In 1999, the euro was introduced to promote financial integration in Europe by sharing risks and pooling markets across borders. It seemed to be working, with more investors in the union buying assets in other countries. When the European sovereign debt crisis hit in the early 2010s, however, and countries like Greece and Italy faced the possibility of default, it sparked an interest in reassessing how integrated the union really was.

The need to understand ownership and risk regarding Europe’s sovereign debt led to the development of Securities Holding Statistics (SHS), which required every Euro Area country to report detailed data on its stock and bond ownership. Complete transparency, however, proved impossible because of the large portion of assets flowing through financial intermediaries domiciled in Ireland, Luxembourg, and the Netherlands, countries the researchers labeled onshore offshore financial centers (OOFCs).

Collaborating with the European Central Bank, Jesse Schreger, associate professor of business in the Economics Division at Columbia Business School, endeavored to trace the flow of capital in OOFCs and gain deeper insights into Euro Area financial integration. Schreger explains, “We wanted to use the full administrative statistics of the Euro Area to hopefully provide a real answer to the question of where capital is allocated and to figure out the core questions of European integration: Who bears the risks, how integrated is Europe, and where is money going?”

How the research was done: Although useful as a starting point, the SHS is reported on a residency basis, where the location of an investment or investor is their legal jurisdiction. When OOFCs are involved, this clouds the ultimate ownership. To unwind the flow of securities through OOFCs to the actual domiciles of the security issuer and ultimate buyer, Schreger and his co-researchers examined massive amounts of commercial data on cross-border investments.

What the researchers found: When it comes to money flowing through OOFCs, roughly half came from European investors, with the rest coming from investors from outside the Euro Area. Likewise, while a large portion of assets flowed back into the Euro Area, non-Euro Area investors tended to use OOFCs to invest in securities outside the Euro Area.

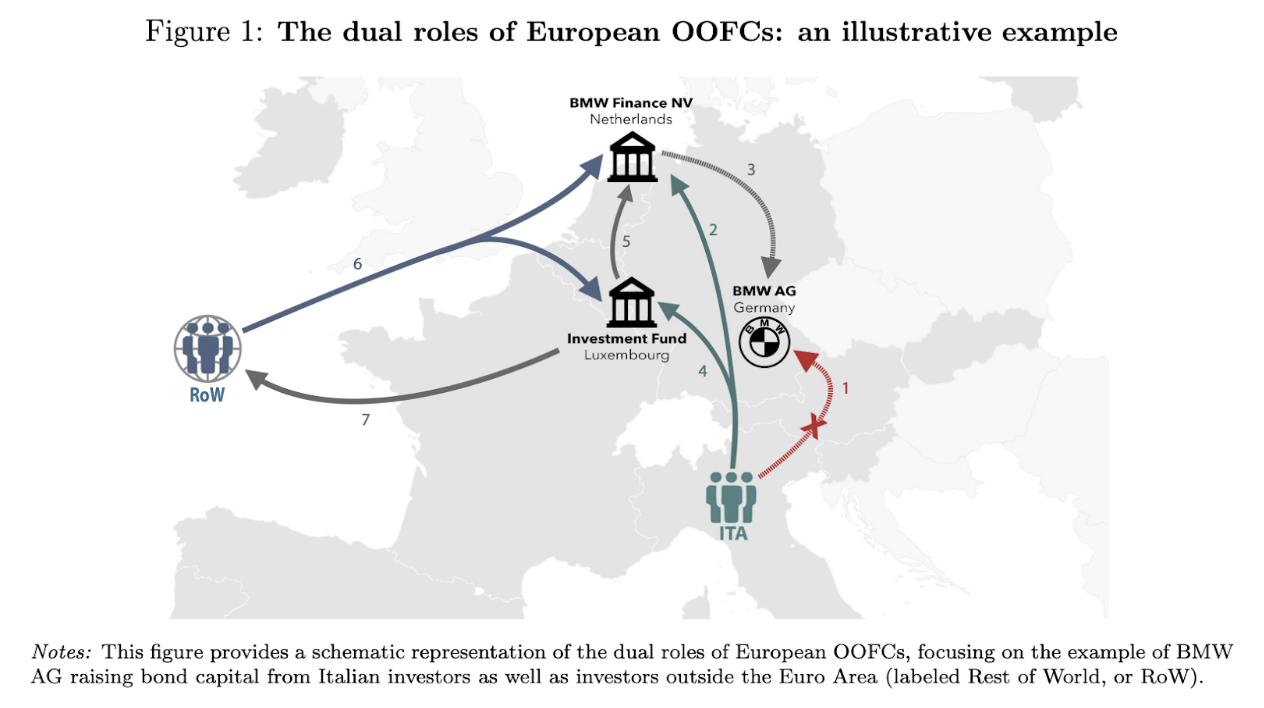

Additionally, while international investment statistics recorded high levels of cross-border investment, researchers found many were double-counted. The diagram below illustrates investment euros from Italy to BMW in Germany. Italian investors purchase these securities from the finance arm of BMW in the Netherlands (arrow 2) or from an OOFC fund in Luxembourg (arrows 4 to 5). Funds ultimately make their way to Germany (arrow 3). While the SHS might count arrows 2 through 5 as separate investments, researchers consolidate them into a single investment (arrow 1) from Italy to Germany.

The study’s new estimates demonstrate that, thanks to the role of OOFCs as hubs of financial intermediation and as places of securities issuance, the Euro Area is less financially integrated than it appears, both within the currency union and vis-à-vis the rest of the world. In the same vein, researchers found that official data overstate a decline in equity home bias, or investors' preference to invest in domestic assets rather than foreign ones. After the introduction of the euro, bond home bias indeed decreased significantly, but the decline in home bias for equity portfolios is exaggerated by the role of OOFCs and is otherwise consistent with other developed countries.

Finally, Schreger examined the issue of €3.2 trillion in so-called missing wealth. “If you look at the world's foreign assets and foreign liabilities as a whole, they should always sum to zero,” Schreger explains. “If I’m the United States and you’re Italy and I buy some of your stocks, I've acquired an asset. Your liability is exactly the assets that I own. The sum of global assets and liabilities have to offset exactly.”

When assets and liabilities don’t balance out, money is deemed missing. For the missing €3.2 trillion flowing through Luxembourg and Ireland, this study demonstrates that the UK plays a key role in holding and investing these funds, surpassing Switzerland in custodial wealth. In fact, the researchers document that most of the missing money is accounted for by UK counterparts.

Why it matters: The study’s results clarify how well the Euro Area is meeting its goal of financial integration. Before now, the extent to which investments flow through OOFCs has kept policymakers from accurately assessing risk exposures within the Euro area. In crises, it has been difficult to establish which countries and sectors will suffer losses — an important issue, given the variance of credit risks among Euro Area countries.

Furthermore, the methodology used in the study can be scaled to investigate the flow of capital globally, particularly when it comes to data on stocks and bonds. Schreger notes, “We can bring to bear massive amounts of commercial data to do this not just for one country or company but for the universe of companies and the universe of securities issued around the world.”

Adapted from "The Geography of Capital Allocation in the Euro Area" by Roland Beck and Martin Schmitz of the European Central Bank; Antonio Coppola, Angus Lewis, and Matteo Maggiori of Stanford University; and Jesse Schreger of Columbia Business School.