Steel Sector Trends

India is one of the fastest growing steel producers, and set to continue use of blast furnaces to meet rapid demand

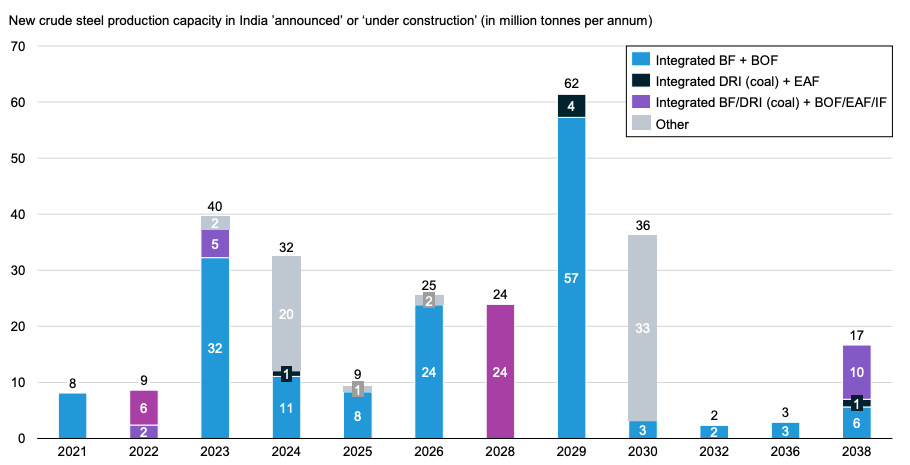

India’s new crude steel production capacity (2021 – 2038E)

Source: India Steel – The Indian Steel Industry. Climate Policy Initiative – Taking Stock of Steel. Credit: Max de Boer, Grace Frascati & Gernot Wagner (22 February 2024); share/adapt with attribution.

Contact: [email protected]

Observations

- India is now the world’s second largest producer of crude steel, and it has typically been a net exporter post FY2016-17, apart from economic downturns

- Because of continued investment, India’s steel making capacity is expected to hit 300 mm tonnes per annum by 2030-31

- To meet demand, India is set to build at least 200 MTPA of new fossil-fuel based, emission-intensive steel production capacity over the next 15 years

- 68% of this capacity is expected to be blast furnaces

- Remaining 32% expected to be from other processes like integrated BF + BOF

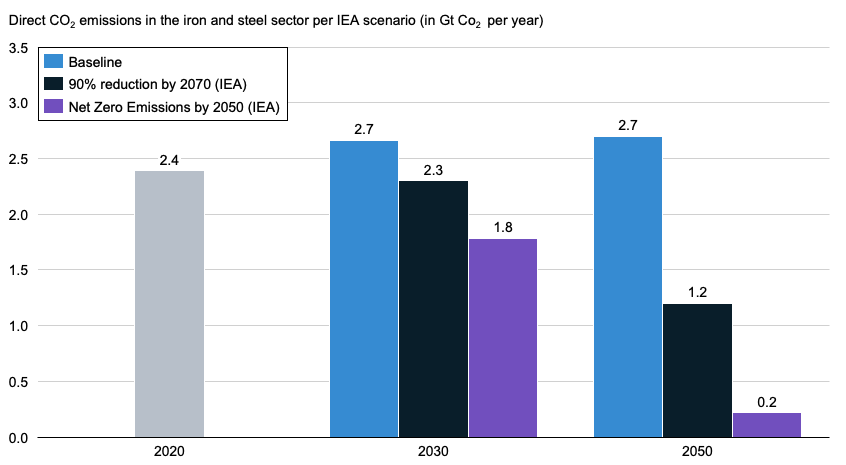

Global iron and steel emissions expected to rise without intervention; future reduction scenarios will require drastic cuts

Only with intervention will CO2e from iron and steel decline into 2050

Notes: Baseline scenario reflects the policies and implementing measures that have been adopted as of September 2022 NZE = Net Zero Emissions. Source: IEA (2020), IEA Net Zero by 2050 (2021),

IEA Iron and Steel Technology Roadmap (2020), McKinsey (2023). Credit: Mimi Khawsam-ang, Max de Boer, Grace Frascati & Gernot Wagner (22 February 2024); share/adapt with attribution.

Contact: [email protected]

Observations

- If no action is taken, global emissions from the iron and steel sector are expected to peak at 2.7 gigatonnes per year in 2050

- Increase in emissions attributable to growing steel demand from emerging economies

- Over time, gradual shift in demand is expected from China to India, Southeast Asia and Africa

- The International Energy Agency (IEA) has developed several possible pathways for the steel industry:

- In the 90% reduction by 2070 pathway, emissions would still need to drop by 50% by 2050

- In the net-zero emissions by 2050 pathway, emissions would already need to drop by 25% by 2030, and drop to close to zero by 2050

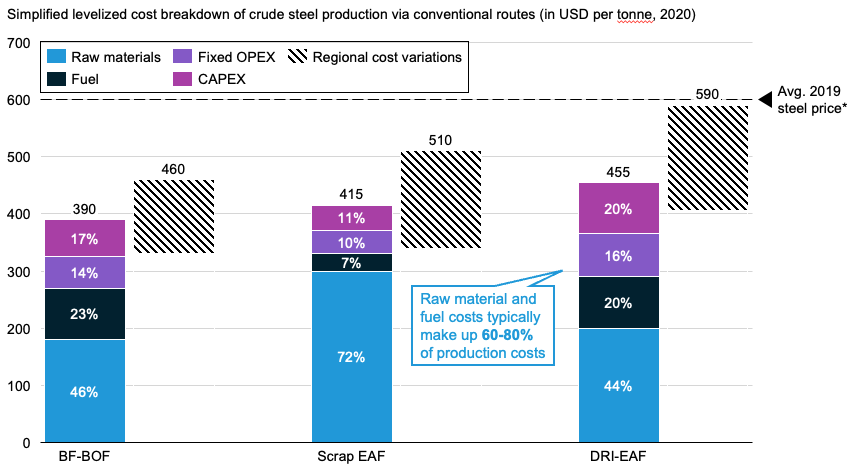

BF-BOF is the cheapest production method, but regional cost differences impact margins across production methods

Regional cost differences cause all steel making methods to be competitive

(*) Average steel price based on Hot Rolled Coil Steel Futures Continuous Contract (HRN00), average of 2019 monthly prices. Source: MarketWatch (2019) McKinsey,IEA Iron and Steel Technology Roadmap (2020), European Commission Joint Research Centre Science for Policy Report (2016). Credit: Mimi Khawsam-ang, Max de Boer, Grace Frascati & Gernot Wagner (22 February 2024);

share/adapt with attribution. Contact: [email protected]

Observations

- Profit margins across the industry are slim – the average EBITDA margin of steel producers over the past 10 years was 8-10%

- Raw material and fuel prices can cause strong fluctuations in margins, given that these typically make up between 60-80% of total production costs

- While some of these markets are global (iron ore), others are more regional (e.g. electricity, scrap steel) which can drive regional cost differences

- Labor costs, feeding into fixed OPEX, are typically higher in advanced economies than in emerging economies

- CAPEX for production equipment is usually consistent across regions. However, engineering, procurement and construction costs can vary significantly

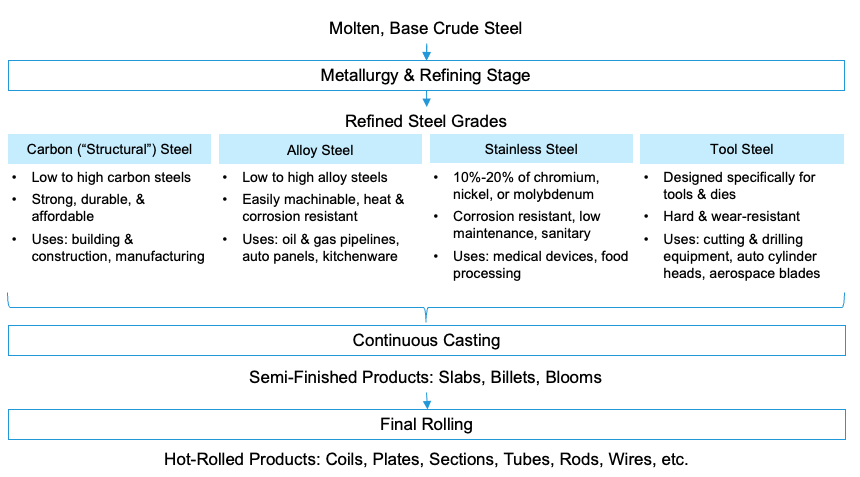

Downstream activities post-crude steelmaking use process heat and represent <20% of total steel production emissions

Downstream steelmaking process

Source: World Steel Association, Association for Iron & Steel Technology, Eziil, Industrial Metal Supply, Steel Manufacturer’s Association Steelmaking Emissions Report (2022).

Credit: Mimi Khawsam-ang, Max de Boer, Grace Frascati & Gernot Wagner (22 February 2024); share/adapt with attribution. Contact: [email protected]

Observations

- On average, <20% of steelmaking CO2 emissions come from downstream processes

- Metallurgy involves adding alloys in hot ladle to convert base crude steel into different types of refined steel (carbon, alloy, stainless, or tool)

- Common alloys: manganese, chromium, cobalt, nickel, tungsten, molybdenum, vanadium

- Refining step traps and removes impurities through processes like stirring molten steel with gas like argon

- Continuous casting molds liquid steel into semi-finished products, usually slabs, billets, or blooms

- Finally, the steel goes through a number of different finishing processes (e.g. hot or cold rolling, galvanizing) depending on the intended end use of the steel

Steel 100% recyclable material; increased use of scrap in primary and secondary routes expected to help decarbonize sector

Source: World Steel Association (2020), World Steel Association Scrap use in the steel industry (2021), World Steel Association Fact sheet: Raw materials in the steel industry (2023), Net Zero Steel

(2021), Mission Possible Partnership Net Zero Steel Sector Transition Strategy (2021), IEEFA (2021), World Economic Forum (2023).

Credit: Mimi Khawsam-ang, Max de Boer, Grace Frascati & Gernot Wagner (22 February 2024); share/adapt with attribution. Contact: [email protected]

Observations

- Steel is 100% recyclable and can be infinitely reused. Its magnetic properties allow easy separation from waste streams

- Scrap EAF lowest-CO2 is the least emitting and least energy intensive conventional route and is also cost competitive

- As a share of steelmaking, Scrap EAF expected to grow from 22% today to almost 50% by 2050 in Net Zero scenario

- Use of scrap as additional metallic inputs in conventional BF-BOF and DRI-EAF possible and proven: EAFs can use up to 100% of steel scrap, and BOFs up to 30%

- Scrap separated into two categories: pre-consumer scrap (scrap from downstream steel manufacturing) and post-consumer scrap (~50/50 split)

- As a share of steelmaking, Scrap EAF expected to grow from 22% today to almost 50% by 2050 in Net Zero scenario

- Over 85% of steel is recycled today, world’s most recycled material. Scrap steel supply only grows as steel products become obsolete

- The scrap steel market is already well-functioning, and expectations are that as scrap becomes more expensive there will be more incentives to recover steel from difficult applications such as foundations

Among major steel producing countries and regions, Asian economies lag in scrap steel consumption

Scrap steel consumption varies regionally but lags places like India and China

_0.png)

Source: Bureau of International Recycling World Steel Recycling in Figures 2017-2021 (2021), IEA Iron and Steel Technology Roadmap (2020), World Steel Association Scrap use in the steel

industry (2021), World Steel Association World Steel in Figures 2023 (2023), IEEFA New From Old: The Global Potential for More Scrap Steel Recycling (2021).

Credit: Mimi Khawsam-ang, Max de Boer, Grace Frascati & Gernot Wagner (22 February 2024); share/adapt with attribution. Contact: [email protected]

Observations

- Average lifespan of a steel product is ~40 years, but with a wide range. Steel packaging (such as tin-coated steel cans) lasts only a few weeks on average, while steel used for buildings may last 100 or more years

- This long life-span means that scrap steel is still scarce in emerging economies, as these countries industrialized later

- Usually, local scrap steel recycling markets feed the domestic steel industry. But there is some international trade taking place:

- Turkey, the world’s 7th largest steel producer, imported over 90% of their scrap steel inputs

- The EU and the US are both large exporters of scrap steel

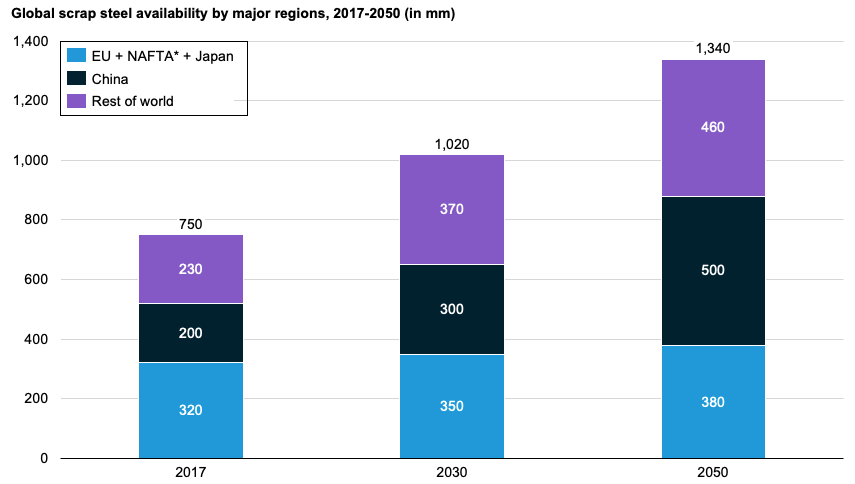

Scrap steel stock is expected to continue growing globally, allowing for more markets to increase scrap steel recycling

(*) Canada, Mexico and USA. Source: World Steel Association (2018), World Steel Association Scrap use in the steel industry (2021), IEEFA New From Old: The Global Potential for More Scrap

Steel Recycling (2021). Credit: Mimi Khawsam-ang, Max de Boer, Grace Frascati & Gernot Wagner (22 February 2024); share/adapt with attribution. Contact: [email protected]

Observations

- Domestic scrap availability to increase significantly in emerging economies over the coming years

- As China matures, it is expected to fuel much of global scrap steel supply through 2050

- Today, steel stock in OECD nations has reached 12-13 tonnes per capita, while in India and Africa this is only 1 tonne per capita – meaning less scrap steel is likely to become available in India and Africa over time

- As scrap availability improves, adoption of Scrap EAF and a growing share of scrap steal in total steel production become more feasible

| BAU | Business as usual | H2O | Water |

| BF-BOF | Blast Furnace-Basic Oxygen Furnace | IEA | International Energy Agency |

| CAPEX | Capital expenditure(s) | HRC | Hot Rolled Coil (type of finished steel product) |

| CCUS | Carbon capture, utilization & storage | MPP | Mission Possible Partnership – industry decarbonization coalition |

| CO | Carbon monoxide | MOE | Molten oxide electrolysis |

| CO2 | Carbon dioxide | NG | Natural gas |

| CO2e | CO2 equivalent, using global warming potential as conversion factor | NAFTA | North American Free-Trade Agreement |

| DAC | Direct Air Capture | NG | Natural gas |

| DRI-EAF | Direct Reduced Iron-Electric Arc Furnace production process | NG DRI-EAF | DRI-EAF production process using natural gas |

| EAF | Electric Arc Furnace | NZE | Net Zero Emissions |

| EBITDA | Earnings before interest, taxes, depreciation, and amortization | O2 | Oxygen |

| EW-EAF | Electrowinning-Electric Arc Furnace | OECD | The Organization for Economic Cooperation and Development |

| Gt | Gigatonne, equal to 1 billion metric tonnes | OPEX | Operational expenditure(s) |

| H2 | Hydrogen | SR-BOF | Smelting Reduction-Basic Oxygen Furnace |