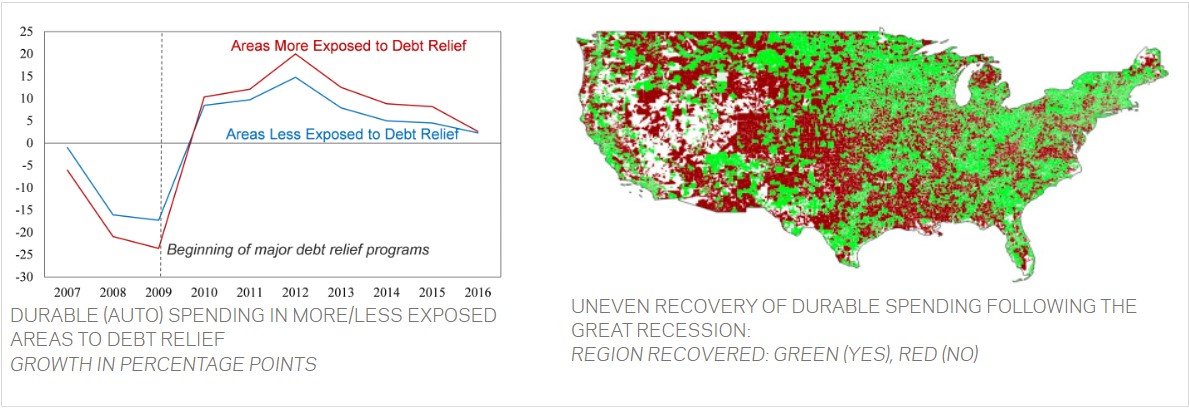

Debt Relief and Real Economy

Research by Tomasz Piskorski of Columbia Business School and Amit Seru of the Stanford Graduate School of Business demonstrates that regions of the US that received more mortgage debt relief recovered much faster following the Great Recession in terms of consumer spending, employment, and housing prices compared to those that received less debt relief.

- See “Debt relief and slow recovery: A decade after Lehman”, T Piskorski and A. Seru, forthcoming in the Journal of Financial Economics [See also May 2019 NBER Digest]

Factors Affecting the Extent of Debt Relief and Pass-Through of Lower Rates to Households

The research by Tomasz Piskorski and Amit Seru also shows that there have been significant barriers to provision of effective debt relief by financial sector and pass-through of low interest rates to households. These factors significantly hampered economic recovery following the Great Recession.

Piskorski and Seru findings suggest that solely relying on private sector for implementation of effective debt relief polices is challenging. Moreover, the considerable regional heterogeneity in economic conditions indicates that one-size-fits-all polices are not that effective and there are significant gains from tying debt relief polices to local economic conditions.

For an overview of these barriers and their implications for mortgage market design and future policy interventions see:

- “Mortgage market design: Lessons from the Great Recession”, T Piskorski and A. Seru, Brookings Papers on Economic Activity Spring 2018.

Below is a list of factors that were shown to adversely affect the extent of debt relief and pass-through of low interest rates to households:

- Mortgage contract rigidity limiting pass-through of lower rates to households: The rigidity of fixed rate mortgages (FRMs), in contrast to more flexible ARMs, hampers the pass-through of debt relief during periods of low interest rates. In particular, the reduction of interest rates during the Great Recession provided borrowers with certain types of ARMs an automatic debt relief, which was not available to households with FRMs.

- See Di Maggio, M., A. Kermani, B. Keys, T. Piskorski, R. Ramcharan, A. Seru, V. Yao, 2017, Interest Rate Pass-Through: Mortgage Rates, Household Consumption and Voluntary Deleveraging, American Economic Review 107, 3550-88. [See also March 2015 NBER Digest]

- Refinancing constraints limiting pass-through of lower rates to households: Households with fixed rate mortgages, the predominant financial obligation of U.S. households, rely primarily on refinancing to receive debt relief from the low interest rate environment induced by monetary policy. Many of these households were left with little equity as house prices dropped during the Great Recession, making them ineligible for loan refinancing that requires a certain amount of borrower equity. In addition, limited competition in the refinancing market and intermediary capacity constrains have also limited the effectiveness of the Home Affordable Refinance Program aimed at facilitating refinancing of such insufficiently collateralized loans.

- See Agarwal, S., G. Amromin, S. Chomsisengphet, T. Landvoigt, T. Piskorski, A. Seru, and V. Yao. 2017, Mortgage Refinancing, Consumer Spending, and Competition: Evidence from the Home Affordable Refinance Program, NBER Working Paper. [See also November 2015 NBER Digest]

- Limited organizational capability of intermediaries to perform loan modifications: The U.S. economy experienced limited loan restructuring during the Great Recession, despite the surge in distressed borrowers. Financial intermediary specific factors impacted the extent of debt relief that was passed to households (and regions), with certain intermediaries having the organizational ability to renegotiate loans significantly more than others. These factors have also limited the effectiveness of the Home Affordable Modification Program that provided financial institutions with monetary incentives to renegotiate distressed mortgages.

- See Agarwal, S., G. Amromin, I. Ben-David, S. Chomsisengphet, T. Piskorski, and A. Seru, 2017, Policy Intervention in Debt Renegotiation: Evidence from Home Affordable Modification Program, Journal of Political Economy 125, 654-712. [See also Lessons learned from HAMP]

- Limited incentives of financial institutions to modify securitized debt that they service for others: Financial institutions were much less likely to renegotiate loans of distressed borrowers if they service these loans for others due to securitization compared to loans they own.

- See Piskorski, T., A. Seru, and V. Vig, 2010, Securitization and Distressed Loan Renegotiation: Evidence from the Subprime Mortgage Crisis, Journal of Financial Economics 97, 369- 397.

- Concerns of financial intuitions that debt relief programs may induce excessive defaults by households: Limited loan restructuring activity can also reflect lenders’ concerns about future moral hazard by borrowers and the inability of lenders to evaluate the repayment ability of borrowers.

- See Mayer, C., E. Morrison, T. Piskorski, and A. Gupta, 2014, Mortgage Modification and Strategic Behavior: Evidence from a Legal Settlement with Countrywide, American Economic Review 104, 2830-285.

Government and Private Household Debt Relief during COVID-19

This newly published paper by Tomasz Piskorski with Susan Cherry (Stanford University), Erica Xuewei Jiang (University of Southern California - Marshall School of Business), Gregor Matvos (Northwestern University - Kellogg School of Management), and Amit Seru (Stanford University)based on following a panel of millions of US consumers, suggests that the majority of forbearance occurred under the provisions of the CARES Act. The researchers estimate that borrowers in forbearance will be left with a “forbearance overhang” of more than $60 billion in accumulated postponed repayments. This forbearance debt overhang amounts to about $1,800 per individual, which is more than half of their average monthly income, and more than 80% for lower income borrowers.

From a policy perspective, thinking through possible extension of provisions of CARES act that are about to expire is critical. Moreover, whenever they do expire, unwinding of forbearance—which could be done in several ways such as front loading or uniformly amortizing or back loading payments—could have first order consequences for household debt distress, and through it, for the aggregate economy.

Key Highlights

- Debt forbearance provided households a very significant financial relief: Loans worth $2 trillion entered forbearance, allowing more than 60 million of Americans to miss cumulative $70 billion of their debt payments.

- Debt forbearance can explain low consumer debt delinquency rates during the pandemic despite record unemployment, with potential significant positive consequences for house prices and consumer spending

- Forbearance rates are higher among the more vulnerable populations: individuals with lower credit scores and lower incomes. Borrowers in regions with a higher likelihood of COVID-19 related economic shocks and higher shares of minorities were more likely to obtain debt relief.

- Forbearance have also importantly complemented other stabilization programs by providing significant relief to financially vulnerable individuals with higher pre-pandemic incomes: 60% of aggregate dollar amount of forbearance has been provided to above median income borrowers, mainly reflecting their higher debt balances.

Media Coverage

The Lesson Lenders Learned from the Great Recession: Forbearance Works (Fortune)

Why a Third of Borrowers in Debt Forbearance Programs are Still Paying Their Bills (Money)

Hutchins Roundup: Debt Forbearance, Online Recruiting, and More (Brookings)