Adapted from “Aggregate Lapsation Risk,” by Ralph S.J. Koijen of the University of Chicago’s Booth School of Business, Hae Kang Lee of the University of South Carolina’s Darla Moore School of Business, and Stijn Van Nieuwerburgh of Columbia Business School.

Life insurance lapsation rates are cyclical, moving with the business cycle.

Recent research by CBS Professor Stijn Van Nieuwerburgh and his co-authors has found that found poorer, less healthy households lapse at a higher rate during recessions than wealthier, healthier households.

Why the research was done: Life insurance is an important financial risk mitigation tool for households. It’s also a prevalent one: In the United States, about 67 percent of men and 62 percent of women between 35 and 44 own life insurance policies. Despite the important financial protection it provides for households, “we noticed that many people lapse in their policies after many years of paying their premiums,” says co-author Stijn Van Nieuwerburgh. “This intrigued us. Who lapses? Why do so many people lapse? When do they lapse? That’s why we set out to explore this.”

Van Nieuwerburgh, the Earle W. Kazis and Benjamin Schore Professor of Real Estate in the Finance Division at Columbia Business School, had previously researched the extent to which households optimally invest in financial products like life insurance and how life insurance companies may be incentivized to subsidize the treatment of life-threatening diseases.

How it was done: The researchers executed three lines of inquiry in this study:

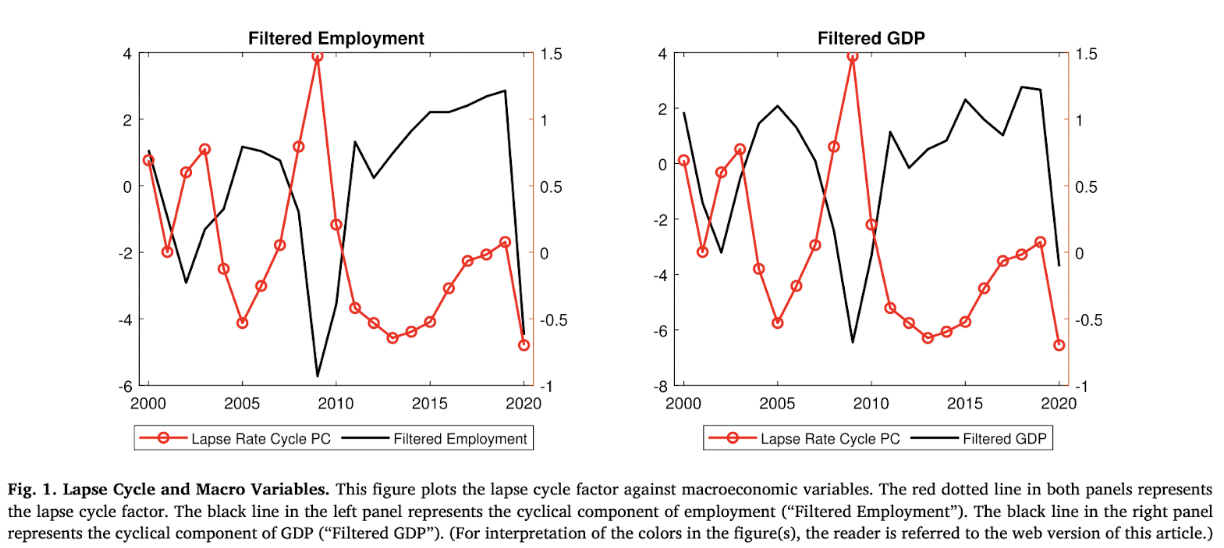

- They looked at lapsation rates over the business cycle using aggregate data from major life insurers’ regulatory filings from 1997 to 2020. They paired this data with GDP and employment data for each year in that time period to show the relationship between macroeconomic trends and lapsation rates.

- The researchers looked at individual policyholder-level data, which they obtained from one major US life insurer. They broke the data into groups of policyholders by socioeconomic markers and health levels to compare lapsation rates among groups.

- The researchers asked, “What does this lapsation behavior mean for the pricing of these policies? Does the fact that lapsation is cyclical affect price?” For this line of questioning, the researchers looked at pricing of policies against groups, how lapsation rates did or did not affect premiums, and profit implications for life insurers.

What the researcher found: The first line of analysis confirms previous studies that showed lapsation rates are cyclical and move with the business cycle, with policyholders lapsing more frequently during hard economic times. However, the analysis showed that lapsation rates behaved differently during the 2020 recession than in other recessions, reversing the general trend: Lapsation rates dramatically declined rather than increased. To explain that trend, Van Nieuwerburgh cites people’s increased awareness of their own mortality because of COVID and therefore a reluctance to let their policies lapse. Government stimulus checks also may have allowed people to continue paying for their policies.

The second part of the data analysis showed that lapsation behavior is tied to characteristics of policyholders. In particular, more economically vulnerable groups — lower income households, those in areas with more minorities, and people in poorer health –– are much more likely to let their policies lapse in bad times compared with healthier, richer people or people who live in areas with fewer minorities.

Last, the researchers found that life insurance companies do not seem to understand that the cyclical nature of lapsation rates affects different groups differently and therefore they do not factor the different effects among groups into the prices of policies. They found this results in a mispricing of policies, which in turn results in economically vulnerable groups overpaying relative to wealthier groups. If life insurance companies adjusted premiums down for vulnerable populations and adjusted premiums up for wealthier households, they could keep profits the same and protect vulnerable households from exposure to the business cycle.

Why it matters: The study’s findings suggest a need for life insurance companies to better understand the cyclical nature of lapsation and how that lapsation varies among groups and to adjust for it in their pricing strategies to protect vulnerable groups. The study also shows that protecting vulnerable groups is possible without sacrificing profit.

“We have redistribution in the life insurance market from poor people to rich people,” explains Van Nieuwerburgh, “which is wrong-way-around redistribution.”