Global carbon emissions from cement production have more than doubled since 2000, and they’re set to continue tracking their steady upward trend — unless cement-industry executives, entrepreneurs, and experts can agree on strategies to reduce them. Fortunately, that’s something many industry leaders are tackling now.

There’s a broad consensus, even outside the cement industry, that simply cutting back on production of cement — and its main derivative, concrete — is not an option. After all, demand for cement remains especially strong in developing countries where urbanization and infrastructure-building are on the rise. In many ways, the trend is a good thing: In both developing and more mature economies, GDP typically tracks linearly with the production of cement and concrete, according to a 2018 UN report.

“Cement utilization is a hallmark of development and maturity in a country,” according to Joseph King, a former program director at the US Department of Energy’s (DOE) Advanced Research Projects Agency ─ Energy. King and other experts visited the Columbia Business School campus recently to participate in a workshop discussion about possible routes for decarbonization in the sector.

The problem is that cement is a major carbon emitter. Collectively, manufacturing sectors account for roughly 30 percent of annual global CO2 emissions and cement is among the biggest polluters, second only to steel.

In discussions of how to decarbonize cement production, much of the focus typically is on the production of clinker, the primary binding agent in cement, and for good reason: Producing clinker accounts for 80 to 90 percent of cement manufacturing emissions. The clinker production process involves heating limestone at temperatures above 1,400 degrees Celsius, which is a massive energy expenditure in itself. But even if the energy used to heat the limestone were 100 percent clean, roughly 60 percent of the process’ current carbon emissions would continue unfettered, since the limestone calcination process is a chemical reaction that produces CO2 as a byproduct.

However, for all the complexity the cement decarbonization puzzle presents, there are early signs of positive change within the industry. One example is the effort to cut back on clinker by substituting a portion of it with supplementary cementitious materials (SCMs) to reduce emissions. Many SCMs come from so-called waste products, like fly ash from coal-fired power generation and blast-furnace slag from iron and steel production.

While these clinker replacements come with their own complications (society’s broader decarbonization will mean less fly ash byproduct, for example), they point to a creativity and resourcefulness within the cement industry — and a reason to be optimistic that decarbonizing could represent other means of unlocking value.

Learn more about Columbia Business School’s Climate Knowledge Initiative: Cement

“Not every industry can recycle demolition waste like we can and use it for raw materials,” noted workshop attendee Maher Al-Haffar, executive vice president of finance and administration at Cemex, one of the world’s largest cement companies. “There's a misconception that for any emitting industry, the cost of transition is value-destructive to shareholders. In our industry, we actually think it’s value-creating.”

But the economics and specific technologies and strategies required to achieve a cleaner future for cement remain murky, and of course, workshop participants didn’t agree on all details. They did, however, agree on one thing: Cement decarbonization is possible — and it’s beginning to happen. They said now is the time to accelerate this fledgling progress with hard-and-fast climate goals in mind.

Here are six key points experts shared at the cement decarbonization workshop:

Insight 1: Reducing emissions from the cement industry requires a “silver buckshot” — not a single silver bullet.

Read more about Columbia Business School’s Climate Knowledge Initiative

Numerous alternatives to the current modes of cement production have been proposed, and some solutions are already beginning to be implemented, including:

- Clinker substitution to reduce emissions, with materials like fly ash or blast-furnace slag

- Improved energy efficiency in cement manufacturing facilities

- Alternate fuels that are less energy-intensive than fossil fuels for heating kilns

Other alternatives and changes to the current process remain more nascent. These include:

- Alternate production methods, including alternate cement feedstocks or different electrochemical reactions that reduce emissions

- Alternative binder chemistries that lower both energy- and process-based emissions

- Carbon capture, utilization, and storage projects

Which alternate route is likely to win over the cement industry? Workshop participants said that’s the wrong question to ask.

“The idea that there’s one solution is a fallacy,” said Rick Bohan, senior vice president of sustainability at the Portland Cement Association. “It’s got to be all of the above.”

“Everyone is looking at a portfolio of solutions,” added Cemex’s Al-Haffar. “We have to have everything on the table; we don’t know how things will evolve.”

One important solution: lower the clinker-to-cement ratio to around 0.5. Eric Koehler, vice president of innovation, product, and quality at building materials company Titan America, explained how the current clinker-to-cement ratio already stands at well below 0.8, comparable to global averages. That’s because most SCM in the United States is added at the concrete batching plant rather than during cement manufacturing, as in most of the rest of the world.

Koehler added that these ratios could and should shrink further, to around 0.5: “The materials and technologies are known, and we expect further innovations to improve the ability of SCM to substitute clinker.”

However, Koehler said this goal ratio won’t be possible by simply relying on conventional SCM substitutes for clinker. To illustrate one of many alternatives, he explained that Titan America is building a first-of-its-kind calcined clay production line at its Troutville, Virginia, plant in the hopes of expanding the use of another type of SCM to reduce clinker — one that has been used at lab and limited industrial scale for decades but needs greater uptake.

As supplies of fly ash and slag dwindle, other companies are getting resourceful about digging up greater supplies of clinker substitutes. Ivan Diaz Loya, vice president of research and product development at Eco Material Technologies, explained that his company excavates fly ash from landfills and ash ponds for use as an SCM in cement.

Workshop attendees also discussed some of the more nascent approaches to overhauling cement production. Brimstone co-founder and CEO Cody Finke said his company eliminates the calcination process of traditional cement production altogether by using carbon-free calcium silicate rocks, which, he explained, comprise over 50 percent of the earth’s crust. This results in what’s known as ordinary Portland cement (OPC), the industry’s mainstay material, and creates SCMs in the same process. One hitch is cost: Because Brimstone's process is not yet at scale, it is not yet cheaper than standard cement production, Finke said — with an emphasis on not yet.

Stephen Galowitz, chief commercial officer at Sublime Systems, presented his company’s breakthrough: an electrochemical process that replaces carbon-intensive limestone with abundant non-carbonate feedstocks such as calcium silicate minerals or industrial waste. The company then uses electricity rather than heat to break down feedstocks to produce a calcium silica cement that displaces ordinary Portland cement.

While workshop participants agreed that an all-of-the-above mindset is what the industry needs to decarbonize cement production, the DOE’s King interjected that the current array of technologies and solutions also presents challenges: “The market right now lacks uniform standards to define low-carbon materials and to enable informed procurement.”

Insight 2: Moves toward decarbonization are happening fast within the cement industry, but there is a long way to go.

So-called alternative cement technologies have been around for decades and, in some cases, longer — as Portland Cement Association’s Bohan pointed out, the Paris Underground was built in the late 1800s using slag cement. But the consensus at the workshop was that in just the past few years, the uptake of alternative and lower-carbon materials in the cement and concrete industries has moved at an exponentially faster pace.

“Non-traditional blended cements are now the vast majority of cements produced in the United States,” said Bohan, noting that the term blended cements means cements that use clinker and fly ash or clinker and other SCMs as binders. “That happened in three years! The idea that people can’t change or that the industry won’t change is just wrong.”

Read more about Columbia Business School’s Climate Knowledge Initiative

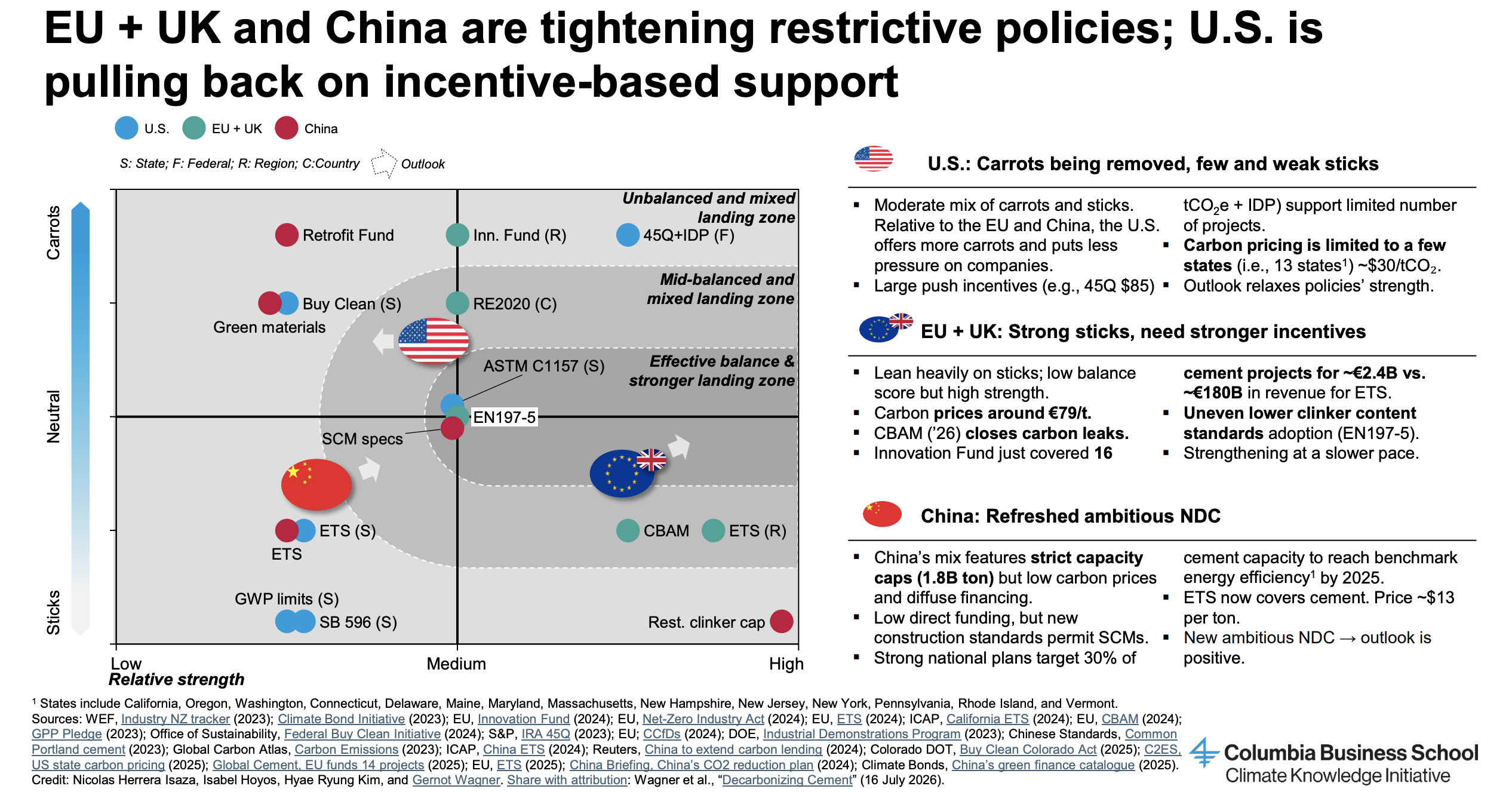

Al-Haffar of Cemex echoed that sentiment. He said over the past three years, Cemex has gone from having almost no low-carbon cement on offer to almost 65 percent low-carbon cement as of June 2024. “This isn’t happening because we’re pushing it,” Al-Haffar said. “It’s happening because it’s being demanded.” In Europe, he pointed out, companies are using SCMs and other decarbonizing means due to incentives from the region’s Emissions Trading System (ETS), which effectively puts a price on carbon.

He added that blended cements haven’t been nearly as prevalent in the US market: “We haven’t had to use them” because of a lack of price on carbon. “There’s more fear around them.” If an ETS were to be instituted in the United States — or in Mexico, China, or India, for that matter — massive industry change would likely happen overnight, Al-Haffar said.

Yet, while the recent uptake in new, lower-carbon materials is heartening, it’s not nearly enough, agreed workshop participants. The next few years will be key in taking even bigger, bolder action on new products and technologies.

“We’re in this critical period of many of these new technologies being tested, over the next five years or so,” said Paul Adeleke, director of strategy, communications, and policy at the Global Cement and Concrete Association (GCCA). “Not all of them can be winners; that is the nature of innovation. Where our own startup platform comes in, for example, is helping to effectively test in a real-world environment some of the more promising technologies with our members, to see if they really can play a role at scale—because that is what we need.”

Of course, a lot rides on the definition of “low carbon” cement. That calls for standardized metrics, ideally set by policy rather than voluntary action by the industry. Moreover, timing is essential, representing another area where policy ought to help push the necessary transformation.

Insight 3: The take-up of lower-carbon cement will require collaboration and adaptation from the construction industry and regulators.

To take bold action, disruptors in cement will need to confront “a tremendous amount of institutional inertia,” said Portland Cement Association’s Bohan. “There’s a reluctance that, OK, we haven’t worked with this material before, and if we don’t have experience with it, we’re going to default to what has been around for a hundred-odd years,” Bohan added.

King acknowledged that the cement sector typically has a 10- to 20-year adoption cycle for new blends and materials, due in part to a need to update standards and a slow customer adoption cycle. As such, King offered this solution: Mitigate liability to drive earlier adoption — for example by setting up the equivalent of a catastrophe fund for infrastructure projects.

However, both standards and builders’ attitudes will have to undergo some change, agreed workshop participants.

“Many of the practices of the construction industry have been established around the properties of Portland cement,” said Daniel Duque, director of Future Tech at Cementos Argos. “We all want to have the properties of Portland cement with low CO2, and that will be difficult to achieve. So, at some point, we have to find common ground and adapt to the properties of low-carbon cements.”

Diaz Loya of Eco Materials agreed: “SCMs require us to think about concrete a little differently. You have to be willing to make adjustments.”

Kim Kurtis, associate dean and a professor in the School of Civil and Environmental Engineering at Georgia Tech, and other workshop participants noted one trend among builders is to compensate for “alternative” cement perceived as riskier by simply adding more cement to concrete. This becomes a “vicious cycle,” Kurtis explained, where attempting to reduce emissions associated with concrete actually yields the opposite result.

To address this problem, she said education and data sharing, and even automation, need to be part of the solution so that builders understand that cements with a given SCM profile, for example, should be mixed in a specific way.

King agreed: “We need to establish shared standards and a data ecosystem for low-carbon products.”

Government regulations for cement and concrete will also need to be amended, several participants said. Al-Haffar noted that as blended cements become more popular in places like Germany, his company is running into this roadblock. “Right now, the regulations say that alternative cements can only be used for low-stress applications,” he said. “But our engineers believe they’re actually adequate for high-stress uses.”

He added, “As an industry, we’re moving from saying we will decarbonize to we are decarbonizing. But we need regulators to do their part or else this won’t work.”

Insight 4: Innovation will need to play a key role to lower costs, especially in developing countries.

“A higher-cost solution has no existing mechanism for scale,” argued Brimstone’s Finke. “To meet Paris [Agreement] goals and move fast, with an achievable level of spend, we need solutions that can be lower cost than conventional production — and we should not settle for higher-cost solutions.”

In Finke’s estimation, insisting on solutions that can eventually be lower cost than existing processes immediately rules out some cement decarbonization strategies that have recently attracted airtime. Among those are carbon capture, utilization, and storage, which, Finke said, “adds a process step but does not add any value” to the customer directly. He added that electrification alone cannot be the answer. Finke’s company focuses on ordinary Portland cement made from silicates, which has the potential to cut costs and carbon.

Read more about Columbia Business School’s Climate Knowledge Initiative

Such solutions may play an important role particularly in developing countries, which will be the biggest users of cement and concrete in the coming decades. The Asia-Pacific region currently accounts for 70 percent of global cement and concrete production and consumption, while Africa and other developing economies account for only 10 to 15 percent. That number is sure to rise both in relative and absolute terms, workshop participants noted. To achieve sector-wide decarbonization, it will be crucial to include strategies that address the needs of these regions.

Current costs of low-carbon technologies remain a significant hurdle, exacerbated by the higher cost of capital in many developing countries, they said. That means global cement decarbonization efforts will need to include solutions that have the potential to lower costs at scale.

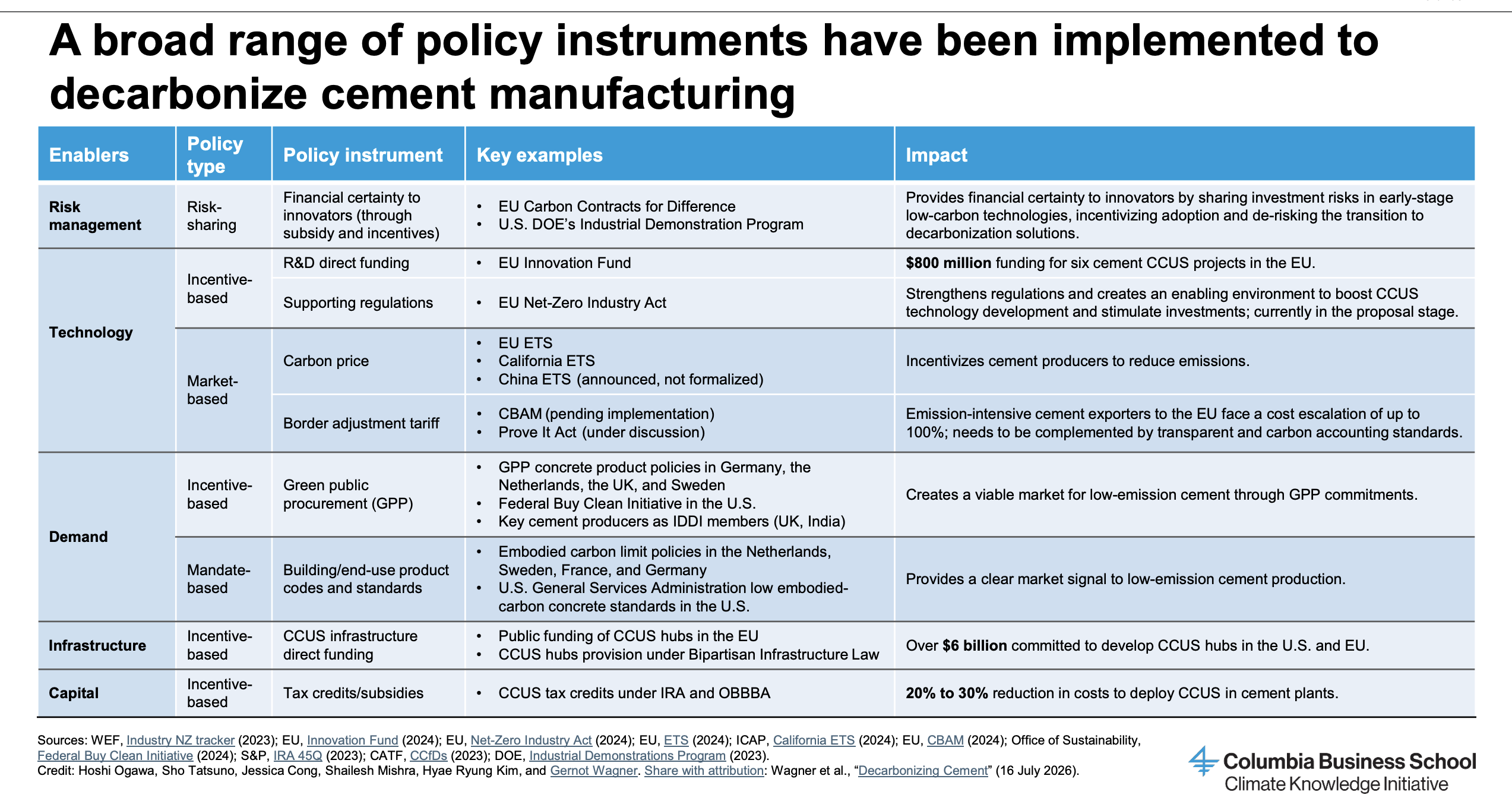

Insight 5: Financing innovation will also be needed to decarbonize the cement industry.

“This is not just about technological innovation; financing innovation has to happen as well,” said Sublime Systems’ Galowitz. “We have to be just as clever on the commercial side as on the technical side.”

Galowitz and others presented some financing innovations that they said could drive change in the cement industry:

- Production tax credits (PTCs), doled out for each ton of low-carbon cement produced. “PTCs have been proven to work,” Galowitz said, referring to the financing mechanism typically applied to renewable energy per kilowatt-hour. “There’s no reason PTCs couldn’t apply in this context,” he added, noting, “PTCs are powerful because businesses can build into predictability; that’s the way businesses have to operate.” Galowitz said PTCs could be applied on the federal or state level, though a streamlined, single federal system should be the goal.

- Book-and-claim systems for cement, which would decouple so-called green attributes like saved greenhouse gas emissions from the physical product (cement, in this case), tapping into carbon markets and other regulatory frameworks to finance low-carbon cement elsewhere. Adeleke of GCCA said his association’s members have expressed interest in such a system: “If we can get this up and running, it’s hard to see a more effective way of potentially delivering finance so quickly.”

- More plentiful funding opportunities for startups, according to Georgia Tech’s Kurtis. “The ‘valley of death’ is real in this industry; very few startups have successfully crossed it,” Kurtis said, referring to the challenging period for startups in which they’ve commenced operations but aren’t yet generating revenue. “How do startups have enough time to get a foothold in the marketplace when there’s so much technical and capital investment required to get there?” Not to mention, she added, the burden of the narrow, patchwork specifications for cement written by byzantine organizations. “Are we holding innovation back?” she asked.

Al-Haffar of Cemex and Duque of Cementos Argos both emphasized that their firms support startup innovation, in part with direct venture capital arms. King wondered whether an even better physical resource for some startups could be government facilitated, in the form of a leasable materials center of excellence that would enable startups to experiment without sacrificing their intellectual property. Galowitz agreed that, in some cases, the government is the best support of necessary disruption in an industry.

Insight 6: Government help is needed to scale novel, lower- and zero-carbon cements.

Galowitz highlighted some of the funding levers that fall squarely in the realm of government — for one, financing large-CapEx projects, which can require hundreds of millions of dollars. Governments can also create contracts for differences, meaning that when prices are below a certain price for a commodity, the government ensures a floor price. “This makes a product institutional grade for investment,” Galowitz explained.

Governments can also act as purchasers. Of particular value would be US Department of Transportation and Department of Defense procurement policies that favor low-carbon cements. These agencies can also partner on pilot projects. After all, Galowitz noted, 60 percent of cement is used in the public realm.

Cheng Qi, director of research and development at Ash Grove Cement, said working with the Army Corps of Engineers research center, the Federal Highway Administration lab, the US Bureau of Reclamation lab, environmental design consultants, and more recently, the MnROAD test track was crucial in getting some of his own company’s novel low-carbon binder solutions off the ground. Qi added that federal and state low-carbon procurement policies will be the pivotal enabler for Ash Grove Cement’s go-to-market strategy.

“Funding follows policy,” added Kurtis, noting that the current lack of uniformity in policies and regulations around alternative cements could be hindering innovation.

Bohan summed up that the scale of change necessary for the cement industry goes beyond the need for a “whole of government” approach: “While a whole-of-government approach is great, we also need a whole-of-society approach.”

Read more about Columbia Business School’s Climate Knowledge Initiative