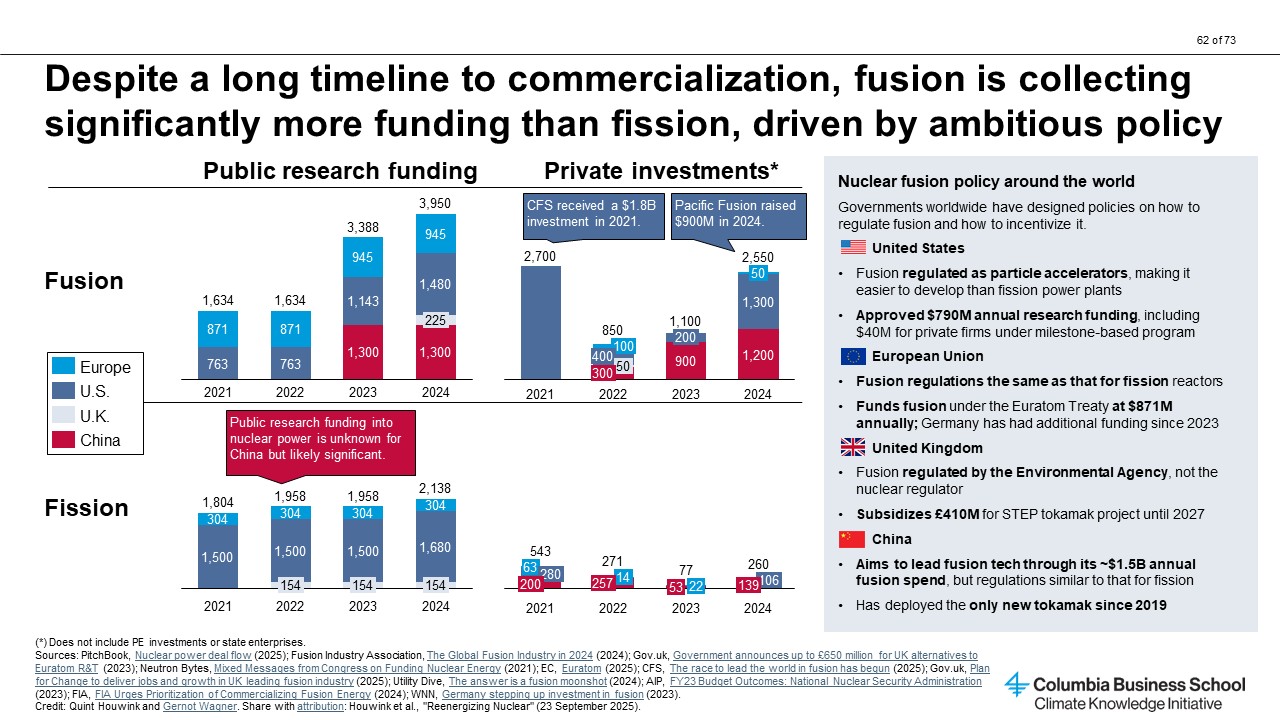

Given this excitement, significant private investment is flowing into emerging technologies like SMRs and XMRs — as well as fusion energy, which is even more nascent in establishing the science undergirding generation.

Some observers in the energy space are nervous about the implications for nuclear development more broadly. “I think there’s a disconnect where you’ve got the highest volumes of money flowing into the highest risk technologies, because it’s a different business model,” says Victor.

Given the interest from private funders, the number of startups tackling both SMR and XMR projects and fusion energy is on the rise. Marvel Fusion’s Freund says although her industry is still focused on finding a technical solution that is reliably producing energy, there are currently about 50 private fusion companies globally — proliferation comparable to the activity in the SMR space, she notes. Freund says fusion companies have collectively received roughly $8 billion in private funding, the majority of it over the past three years. (Most of these companies have collected $50 million or less in funding, while a couple of major players have received far more sizable chunks, like Commonwealth Fusion Systems, which has received roughly $2 billion in funding.)

Freund expects that the next stage for the fusion space will be a commercial consolidation, with no more than about 15 companies receiving sufficient funding to proceed to the next stage of growth.

“I would say maybe we’ll see 15 companies build a tech demonstrator,” she predicts. Of those 15, maybe five will build something that could be a prototype of a power-generating machine, and then maybe one to three will turn that into a power plant.”

Many experts point out that the elephant in the room for all these new tech builds, whether fusion or SMRs, is, “Who eats the first-of-a-kind costs?”

Comello of the EFI Foundation proposes a buyer’s club, similar to the advanced market commitments used by the COVAX coalition for vaccines and, more recently, by Stripe for carbon removal. Nuclear projects need a large and credible orderbook to bring costs down, but such an orderbook is often too large and risky for any single buyer; by pooling demand, a buyers’ club could give developers the confidence to invest.

Some experts express hesitation about whether a buyers’ club for ushering along the development and deployment of new nuclear technologies could achieve sufficient scale. No matter what, most agree that governments will likely need to step in and provide sizable funding support for any first-of-a-kind development in nuclear energy, where market perils have proved to be nearly equal to the energy source’s promises. One challenge will be ensuring that government officials don’t pick favorites among the pathways toward nuclear energy but instead enable a diverse energy ecosystem to flourish.

Learn more about Columbia Business School’s Climate Knowledge Initiative: Nuclear

We thank Quint Houwink, Adele Teh, Hinako Arai, Vedant Bhansali, Khande-Jaé Fisher, Brenda Rain, Christian Sandjaja, Clara Zibell, Hyae Ryung Kim, and Isabel Hoyos for research and analysis supporting this article.