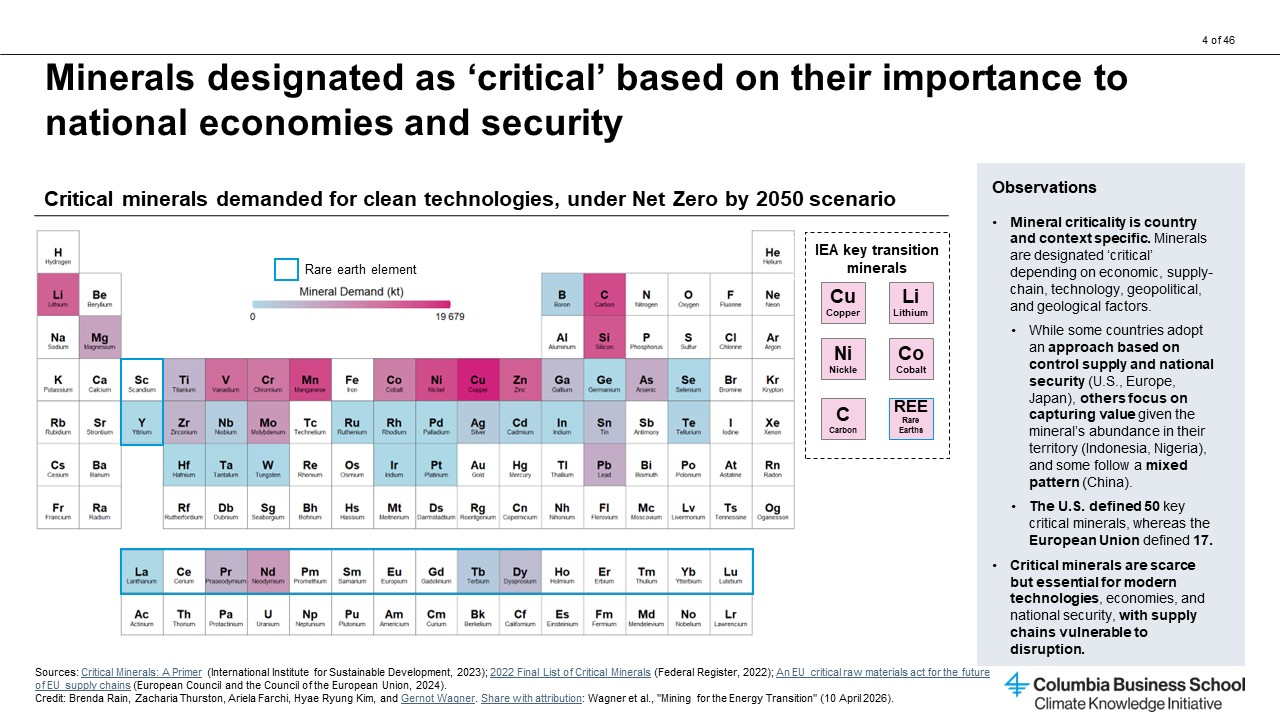

Rare earth elements (REEs) are a fixed and globally consistent group of 17 metals that sit together in the periodic table—atomic numbers 57 through 71, plus adjacent 21 and 39. They are classified based on similar chemical properties, and though they’re not scarce in the earth’s crust, their deposits are rarely concentrated enough for economical extraction, thus, earning the description rare.

Some, but not all, REEs are also considered critical minerals, a dynamic and political—though not scientific—classification that changes by country and over time. The 2025 U.S. list of critical minerals totals 60 (10 more than the previous one, released in 2022); the latest EU list, published in 2023, identifies 34.

Critical minerals are generally defined as those indispensable to a nation’s economy and vulnerable to supply chain disruptions. But the focus can vary. For example, the United States’ definition emphasizes national security while the EU’s explicitly names renewable energy as a sector of critical importance.

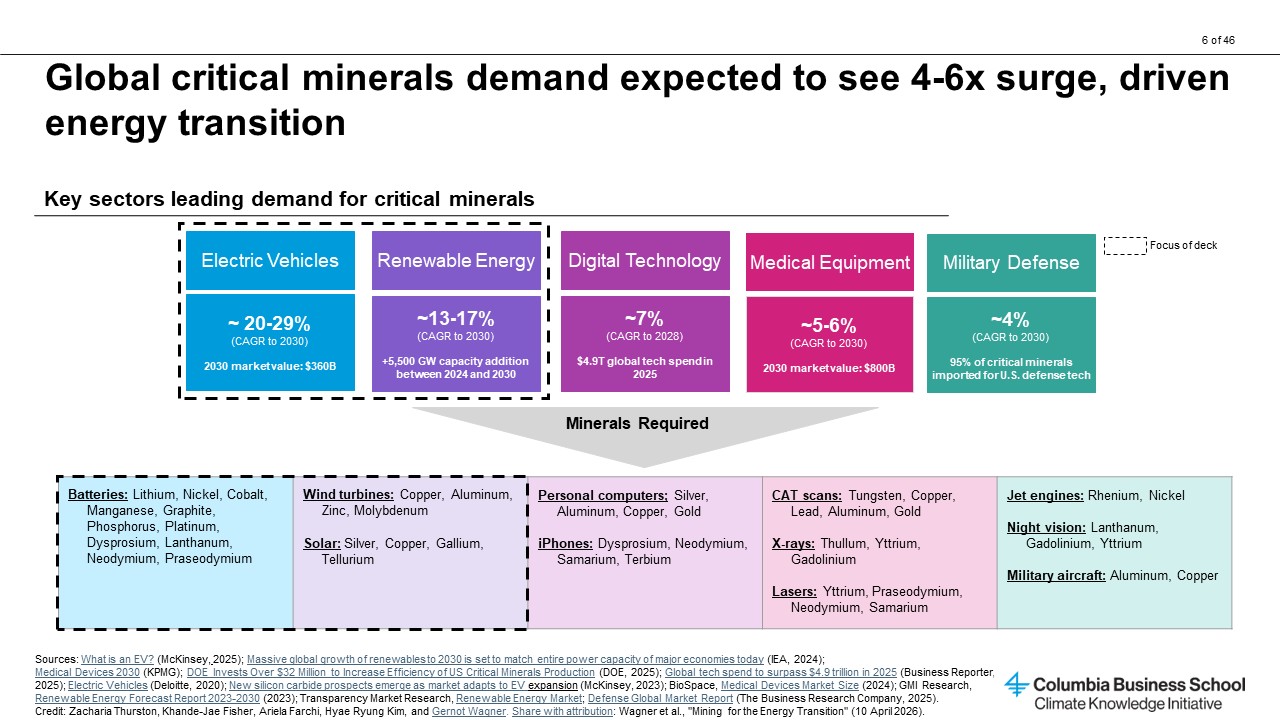

Climate-motivated or not, the Trump administration’s campaign to shore up mineral supply chains is mission critical to the energy transition. The biggest end users of critical minerals are companies that produce technologies such as solar panels and batteries, including those that power electric vehicles, making lithium, cobalt, copper, and nickel the physical foundation of clean infrastructure.

Key Insight #1: Critical minerals are the building blocks of clean technology

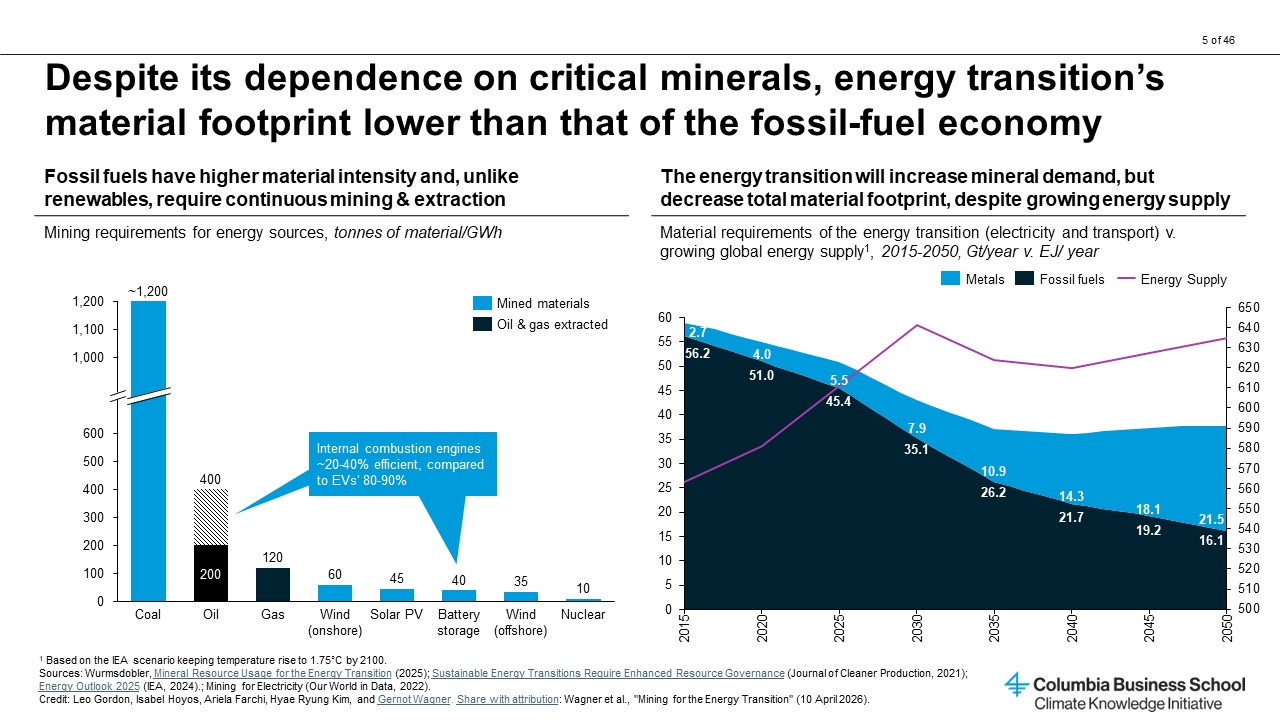

The reality that electrification results in increased global mineral demand is undeniable and unavoidable. Building an EV requires six times the mineral input of a conventional car, and a wind power plant requires nine times the mineral content of a gas plant.

Under current electrification trends, the International Energy Agency expects demand for lithium to rise about 4.5-fold by 2040 and demand for nickel, cobalt, and graphite to increase by a factor of 1 to 2. Electric vehicles will drive most of the growth, as these critical minerals are essential components of batteries. In fact, EV batteries alone already account for roughly one-third of today’s total mineral demand. Renewables are a close second, with copper, zinc, and silicon being key inputs.

Supplying critical minerals sustainably is an environmental challenge, but it is far from an insurmountable one.

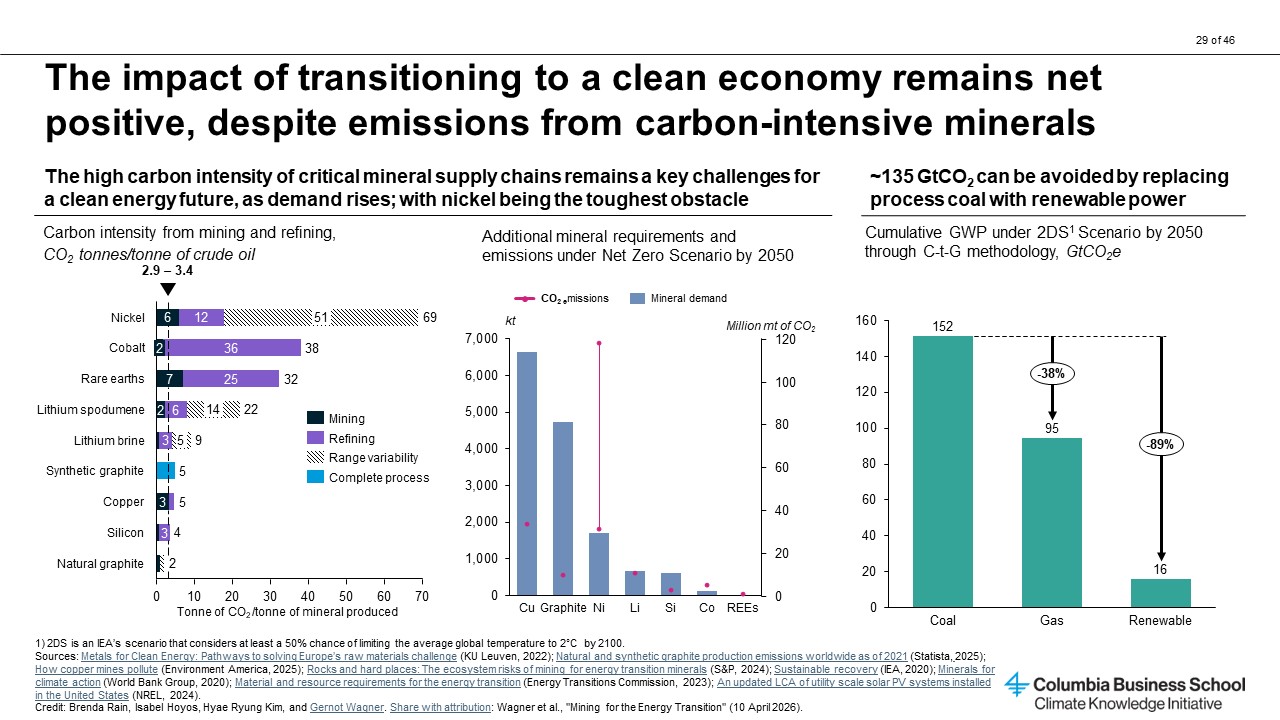

For one, even though most of this demand is front-loaded, the total material requirement of a net zero scenario economy is almost 30 percent less than today’s predominantly fossil fuel-based one. The coming decades will demand an enormous volume of mineral materials for an upfront build-out of EV fleets, wind farms, solar panels, long-distance transmissions, and stationary battery storage. But critical minerals are infrastructure, while today’s hydrocarbons must be burned continuously to power the world.

Key Insight #2: Midstream supply chain consolidation is a production constraint and geopolitical hazard

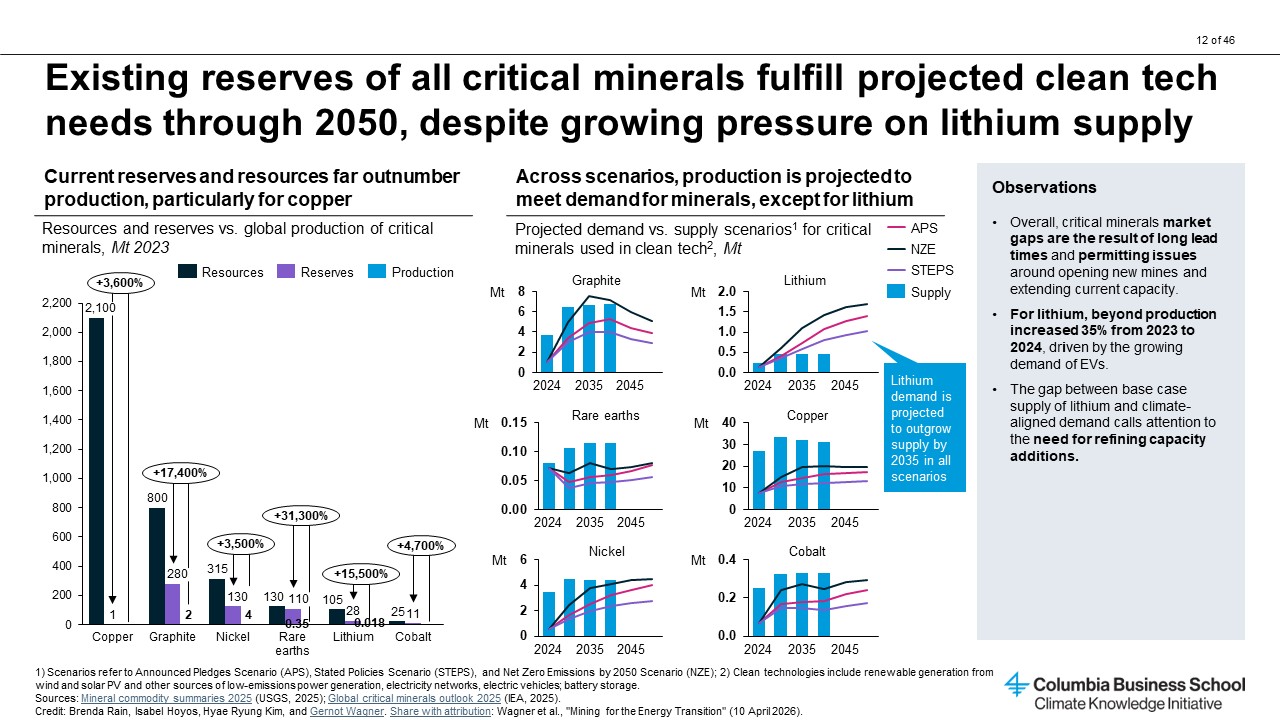

There are currently enough known reserves to meet the projected needs of clean energy technologies through mid-century, but the gap between demand and production is widening—mining, refining, and transport infrastructure will need to scale by three to five times.

While mining investment has accelerated, the bottleneck lies in the midstream. The supply of mined lithium, for example, increased 35 percent in 2024, yet refining capacity has not kept up with the pace of battery manufacturing growth. Moreover, refining and processing capacity is highly concentrated.

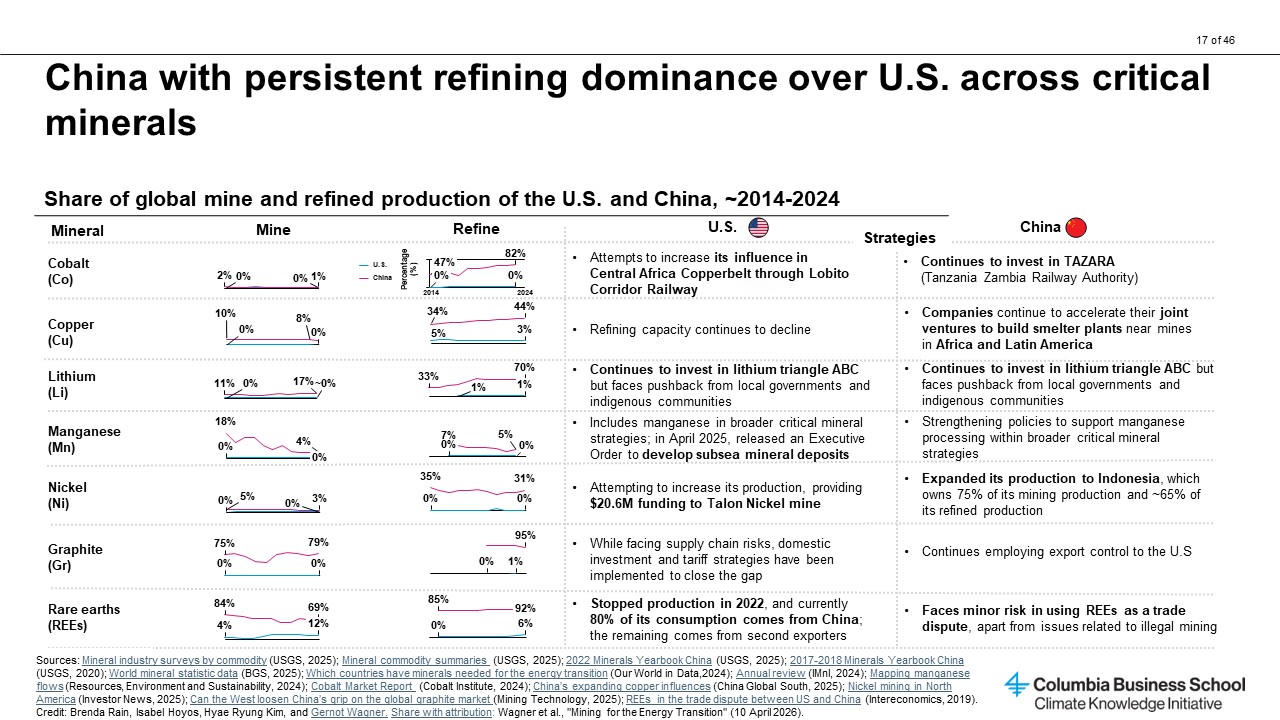

China currently refines over 90 percent of rare earth minerals and graphite, 65 percent of nickel, and nearly 50 percent of copper globally. It also dominates the processing of battery cathode and anode materials and other components, maintaining disproportionate control over clean energy supply chains.

In response, nations are pursuing diversification strategies: Indonesia is scaling nickel refining; the United States and the European Union are offering incentives for domestic processing; and international partnerships are forming in an aim to reduce reliance on China’s midstream dominance.

The U.S.-Ukraine Reconstruction Investment Fund is a recent example: a 50/50 comanaged fund focused on postwar rebuilding through investments in mining, energy, and infrastructure. With Ukraine’s critical mineral reserves valued at over $350 billion—many located in conflict-prone eastern regions—the deal underscores the geopolitical importance of resource access.

The agreement offers tax and tariff exemptions and commits Ukraine to channel 50 percent of revenues from new projects into the fund while retaining full ownership of existing assets. The United States provides military aid and gains commercial priority through offtake rights and first-refusal mechanisms, administered by the U.S. International Development Finance Corporation.

More broadly, the deal reflects a shift toward state-backed strategies to secure mineral access, reduce reliance on China and Russia, and build resilient, friend-shored supply chains. Critical minerals are not just industrial inputs but strategic assets tied to national security, foreign policy, and economic resilience, at the center stage of global finance and diplomacy. The environmental and social costs of mining, though substantial, are significantly smaller than those of the fossil-fueled economy, and that does not even count the costs of unmitigated climate change.

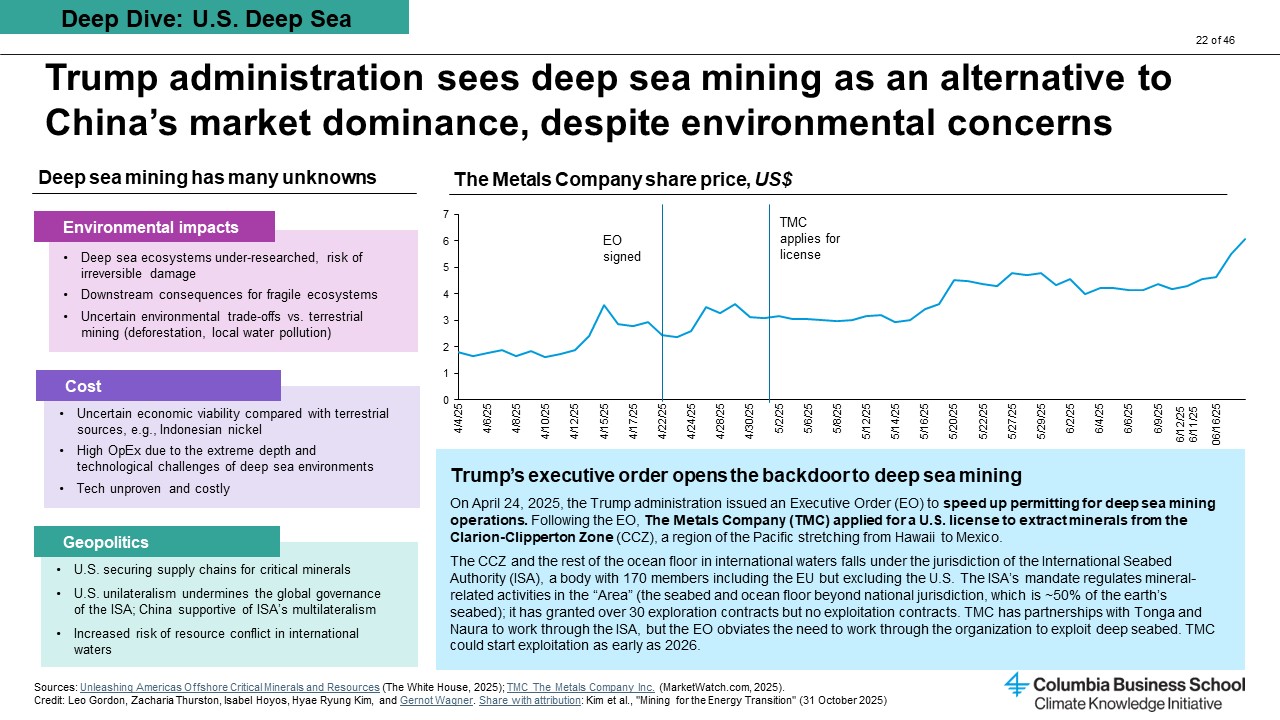

As terrestrial ore grades decline—exacerbated by climate-driven droughts and floods—and extraction grows more energy- and water-intensive, the deep sea is increasingly becoming a geopolitical front line. Seabed regions like the Clarion-Clipperton Zone (CCZ), spanning Hawaii to Mexico, are rich in high-grade polymetallic nodules containing cobalt, nickel, copper, and rare earth minerals vital to clean energy technologies, offering a potential high-purity alternative to constrained terrestrial sources.

Momentum accelerated after an April 2025 U.S. executive order streamlined permitting for deep sea mining, allowing U.S. companies such as The Metals Company (TMC) to bypass traditional international frameworks. While most of the CCZ lies in waters governed by the International Seabed Authority (ISA), the United States, which is not a member of the organization, has opted for a more unilateral approach, raising legal and geopolitical tensions.

The environmental and governance risks of this exploration should not be understated. The deep sea hosts fragile, poorly understood ecosystems, and mining could cause irreversible harm to biodiversity. The economics remain uncertain, especially against cost-competitive terrestrial alternatives like Indonesian nickel. And the political risks are substantial, with unilateral U.S. actions potentially undermining ISA authority and inflaming geopolitical tensions with China and other countries.

But environmental and social concerns are not limited to deep sea mining. Mining metals often produces tailings that can contaminate local water supplies; refining requires substantial energy, which often comes from fossil sources; and mineral supply chains often have a high exposure to child labor and unsafe working conditions.

Climate change is making mining even harder. Many of the world’s richest mineral reserves are in climate-vulnerable areas. An estimated 30 to 50 percent of global copper, gold, iron ore, and zinc production already occurs in regions facing high water stress. In Chile, the world’s leading copper and lithium producer, megadrought conditions have forced companies like Anglo American and BHP to invest billions of dollars in desalination and water recycling infrastructure.

As mines age, ore grades decline, requiring more energy, water, and land to extract the same amount of metal. This drives up costs, increases emissions, and intensifies pressure on already scarce resources. Because critical minerals are vital for clean energy, more materials must be mined and processed, increasing tailings, land disturbance, and energy use in regions often still reliant on fossil fuels.

The convergence of declining ore quality, climate stress, and community conflict threatens mineral supply chain stability. Meeting future demand will require industry-wide shifts toward sustainable, equitable, and climate-resilient mining practices.

Key Insight #3: Circularity could ease supply chain pressures and reduce the environmental and social footprint of critical minerals production

Even if the world could mine fast enough to meet clean energy demand, doing so would be expensive, risky, and politically fraught. Material efficiency, substitution, and recycling are underutilized levers for critical minerals supply.

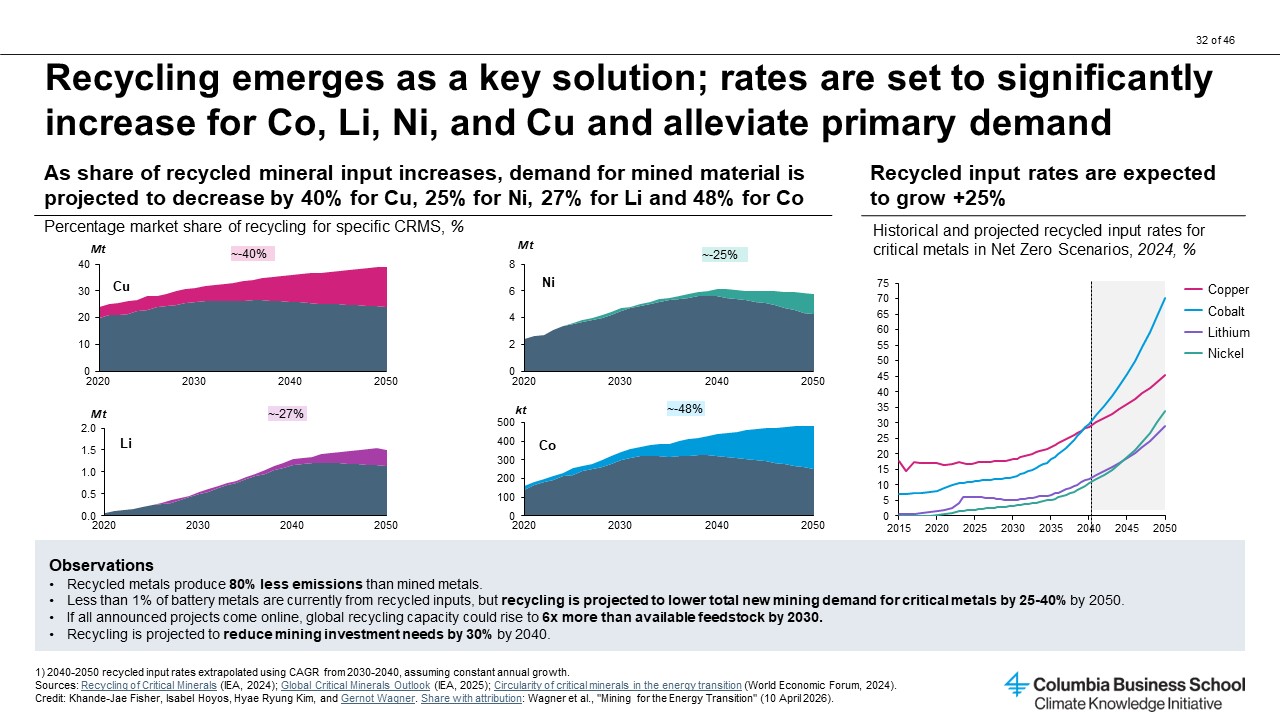

By 2050, recycling could reduce the need for new mining of copper and cobalt by 35 percent, lithium by over 20 percent, and nickel by 15 percent—yet less than 1 percent of these materials are currently recovered. Barriers include fragmented supply chains, limited disassembly infrastructure, and the lack of clear product standards. Heterogeneous waste streams and low mineral concentrations in end products make recovery costly and inefficient.

China’s battery recycling mandates and the EU’s Battery Passport initiative are promising steps, but they remain the exception. While most countries have enacted some form of Extended Producer Responsibility policy, only a few combine financial incentives with comprehensive recovery strategies. To close the gap, governments must push policy to embed circularity from design to disposal, and the private sector must innovate across the entire product lifecycle.

Business models will need to innovate, too. One example: China’s NIO battery-swapping model allows closed-loop collection of spent batteries by selling the battery separately from the vehicle, retaining ownership, and streamlining end-of-life recovery. In the United States, Nth Cycle’s electroextraction technology can be co-located with recyclers, reducing refining emissions by up to 44 percent and shortening supply chains.

The transition from fossil fuels to clean energy is also a transition in the physical economy, from short-lived combustion to long-lived infrastructure. Achieving a net zero future will depend not only on innovation in energy systems, but on a reimagining of how we mine, move, and reuse the materials that sustain it.

We thank Hyae Ryung (Helen) Kim, Ariela Farchi, Khande-Jae Fisher, Leo Gordon, and Brenda Rain for research and analysis supporting this article.

Zacharia Thurston contributed to this work in his capacity as CKI Fellow.