Addressing Cement's Critical Challenge

Cement production accounts for 5-8% of global CO2e emissions, with emissions more than doubling since 2000. Over 80% of these emissions come from the calcination of limestone in clinker production, an emission-intensive process with no easy substitute. As demand for cement continues to grow, reducing its carbon footprint is a critical challenge.

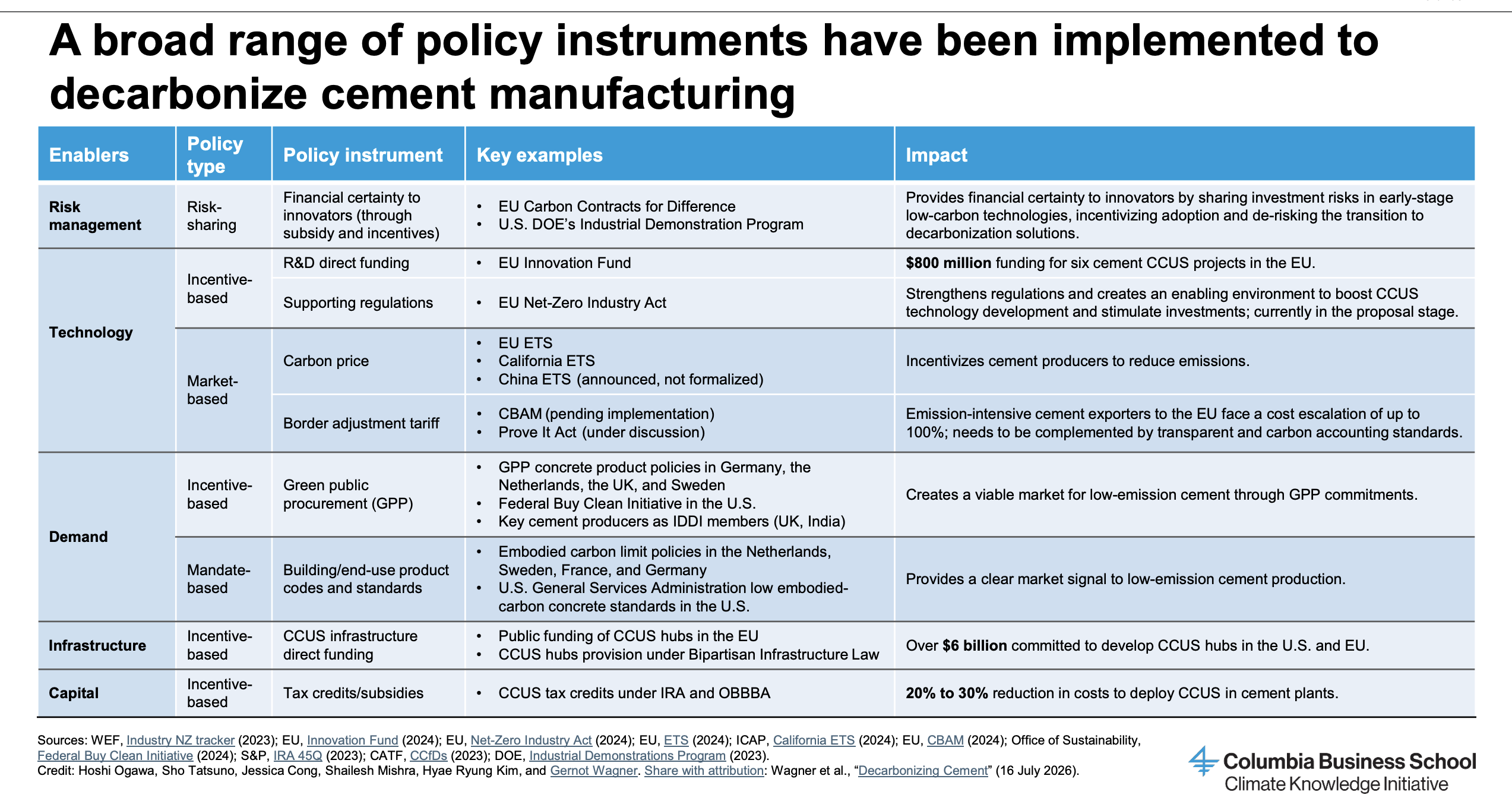

Key decarbonization strategies focus on reducing clinker use, developing alternative chemistries, and scaling carbon capture technologies. However, adoption remains slow due to cost, infrastructure constraints, and regulatory uncertainty. The key question is: How can the industry accelerate the transition while maintaining performance and affordability?

Download Decarbonizing Cement below to explore innovative technologies, market barriers, and policy levers to accelerate the adoption of these solutions.

Four Key Points

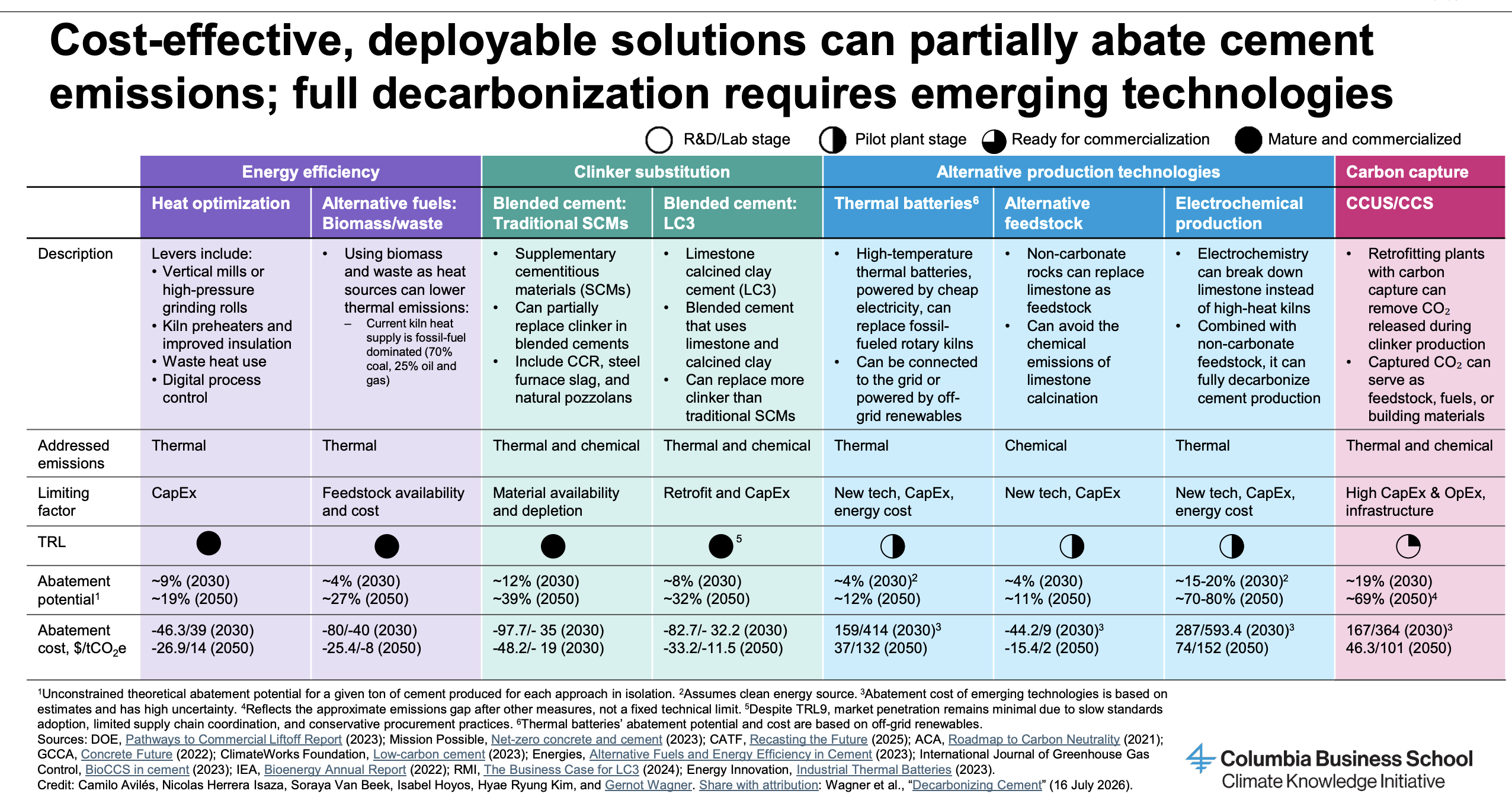

Reducing emissions from the cement industry requires an “all-of-the-above” approach — not the discovery of a single silver bullet. This will include currently deployable measures like clinker substitution, energy efficiency, and alternative fuels, as well as alternative production methods, nascent technologies, and carbon capture.

Moves toward decarbonization are already happening fast within the cement industry, but there is a long way to go. In just the past few years, the uptake of alternative and lower-carbon materials in the cement and concrete industries has moved at an exponentially faster pace.

The take-up of lower-carbon cement will require collaboration and adaptation from the construction industry and regulators. The cement sector typically has a ten-to-twenty-year adoption cycle for new blends and materials—due in part to a need to update standards, and in part to a slow customer-adoption cycle.

Innovation will need to play a key role in lowering costs, especially in developing countries. Current costs of low-carbon technologies remain a significant hurdle, exacerbated by the higher cost of capital in many developing countries.

Cementing Carbon: Constructing the Low-Carbon Future

To appreciate how fundamental a role cement plays in human society, one must first understand the importance of the carbon cycle in the evolution of the planet. Carbon dioxide (CO₂) in the atmosphere dissolves in seawater and gets metabolized by living corals and plankton that eventually die and decompose into ocean sediments. The sediments are compressed over millions of years until they become limestone – a natural storage vault for elemental carbon, like coal, oil and gas.

Brimstone: How one company uses different rocks to make the

Cement production is something we rarely think about, but it’s one of the largest contributors to climate change. As more cement is needed every year, is there anything we can do to stop this problem from building up? Caltech Ph.D. Cody Finke has a high-tech solution and he’s already attracting big name investors. @ColumbiaBusiness Professor and Climate Economist Gernot Wagner heads to Brimstone's laboratory to see what’s really going on.

Sublime: Cleaning up cement, one electron at a time

In a small warehouse just across from a local brewery, Leah Ellis and her team of young, ambitious scientists are working on something incredible. They’re making a new kind of cement to solve one of the industry's biggest problems: pollution. Cement production is a massive contributor to climate change. Climate Economist and @ColumbiaBusiness Professor Gernot Wagner heads to Sublime System’s laboratory to see what’s really going on.

Who Pays for Cutting Carbon Out of Making Cement?

Industry incumbents must decide when and how to use new production methods while the old one remain profitable. Explore the rest of the content below.

Decarbonizing Cement: Six Key Points from Industry Leaders

Global carbon emissions from cement production have more than doubled since 2000, and they’re set to continue tracking their steady upward trend — unless cement - industry executives, entrepreneurs, and experts can agree on strategies to reduce them. Fortunately, that’s something many industry leaders are tackling now.