In the 1990s, more than 8,000 US companies traded on stock exchanges. Today, around 4,000 do. It’s a startling trend in a country where the value of the S&P 500 index is shorthand for economic prosperity.

A common scapegoat for this decline is the burden of governmental regulations. The costs of complying with these regulations, the theory goes, outweigh the benefits of going public. But data on the actual costs of regulation are hard to come by. Companies may exaggerate their costs as they lobby for less regulation.

Regulators, in turn, underestimate the burden of compliance by failing to account for less quantifiable costs, such as a company being forced to disclose information that could benefit a competitor.

To figure out whether the costs of regulation are actually leading to fewer companies going public, researchers and policymakers need more objective and comprehensive data.

That data is now available, thanks to an innovative approach from a pair of researchers in Columbia Business School’s Finance Division: Kairong Xiao, the Roger F. Murray Associate Professor of Business, and Michael Ewens, the David L. and Elsie M. Dodd Professor of Finance and co-director of the Private Equity Program.

Are Costly Regulations the Real Cause?

Rather than relying on companies’ claims of regulatory burdens, Xiao and Ewens used what they call the revealed preferences approach, looking at a firm’s actions as the truest measure of those costs.

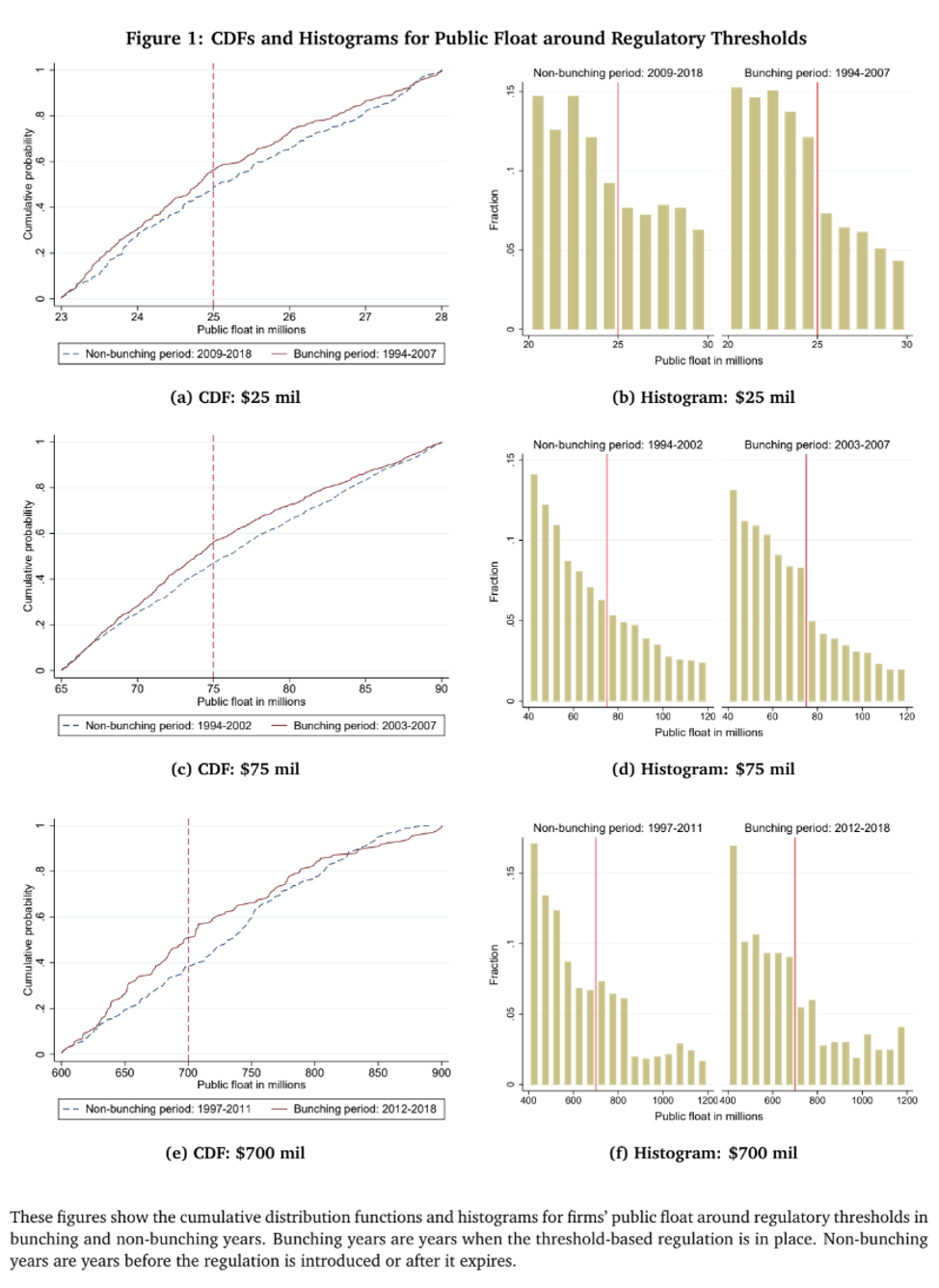

The research took advantage of the fact that certain regulations are triggered only when a firm’s public float — the portion of shares owned by public investors — exceeds a certain threshold. Xiao explains that the distinction between public and private firms is more nuanced than is commonly understood. “There's actually a gray area where, if your firm is under a certain threshold, you're kind of in between public and private,” he says. “You are exempted from a lot of the regulations that would impact the biggest public firms like Apple and Google.”

If companies find it’s too costly to cross a certain threshold — for example, if they have to disclose more information or hire external auditors — they will try to stay below it. “If that regulation triggered at the threshold is truly costly, you're going to see a lot of firms essentially manipulating their public float to stay below, predominantly through borrowing more and changing their debt-equity ratio,” Xiao says. But if the benefits of going public — for example, access to new capital markets and greater liquidity — outweigh those costs, they’ll cross it.

If a regulation is costly, the researchers theorize, a disproportionate number of companies will be “bunched” below the triggering threshold. The study examined three regulations with size-related exemptions and found a statistically significant bunching under those thresholds when compared with company-size distribution in the years prior to the regulations.

Measuring Regulatory Costs Through “Bunching Estimation”

By examining how firms are bunching below those three thresholds, Xiao and Ewens were able to infer the regulatory compliance costs of crossing them. “The maximum amount of money they are willing to give up in order to avoid regulation essentially tells you the true net cost of regulation,” Xiao says.

The study shows the compliance costs of the three regulatory rules range from 1.2 to 1.8 percent of market capitalization for the firms near those thresholds; for a median US public company, the compliance costs amount to 4.3 percent of market capitalization. It's one of the first truly objective measures of the monetary cost of regulation.

While acknowledging that the numbers are not insignificant, Ewens speculates that those costs aren’t high enough for a company to continue manipulating its float indefinitely.

“It takes time and energy to manipulate a float, and your ultimate goal is to grow your company,” Ewens says. “You’re going to cross that threshold eventually.”

Growing Availability of Private Funding

Using these estimated compliance costs and a model estimating the probability of a firm going public, Xiao and Ewens ran several counterfactual analyses looking at how the number of companies going public each year would have been different if various regulations, such as the Sarbanes–Oxley Act of 2002, didn’t exist.

They found that even removing all post-2000 regulatory costs would not change the declining trend in IPOs. In fact, they concluded that regulatory costs themselves probably account for only 7.3 percent of the IPO decline, especially since IPOs don’t face size-triggered regulations all at once. Other factors are likely more to blame, particularly the growing availability of private funding through avenues like venture capital and private equity.

“Firms are staying private because they can now in ways that they couldn't before,” Ewens says. “They can raise money at crazy valuations and not worry about running out and having to tap the public markets."

But while those alternative financing options benefit companies, they may undermine economic opportunity for the country as a whole by reducing the public’s access to investment markets. Xiao says it would be unfortunate if the growth of the next big, successful companies are “only benefiting a few VC masters and private equity investors. We somehow need to make sure that the dividends are paying out to everybody.”

Regulations vs. Other Factors Behind Fewer IPOs

The bunching estimator approach to regulatory cost does have some limitations: It applies only to regulations with size-based thresholds, and it doesn’t work with brand new regulations. But by capturing both direct and indirect costs, Xiao and Ewens’s work gives regulators a more comprehensive and objective tool when reviewing the cost-benefit balance of existing regulations. Moreover, net cost estimates can also guide decisions about new regulatory proposals when these new rules bear similarity to existing ones or when regulators conduct pilot experiments on a subset of firms.

The new study represents a significant contribution to the ongoing conversation about the effect of regulations on both individual firms and the broader public markets. Being able to estimate actual costs may give regulators more confidence in pushing back on calls for deregulation.

“We hope our method can help move the needle on these cost-benefit analyses,” Xiao says. “The public market is disappearing, and it’s concerning, but regulatory cost isn’t the smoking gun.”

FAQs:

Q: How many US public companies exist today compared with the 1990s?

A: The number has dropped by about 50 percent — from over 8,000 in the 1990s to around 4,000 today.

Q: What’s the common theory for this decline?

A: Many blame the cost of complying with government regulations for discouraging companies from going public.

Q: How does this new research measure the cost of regulation?

A: The study by Columbia Business School’s Michael Ewens and Kairong Xiao uses a “bunching estimation” approach, observing how companies adjust their public float to stay below regulatory thresholds.

Q: What did the researchers find?

A: Regulatory compliance costs range from 1.2% to 1.8% of market cap near certain thresholds — 4.3% for a median US public company. While meaningful, these costs explain only about 7.3% of the decline in IPOs.

Q: If not regulation, what’s causing fewer companies to go public?

A: The rise of private funding — venture capital, private equity, and other alternative financing — gives companies the ability to stay private longer.

Q: Why does this matter for investors and the public?

A: When high-growth companies remain private, their gains are concentrated among a small group of private investors, limiting opportunities for the broader public to participate.

Q: How can this research help regulators?

A: The bunching estimation method offers an objective way to quantify regulatory costs, helping policymakers weigh costs against benefits when reviewing or designing regulations.

Adapted from “Regulatory Costs of Being Public: Evidence from Bunching Estimation” by Michael Ewens and Kairong Xiao of Columbia Business School and Ting Xu of the University of Toronto.