More than a third of Americans rent their homes, and many of them operate paycheck to paycheck and with tight margins. It’s discouraging but not surprising that one in 10 renters is behind in rent at any given point in time.

Boaz Abramson, assistant professor in the Finance Division at Columbia Business School, hopes his work can help change things for the better.

“More than 50 percent of renters in the United States are rent-burdened, meaning they pay more than 30 percent of their income on rent. About 30 percent are severely rent-burdened,” Abramson says. “These numbers speak for themselves and motivate research that seeks solutions.”

Health and income shocks, like unexpected medical expenses or losing a job, can lead tenants to miss rent payments they intended to make, with far-reaching consequences. Landlords lose income needed to cover mortgages, property taxes, and maintenance costs. Renters may damage their credit score and, in the worst case, face eviction. And if renters become homeless, they may increase the demands on taxpayer-funded social services.

Given the magnitude of the housing security problem in the United States, the need to find potential fixes is urgent. Together with Stijn Van Nieuwerburgh, the Earle W. Kazis and Benjamin Schore Professor of Real Estate in the Finance Division of Columbia Business School, Abramson decided to research whether rent guarantee insurance (RGI) programs, either public or private, might improve the situation for all parties. Much as auto insurance provides coverage in the event of an accident, RGI covers rent in the event a tenant falls behind on their monthly payment. Though relatively unknown to the public, RGI is a new and emerging insurance product currently being offered by several innovative fintech startups.

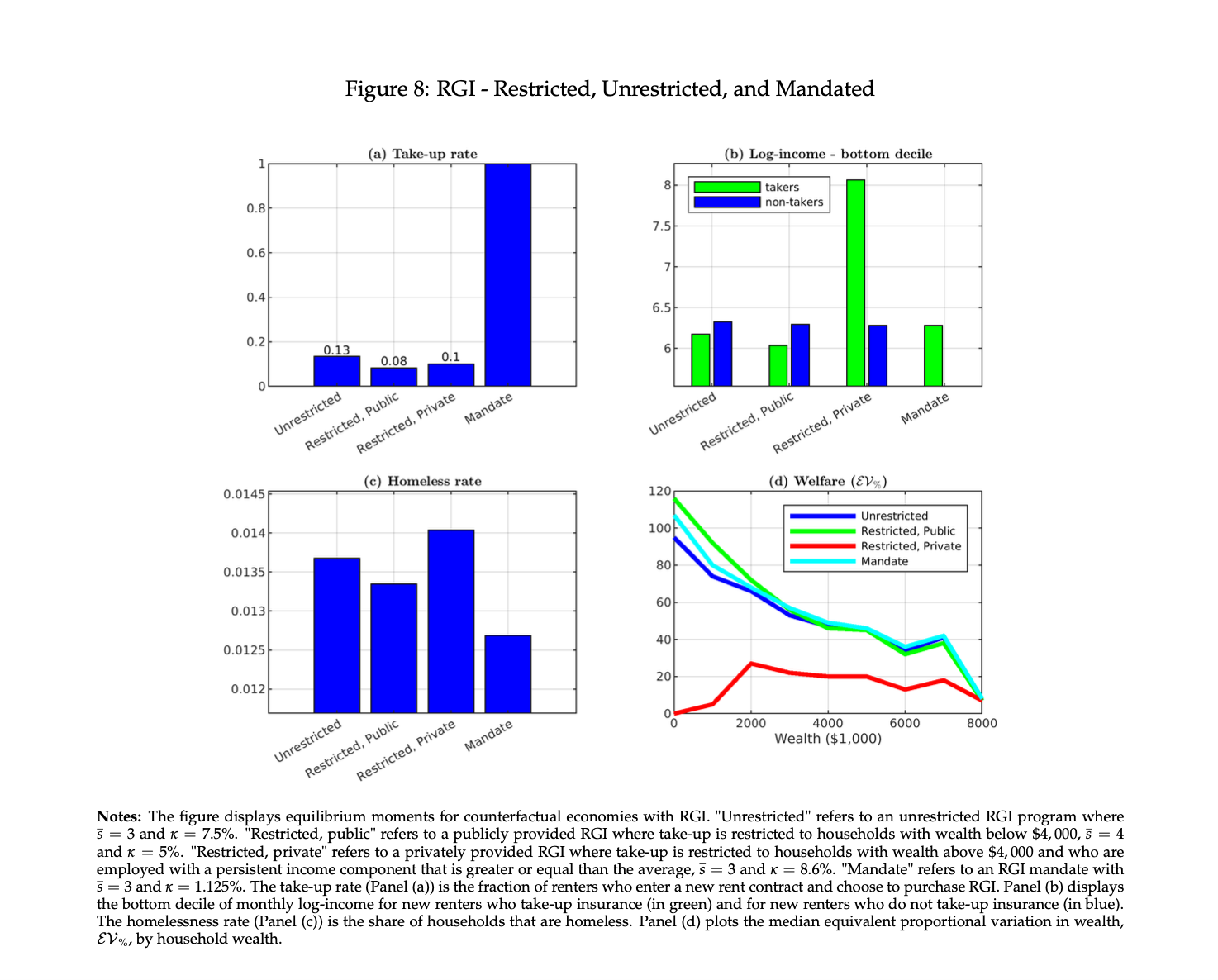

How the research was done: The authors developed a dynamic equilibrium mode and calibrated it to the US housing market. The model captures key features of the data, such as the heavy rent burden of tenants, their modest wealth accumulation, the incidence of nonpayment of rent and eviction, the prevalence of homelessness, the distribution of rents and security deposits, and the income and health risk that drive tenants to default on rent.

Using this model, the authors studied the effects of RGI, considering two potential providers of such insurance: private insurers and a public insurance agency. For each, the authors evaluated various RGI programs, specifically unrestricted RGI (where takeup is available to anyone who wants it), restricted RGI (where takeup is restricted to subsets of households), and an RGI mandate (which requires all tenants to take up the insurance).

The researchers analyzed the impact of these RGI products on housing security and assessed the financial viability of both private and public options. The main difference between the private and the public insurer is that the public insurance agency operates from government funds and must be considered in light of total government expenditure, not the insurance provider’s simple profit and loss. Because it reduces evictions, a public-insurer RGI program can lead to substantial governmental savings on homelessness expenses by keeping people housed. For the private insurer, the only source of revenue is the insurance premiums collected from insured renters.

What the researchers found: A public RGI system could offer significant individual and societal benefits, while a private insurance system’s benefits would be limited.

A private insurer would find it difficult to break even if it made rental insurance unrestricted, because the applicant pool would skew heavily toward people most likely to make a claim. For this reason, private insurers screen, or restrict, takeup to middle-income households that face less delinquency risk. Subsequently, private RGI has a limited impact on housing insecurity. “Ultimately, it’s a thin product offered to a particular crowd,” Abramson concludes.

On the other hand, a public insurer has a different bottom line: The relatively low costs incurred by preventing rent defaults might help avert more significant public expenses, like homeless services. “New York City currently spends $50,000 per year per person in the homeless system,” Abramson says. “Expenses like these are the main reason insuring households can be cost effective for a public insurer.”

In places with strong tenant protections, RGI may prove especially valuable. “If eviction protections are very strong, or if security deposit caps are in place, landlords might not be willing to rent to tenants in the first place if they have less-than-perfect credit,” Abramson says. “It turns out these tenant protections make RGI substantially more effective, since RGI mitigates a lot of the unintended consequences associated with these policies.”

Why the research matters: Housing insecurity is widespread and costly for society. “More than 3.5 million eviction cases are filed against renters in the United States every year, and more than 650,000 people are homeless on any given night,” Abramson says. “Our work shows that by providing rent guarantee insurance, the government can reduce rent delinquencies, homelessness, and evictions — and, at the same time, lower the fiscal costs of housing insecurity.”

It just might be a legislator’s dream: a policy that improves people’s lives while paying for itself.

Adapted from “Rent Guarantee Insurance” by Boaz Abramson of Columbia Business School and Stijn Van Nieuwerburgh of Columbia Business School.