Kairong Xiao, the Roger F. Murray Associate Professor of Business at CBS, grew up in China with only a broad-strokes view of the American financial system — he always assumed it was a purely free-market paradigm. But when he moved stateside and experienced the landscape firsthand, he realized the nuts and bolts were much more nuanced.

“I was shocked to see how complicated financial regulation is,” he recalls. This realization sparked a fascination with the intricate dance between government and markets. “It’s a very interesting intellectual exercise to understand how to design those rules so that the free market can operate without harming people.”

Since 2008, that dance has gotten a lot more complicated. In the aftermath of the financial crisis, regulators scrambled to implement new rules to prevent history from repeating itself, and the sweeping reforms they introduced have reshaped the banking industry.

Xiao’s latest study — co-authored with Suresh Sundaresan, the Robert W. Lear Professor of Finance and Economics in the Finance Division at CBS, and published in the Journal of Financial Economics — dives deep into one of the most significant post-crisis reforms: liquidity regulation. The findings paint a picture of how these new rules are affecting the banking sector, often in unanticipated ways.

Liquidity Regulation to the Rescue?

Before 2008, bank regulation focused heavily on capital requirements, essentially ensuring banks had enough financial cushion to absorb losses. “The idea behind this type of regulation was that if banks had enough equity, capital, and skin in the game, they would behave prudently,” says Xiao.

But the crisis exposed a critical blind spot: Banks with seemingly sufficient capital on paper could still run into severe liquidity problems. “During the financial crisis, many banks seemed to have adequate capital, but when depositors went to withdraw deposits, they found out the bank didn’t have enough liquidity,” he explains. “The balance sheet seemed sound in the long term, but in the short term, they didn’t have the funds.”

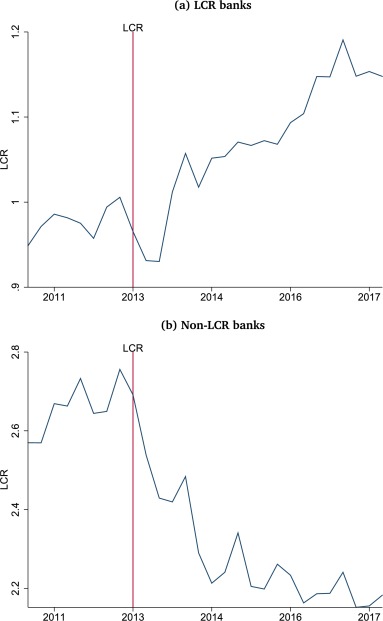

This realization led to a major shift in regulatory thinking. In addition to capital requirements, banks would now face liquidity requirements, designed to ensure they could meet short-term obligations even in times of stress. This paradigm shift led to the creation of the liquidity coverage ratio (LCR), a regulatory measure applicable to banks with more than $50 billion in total assets.

The LCR, Explained

At its core, the LCR requires big banks to hold highly liquid assets (like cash and government bonds) proportional to their potential short-term cash outflows. The idea is simple: For every promise a bank makes to short-term creditors, it needs to set aside some easily accessible funds. “This is intended to ensure banks don’t overpromise,” notes Xiao.

But the reality of implementing this seemingly straightforward concept has led to complex and sometimes unexpected consequences. To understand the LCR’s impact, the researchers employed both empirical analysis — examining bank balance sheets, lending patterns, and liquidity ratios before and after the LCR’s implementation — and theoretical modeling. Since the study coincided with the regulation’s initial rollout, it allowed the researchers to observe, in real time, how the banking system adapted to the new rules.

Results: The Good, the Bad, and the Unexpected

The first key finding was that while regulation achieved its intended purpose — reducing liquidity risks for large banks — it had the unintended consequence of crowding out lending at the big banks subject to the LCR. “If my balance sheet is $100, and I’m being forced by regulation to hold $50 of government bonds, the most I can lend to households or firms is $50,” explains Xiao. “So, to the extent that people care about banks’ ability to facilitate growth, that’s concerning.”

Another, more surprising finding was that as large banks became more constrained, smaller banks not subject to the LCR began taking on more liquidity risk. “We found that the illiquidity and ‘overpromising’ problem doesn’t disappear; it just shifts to smaller institutions,” says Xiao, adding that the combined impact of thousands of community banks taking on this risk can be significant for overall financial stability. “They may be small individually, but collectively, they’re a considerable part of the economy.”

Additionally, the research suggests that the current regulatory design can exacerbate market swings during crises. As demand for safe assets spikes, their yields plummet, making it even more costly for banks to comply with the LCR precisely when they need the most flexibility. “It’s effectively a tax on these bigger banks, because liquid assets have a low return,” says Xiao. “This cost is procyclical because when a crisis looms, it’s crucial for banks to build stronger liquidity buffers — yet that’s precisely when the current rule becomes most costly.”

An Ongoing Tango: Regulation and the Future of Finance

As recent bank failures demonstrate, the quest for financial stability is far from over. Xiao sees rich ground for future research, particularly in exploring how liquidity and capital regulations interact.

While the study’s primary audience is policymakers and bankers, its implications extend far wider. For entrepreneurs, small businesses, and the general public, the migration of lending activity to smaller banks could change where and how companies access credit. “There are implications for the cost of getting services from banks, like taking out a mortgage or a personal loan,” says Xiao. “Some banks will not be willing to take up certain loans just because they have a big liquidity penalty on their balance sheet.”

One possible solution? Xiao and Sundaresan propose that central banks offer a committed liquidity facility. This would allow banks to pay a fixed fee for guaranteed access to liquidity during crises. This approach could preserve the benefits of liquidity regulation while mitigating its unintended consequences.

Ultimately, the challenge lies in striking a balance between regulation and market efficiency — a delicate dance of promoting stability without stifling growth. “How do we design the regulations so that they’re not overly burdensome for banks and, at the same time, maintain the stability of the financial system?” says Xiao. “It’s a very important question.”

Adapted from “Liquidity Regulation and Banks: Theory and Evidence” by Suresh M. Sundaresan, the Robert W. Lear Professor of Finance and Economics in the Finance Division at CBS, and Kairong Xiao, the Roger F. Murray Associate Professor of Business in the Finance Division at CBS.