Up until the past few years, the United States and other advanced economies enjoyed an unusually long period of low and stable inflation. But recent rising inflation has taken a heavy toll on households and businesses, making people’s day-to-day lives more difficult. Understandably, everyone wants to know where inflation is going next.

One popular view among economists is that inflation will eventually return and stay at lower central bank targets — around 2 percent in advanced economies, somewhat higher in emerging ones. A countervailing argument, however, holds that structural changes in the global economy will keep inflationary pressure high, making the job of central bankers much more challenging than in the past few decades. It’s a debate Columbia Business School’s Pierre Yared and fellow researchers consider in their new study, “Changing Central Bank Pressures and Inflation.”

“We were interested in trying to understand the forces that kept inflation low for the past three decades and look forward to see where inflation is likely going,” explains Yared, the MUTB Professor of International Business at CBS.

How the research was done: Yared and his fellow researchers created a new model to study the relationship between global economic factors and inflation. They started with the New Keynesian model, the most well-known framework for studying monetary policy, and modified it in two important ways: They allowed for the steady state of inflation to be greater than zero, and they recognized that central banks are not always committed to perfect monetary policy, instead having discretion to respond to political economy factors.

Under the new model, the researchers can predict how different economic factors manifest themselves in long-run inflation and evaluate the impact of phenomena such as deglobalization and supply chain disruptions. It also allows them to quantify how these different economic mechanisms affect inflation, in both the short and long term.

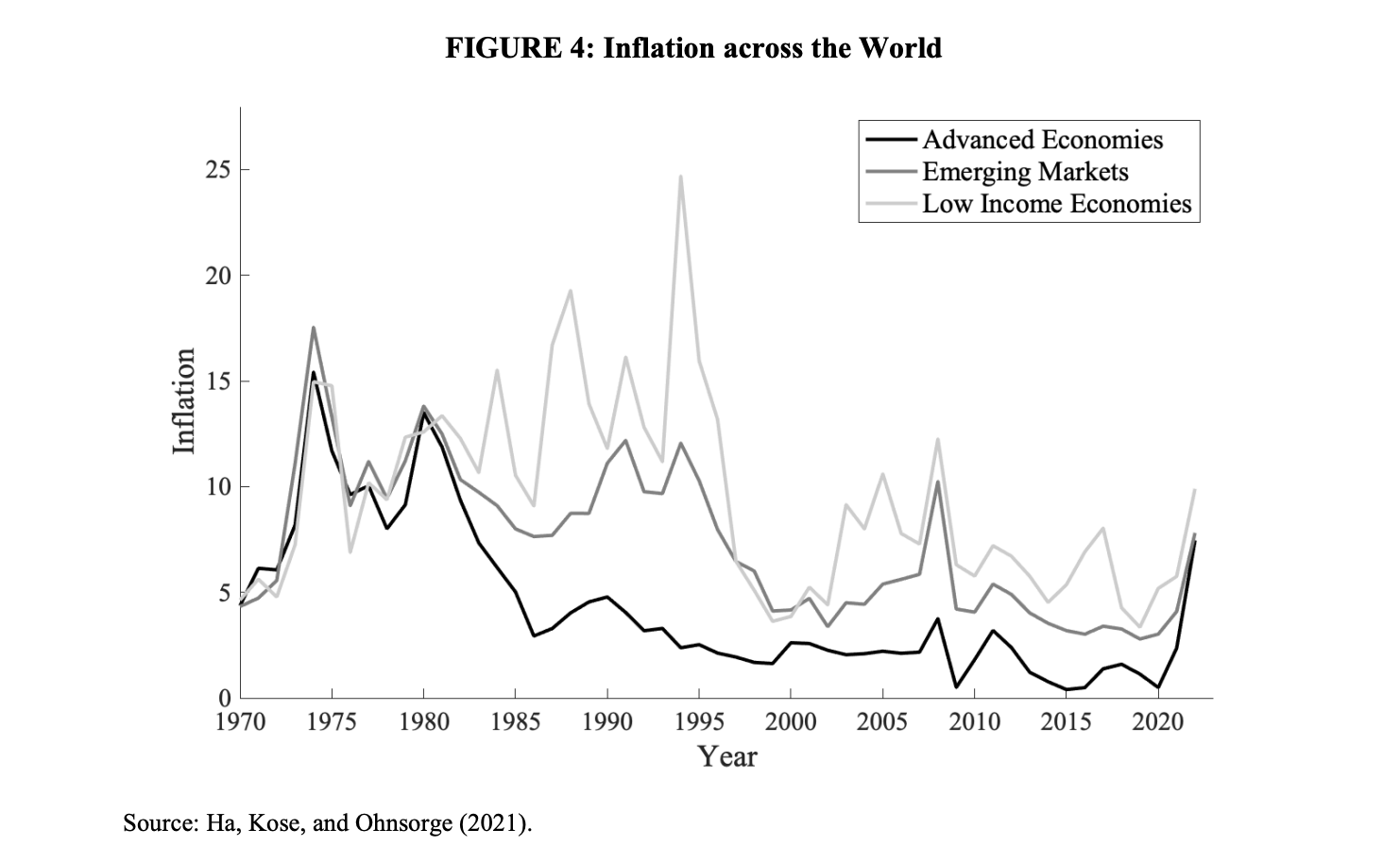

What the researchers found: Over the past few decades, the job of the central banks to keep inflation low was made easier over the last few decades by several factors:

- Globalization through the reduction and elimination of barriers to trade and foreign direct investment brought about more competition and lower prices.

- De-unionization reduced wage pressures in advanced economies.

- The public-debt-to-GDP ratio in emerging markets declined, reducing the incentive for central banks to accommodate fiscal policy with looser monetary policy.

Now, these global forces are reversing course. An international trend toward protectionism, partially fueled by tensions among world superpowers, has led to economic nationalism and the reshoring of production to home countries where costs may be higher. The COVID pandemic exposed weaknesses in critical supply chains that caused governments to double down on reshoring in the name of national security. At the same time, most advanced economies are experiencing expanding fiscal pressure for servicing national debt, spending more on industrial policy, and honoring increasingly expensive entitlement programs for aging populations.

The researchers argue that while inflation is likely to come down from its recent highs, it will remain higher on average in the long run from what were the abnormally low levels over the past three decades. Unfortunately, price hikes are likely to come in the form of sudden surges, like the one seen in 2022, rather than gradual increases. The model showed that inflation rates will tend to spike up in response to disruptive economic events, overcorrecting, before falling to a higher average level.

Why it matters: The researchers suggest that it’s time central banks begin to take a new set of factors into consideration in keeping inflation under control. “This is a warning to central banks that they can’t take their pre-COVID past successes for granted,” Yared says. “Their jobs are getting much harder. It will be globally much more difficult for all central banks to fight the forces pushing inflation upward.”

Adapted from: “Changing Central Bank Pressures and Inflation” by Hassan Afrouzi of Columbia University, Marina Halac of Yale University, Kenneth Rogoff of Harvard University, and Pierre Yared of Columbia Business School.